動的トレンドモメンタム最適化戦略とGチャンネル指標の組み合わせ

1

Follow

1802

Followers

概要

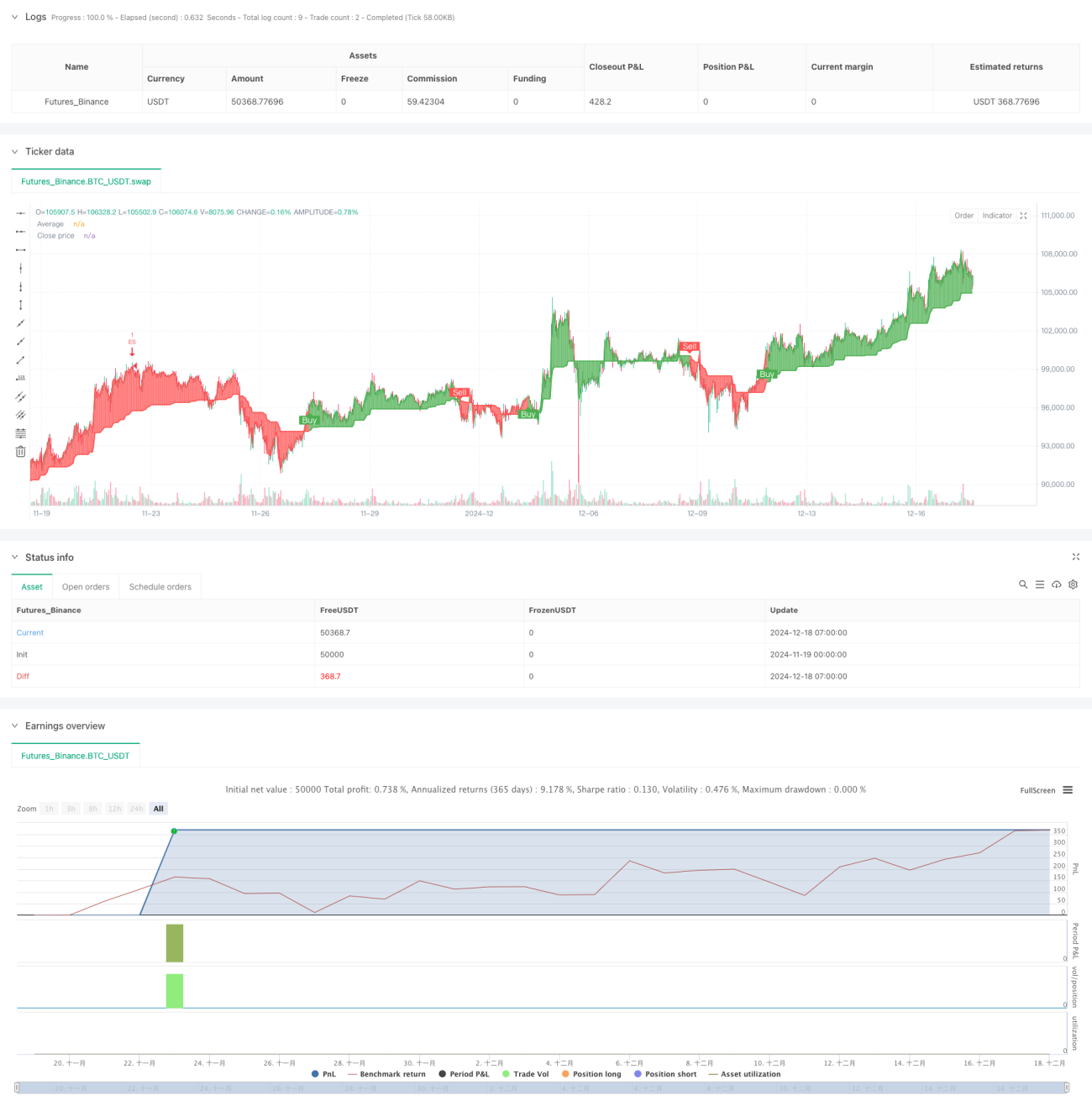

本戦略は、Gチャネル、RSI、MACDインジケーターを融合した高度なトレンド追跡取引システムです。サポートゾーンとレジスタンスゾーンを動的に計算し、モメンタム指標を組み合わせることで、確率の高い取引機会を特定します。戦略の核心は、カスタムGチャネル指標を用いて市場トレンドを判断し、RSIとMACDでモメンタムの変化を確認し、より正確なトレードシグナルを生成することにあります。

戦略の原理

本戦略は三重のフィルタリングメカニズムを採用し、取引シグナルの信頼性を確保します。まずGチャネルは、指定期間内の最高価格と最低価格を計算することで、サポートゾーンとレジスタンスゾーンを動的に構築します。価格がチャネルをブレイクすると、システムは潜在的なトレンド転換点を識別します。次にRSI指標は、市場が買われすぎまたは売られすぎの状態にあるかを確認し、より価値のある取引機会を選別するのに役立ちます。最後にMACD指標は、ヒストグラムの正負値によってモメンタムの方向と強さを確認します。これら3つの条件がすべて満たされた場合のみ、システムは取引シグナルを発します。

戦略の優位性

- 多次元のシグナル確認メカニズムにより、取引の精度が大幅に向上

- 動的なストップロスと利益確定設定により、リスクを効果的に管理

- Gチャネルの適応特性により、さまざまな市場環境に対応可能

- ポジション管理や資金管理を含む、優れたリスク管理システム

- 視覚的なラベルシステムにより取引シグナルを直感的に表示、分析と最適化が容易

戦略のリスク

- レンジ相場では誤ったシグナルが発生する可能性があり、市場環境の識別が必要

- パラメータの過度な最適化はオーバーフィッティングのリスクにつながる

- 複数の指標は高ボラティリティ期間にラグ効果を生じる可能性がある

- ストップロス水準の設定が不適切だと、大きなドローダウンを招く恐れがある

戦略の最適化方向

- 市場環境識別モジュールを導入し、異なる市場状態に応じて異なるパラメータ設定を使用

- 市場のボラティリティに応じてストップロス水準を動的に調整する、適応型ストップロスメカニズムを開発

- 出来高分析指標を追加し、シグナルの信頼性を向上

- Gチャネルの計算方法を最適化し、ラグ効果を低減

まとめ

本戦略は、複数のテクニカル指標を総合的に活用することで、完全な取引システムを構築しています。その核心的な優位性は、多次元のシグナル確認メカニズムと優れたリスク管理システムにあります。継続的な最適化と改良により、さまざまな市場環境で安定したパフォーマンスを維持することが期待されます。トレーダーは実運用前に、異なるパラメータの組み合わせを十分にテストし、具体的な市場特性に応じて適切に調整することを推奨します。

Source

Pine

/*backtest

start: 2024-11-19 00:00:00

end: 2024-12-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("VinSpace Optimized Strategy", shorttitle="VinSpace Magic", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input ParametersStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1