1

Follow

1802

Followers

概要

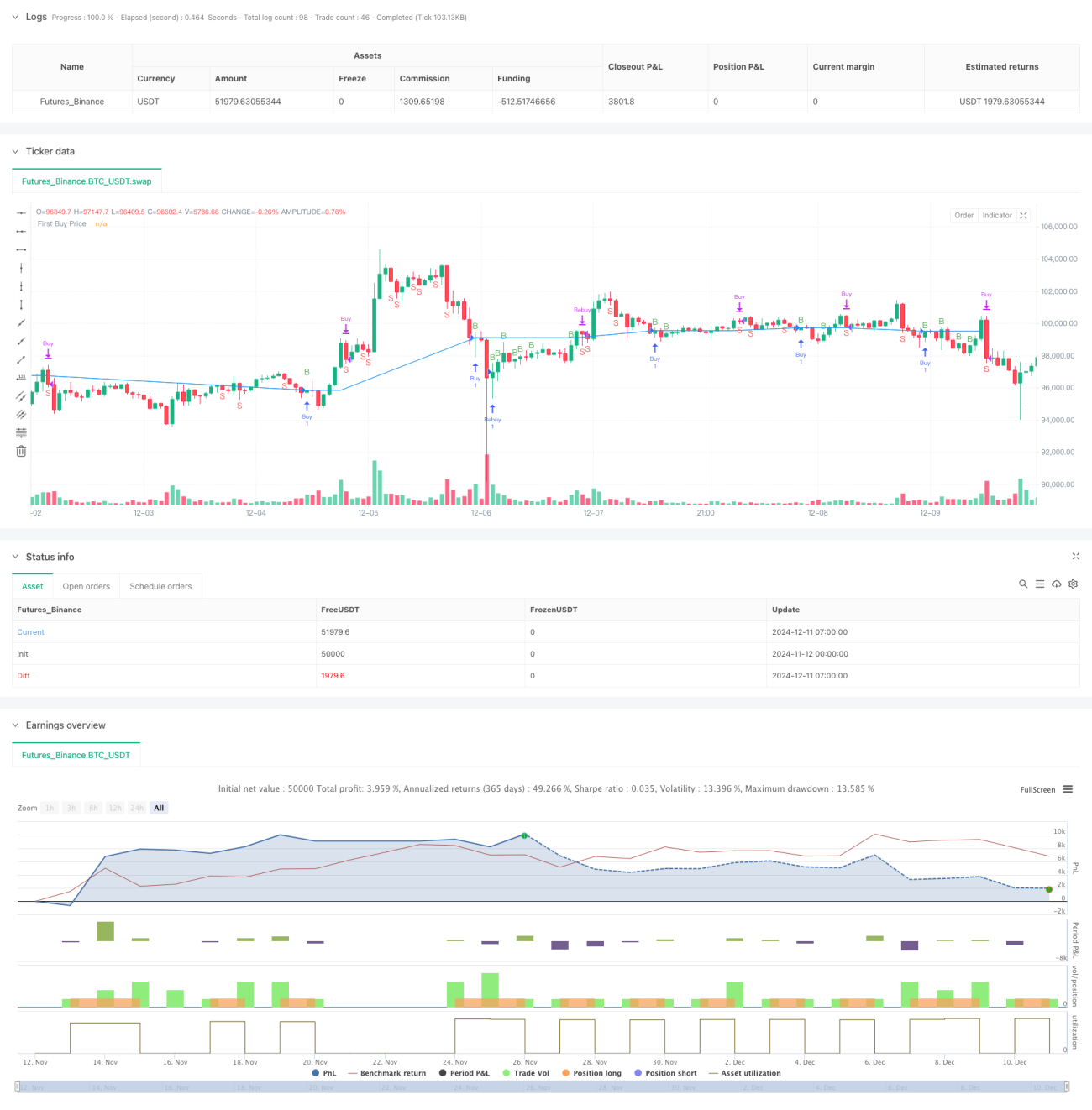

本戦略は、二重RSI(相対力指数)指標に基づく適応型取引システムです。異なる時間周期のRSI指標を組み合わせて市場のトレンドと取引機会を識別し、資金管理とリスク管理メカニズムを通じて取引パフォーマンスを最適化します。本戦略の核心は、マルチサイクルRSIの連携により、取引の安全性を確保しつつ収益性を高める点にあります。

戦略原理

本戦略は7周期のRSIを主要な取引シグナルとして使用し、同時に日足RSIをトレンドフィルターとして活用します。短期RSIが40未満から上抜けし、かつ日足RSIが55を超えた場合、システムは買いシグナルを発します。ポジション保有中に価格が最初の建値より下落した場合、システムは自動でポジションを追加し、平均コストを低減します。RSIが60以上から下抜けした場合、システムは利益確定で決済します。また、5%のストップロスを設定してリスクを抑制します。戦略には資金管理モジュールも含まれており、総資金とあらかじめ設定したリスク比率に基づいて各取引のポジションサイズを自動計算します。

戦略の利点

- マルチサイクルRSIの組み合わせにより、シグナルの信頼性が向上

- 適応型のポジション追加メカニズムにより、保有コストを効果的に低減可能

- リスク選好に応じてポジションサイズを自動調整する完全な資金管理システム

- 固定ストップロス保護により、各取引のリスクを厳格に管理

- 取引コストを考慮しており、実際の取引環境に適合

戦略のリスク

- RSI指標は激しく変動する市場で誤ったシグナルを発生させる可能性あり

- ポジション追加メカニズムは継続的な下落相場で大きな損失をもたらす可能性あり

- 固定パーセンテージのストップロスは高ボラティリティ時期に過度に保守的になる可能性あり

- 取引コストは頻繁な取引時に収益に著しい影響を与える可能性あり

- 戦略実行には十分な流動性が必要

戦略の最適化方向性

- ボラティリティ指標(例:ATR)を導入し、ストップロス水準を動的に調整

- トレンド強度フィルターを追加し、レンジ相場での誤ったシグナルを低減

- ポジション追加ロジックを最適化し、市場のボラティリティを考慮して動的に調整

- より多くの時間周期のRSI確認シグナルを追加

- 適応型のポジション管理システムを開発

まとめ

本戦略はテクニカル分析とリスク管理を組み合わせた完全な取引システムです。マルチサイクルRSIの連携により取引シグナルを提供し、資金管理とストップロスメカニズムによりリスクを制御します。この戦略はトレンドが明確な市場での運用に適していますが、実際の市場状況に応じてパラメータの最適化が必要です。システムの拡張性は良好で、さらなる最適化の余地を残しています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1