多重時間枠トレンドフォローとATRによる利益確定・損切り戦略

1

Follow

1802

Followers

概要

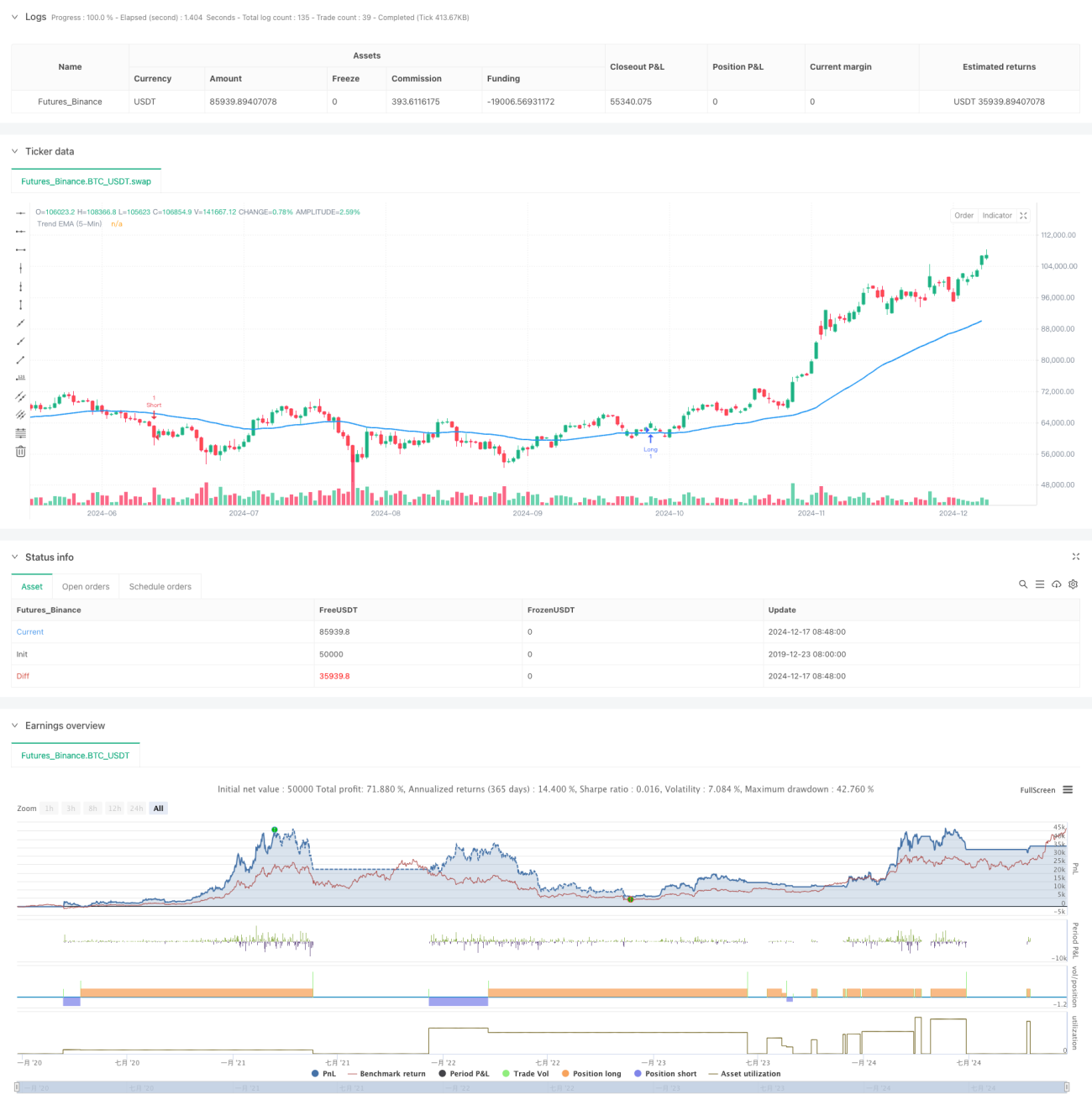

これは、UT Botと50期間指数移動平均(EMA)を組み合わせたトレンドフォロー型取引戦略です。主に1分足で短期売買を行い、5分足のトレンドラインを方向性のフィルターとして使用します。ATR指標を用いて動的にストップロスを計算し、2つの利確目標を設定して利益を最適化します。

戦略の原理

戦略の中心的なロジックは、以下の主要コンポーネントに基づいています。

- UT Botを使用して動的サポート・レジスタンスラインを計算

- 5分足の50期間EMAで全体トレンド方向を判断

- 21期間EMAとUT Botのシグナルを組み合わせて具体的なエントリーポイントを決定

- ATRの倍数で動的トレーリングストップロスを設定

- 0.5%と1%の2つの利確目標を設定し、それぞれ50%ポジションを決済

価格がUT Botが計算したサポート/レジスタンスラインをブレイクし、21期間EMAとUT Botがクロスした際、価格が5分足の50期間EMAの正しい方向にあれば、取引シグナルがトリガーされます。

戦略の強み

- 複数時間足の組み合わせにより取引の信頼性向上

- 動的ATRストップロスは市場の変動に適応可能

- 二重利確目標で収益と勝率のバランスを最適化

- Heikin Ashiローソク足を使用することで偽のブレイクを一部フィルタリング

- 柔軟な取引方向の選択(買いのみ、売りのみ、両方向取引可)

戦略のリスク

- 短期取引ではスプレッドや手数料コストが高くなる可能性

- ボックス相場では偽シグナルが頻発する可能性

- 複数条件による制限で潜在的な取引機会を逃す可能性

- ATRパラメータの設定は市場ごとに最適化が必要

戦略の最適化方向

- 出来高指標を補助確認として追加可能

- より多くの市場心理指標の導入を検討

- 市場の変動特性に応じた適応パラメータの開発

- 取引時間帯のフィルター追加

- よりスマートなポジション管理システムの開発

まとめ

本戦略は、複数のテクニカル指標と時間足を組み合わせることで、完全な取引システムを構築しています。明確なエントリー・エグジット条件に加え、堅牢なリスク管理メカニズムも備えています。実際の運用では市場状況に応じたパラメータ最適化が必要ですが、全体のフレームワークは実用性と拡張性に優れています。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Created by Nasser mahmoodsani' all rights reserved

// E-mail : [email protected]

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1