高度なトレンドフォローと適応型トレーリングストップロス戦略

1

Follow

1802

Followers

概要

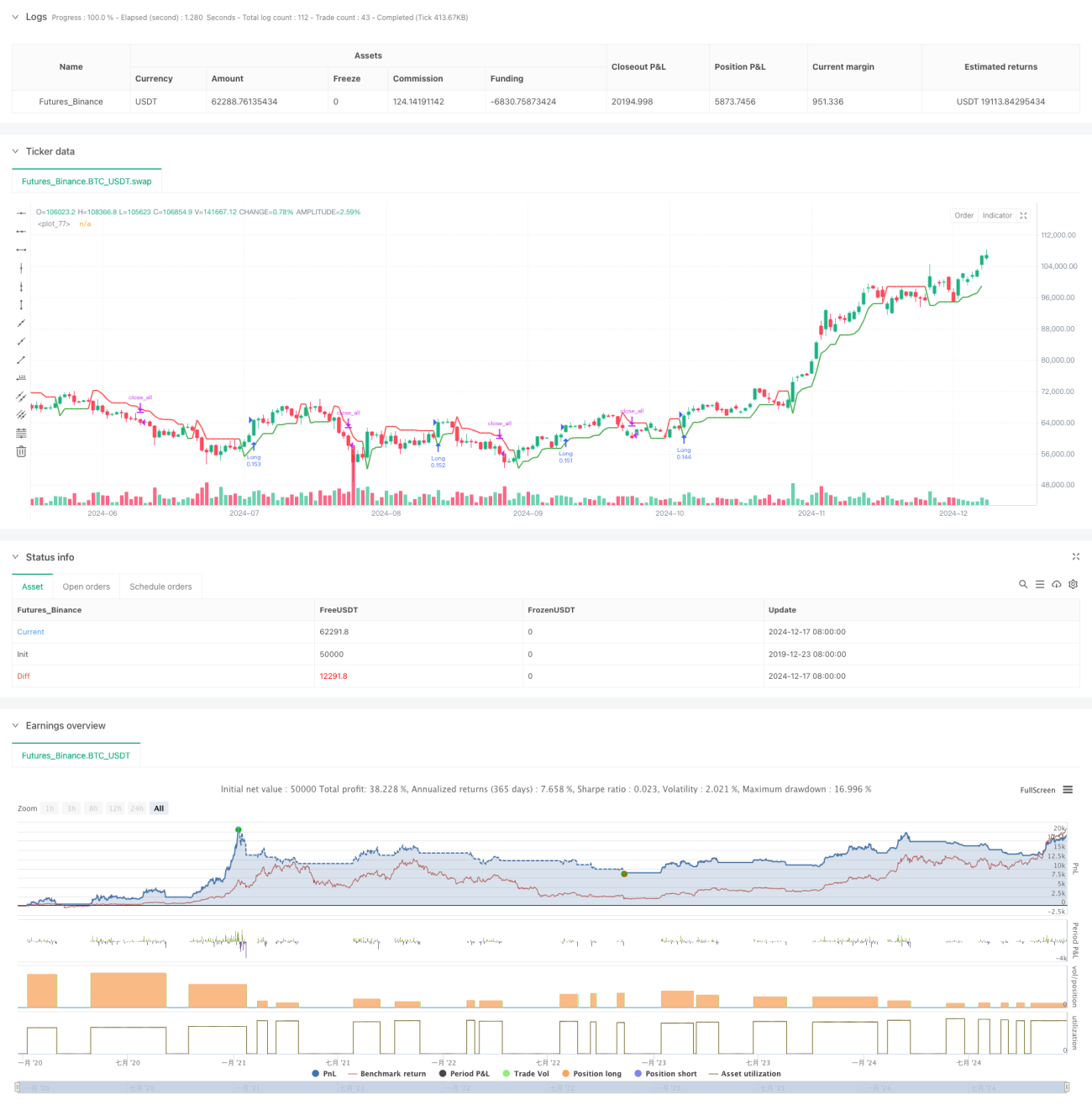

これはSupertrendインジケーターをベースとしたトレンドフォロー戦略であり、適応型のトレーリングストップ機構を組み合わせています。本戦略は主にSupertrendインジケーターを用いて市場のトレンド方向を識別し、動的に調整されるトレーリングストップによってリスク管理とエグジットタイミングの最適化を図ります。戦略は複数のストップ方式(パーセンテージストップ、ATRストップ、固定ポイントストップ)をサポートし、異なる市場環境に応じて柔軟に調整可能です。

戦略原理

戦略のコアロジックは以下の主要要素に基づきます:

- Supertrendインジケーターをトレンド判断の主な基準として使用。このインジケーターはATR(平均真実レンジ)を組み合わせて市場のボラティリティを測定します。

- エントリーシグナルはSupertrendの方向変化によってトリガーされ、ロング、ショート、または双方向の取引をサポートします。

- ストップ機構には適応型のトレーリングストップを採用し、市場のボラティリティに応じてストップ位置を自動調整します。

- 取引管理システムにはポジション管理(デフォルトでは口座残高の15%ポジション)と時間フィルタリング機構が含まれます。

戦略の利点

- トレンド捕捉能力が高い:Supertrendインジケーターにより主要トレンドを効果的に識別し、誤判定を低減します。

- リスク管理が充実:多様なストップ機構を採用し、異なる市場環境に適応可能です。

- 柔軟性が高い:複数の取引方向やストップ方式の設定が可能です。

- 適応性が強い:トレーリングストップが市場のボラティリティに応じて自動調整され、戦略の適応力を向上させます。

- 完全なバックテストシステム:時間フィルタリング機能が組み込まれており、過去のパフォーマンス分析に便利です。

戦略のリスク

- トレンド反転リスク:激しい変動市場では誤ったシグナルが発生する可能性があります。

- スリッページリスク:トレーリングストップの執行が市場流動性の影響を受ける可能性があります。

- パラメータ感応度:Supertrendの係数とATR期間の設定が戦略パフォーマンスに大きく影響します。

- 市場環境依存性:レンジ相場では頻繁な取引によりコストが増加する可能性があります。

戦略の最適化方向

- シグナルフィルターの最適化:追加のテクニカル指標を用いて誤ったシグナルをフィルタリングできます。

- ポジション管理の最適化:市場のボラティリティに応じてポジション比率を動的に調整可能です。

- ストップ機構の強化:平均コストを組み合わせたより複雑なストップロジックを設計できます。

- エントリータイミングの最適化:価格構造分析を追加することでエントリー精度を向上させられます。

- バックテストシステムの充実:より多くの統計指標を追加して戦略パフォーマンスを評価できます。

まとめ

本戦略は設計が合理的でリスクが管理可能なトレンドフォロー戦略です。Supertrendインジケーターと柔軟なストップ機構を組み合わせることで、高い収益性を維持しつつリスクを効果的に制御できます。戦略の設定自由度が高く、様々な市場環境での使用に適していますが、十分なパラメータ最適化とバックテストによる検証が必要です。今後はさらに多くのテクニカル分析ツールやリスク管理手段を追加することで、戦略の安定性と収益性を向上させることが可能です。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Supertrend Strategy with Adjustable Trailing Stop [Bips]", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15)

// InputsStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1