# マルチタイムフレーム流動性ハブヒートマップ定量戦略

1

Follow

1802

Followers

概要

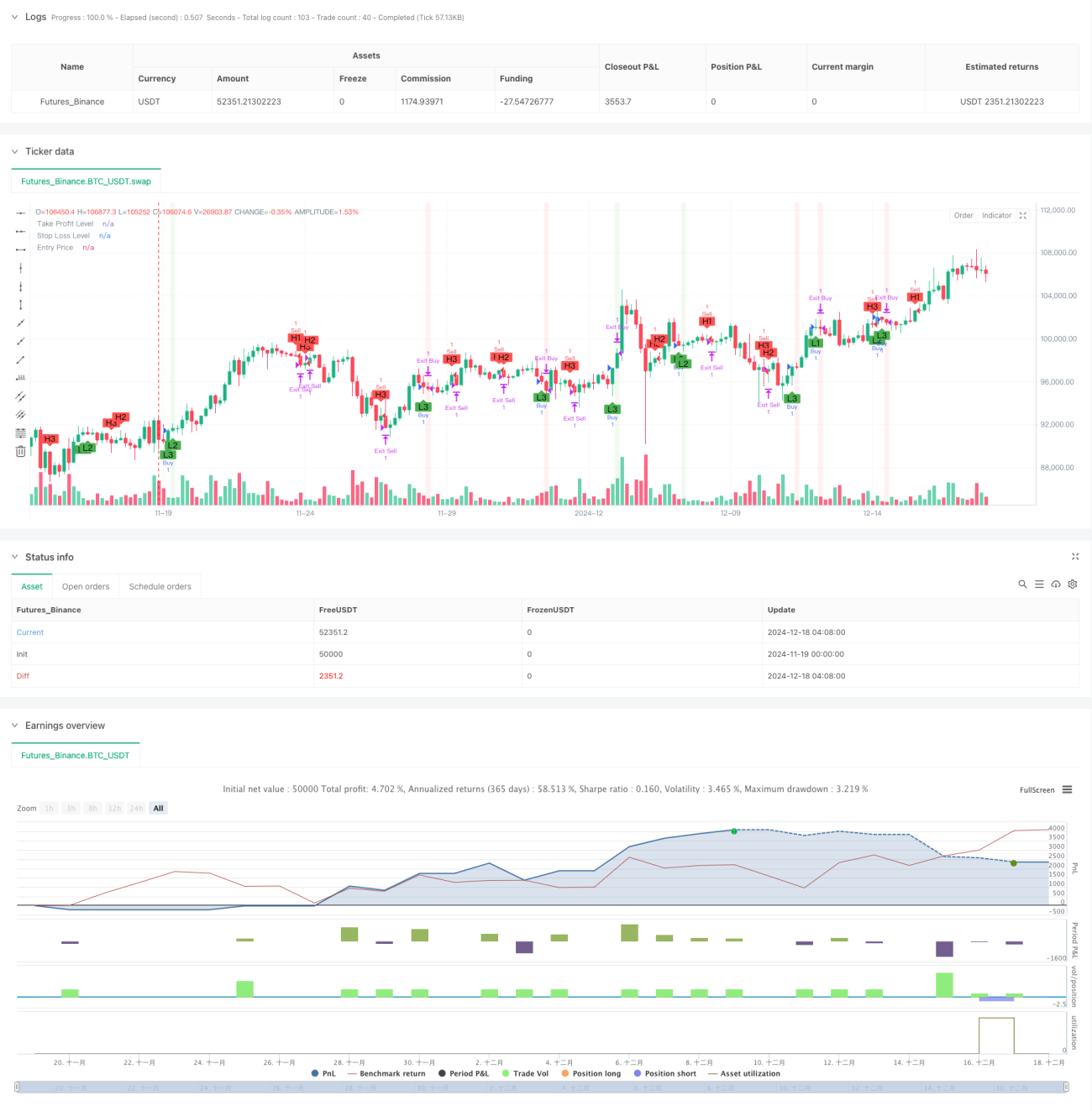

本戦略は、複数時間枠の流動性ハブポイント検出に基づく定量取引システムです。3つの異なる時間枠(15分・1時間・4時間)の価格行動を分析し、重要なサポート・レジスタンス水準を特定し、それに基づいて取引判断を行います。システムは、固定額の利食い・損切り設定を含む資金管理機能を統合し、トレーダーが市場構造をより良く理解できるよう直感的な視覚フィードバックを提供します。

戦略の原理

戦略の中核は、ta.pivothighおよびta.pivotlow関数を用いて複数時間枠で価格ハブポイントを検出することです。各時間枠において、左右の参照ローソク足数(デフォルト7)を使用して有意な高値・安値を特定します。任意の時間枠で新たなハブ安値が出現した場合、ロングシグナルを生成し、新たなハブ高値が出現した場合、ショートシグナルを生成します。取引執行は固定額の利食い・損切り管理により行われ、moneyToSLPoints関数で米ドル金額を対応するポイント数に変換します。

戦略の優位性

- 複数時間枠分析により、より包括的な市場の視点が得られ、異なるレベルの取引機会を捉えるのに役立ちます

- ハブポイントに基づく取引ロジックは確固たるテクニカル分析基盤を持ち、理解・実行が容易です

- 統合された資金管理機能により、各取引のリスクを効果的にコントロールできます

- 可視化インターフェースにより、ポジション、利食い・損切り水準、損益領域などの取引状態を直感的に表示します

- 戦略パラメータは調整可能で、適応性が高く、さまざまな市場条件に応じた最適化が可能です

戦略のリスク

- 複数時間枠のシグナルが競合する可能性があり、合理的なシグナル優先順位メカニズムを構築する必要があります

- 固定額の利食い・損切りはすべての市場条件に適しているとは限らず、ボラティリティに応じて動的に調整することを推奨します

- ハブポイント検出の遅延により、エントリータイミングが遅れる可能性があります

- 激しい変動時には、偽のブレイクアウトシグナルが発生する可能性があります

- 時間枠ごとの流動性の差異に注意する必要があります

戦略の最適化方向

- ボラティリティ指標を導入し、利食い・損切り水準を動的に調整する

- 出来高確認メカニズムを追加し、ハブポイントの信頼性を高める

- 時間枠優先順位システムを開発し、シグナル競合を解決する

- トレンドフィルターを統合し、レンジ相場での過剰取引を回避する

- 価格構造分析を追加し、エントリータイミングの精度を向上させる

まとめ

複数時間枠の流動性ハブポイントヒートマップ定量戦略は、構造が整い、ロジックが明確な取引システムです。多角的な市場分析と厳格なリスク管理により、トレーダーに信頼性の高い取引フレームワークを提供します。固有のリスクや制限はあるものの、継続的な最適化と改善により、本戦略はさまざまな市場環境で安定したパフォーマンスを維持することが期待されます。

Source

Pine

/*backtest

start: 2024-11-19 00:00:00

end: 2024-12-18 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pmotta41

//@version=5

strategy("GPT Session Liquidity Heatmap Strategy", overlay=true)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1