1

Follow

1802

Followers

概要

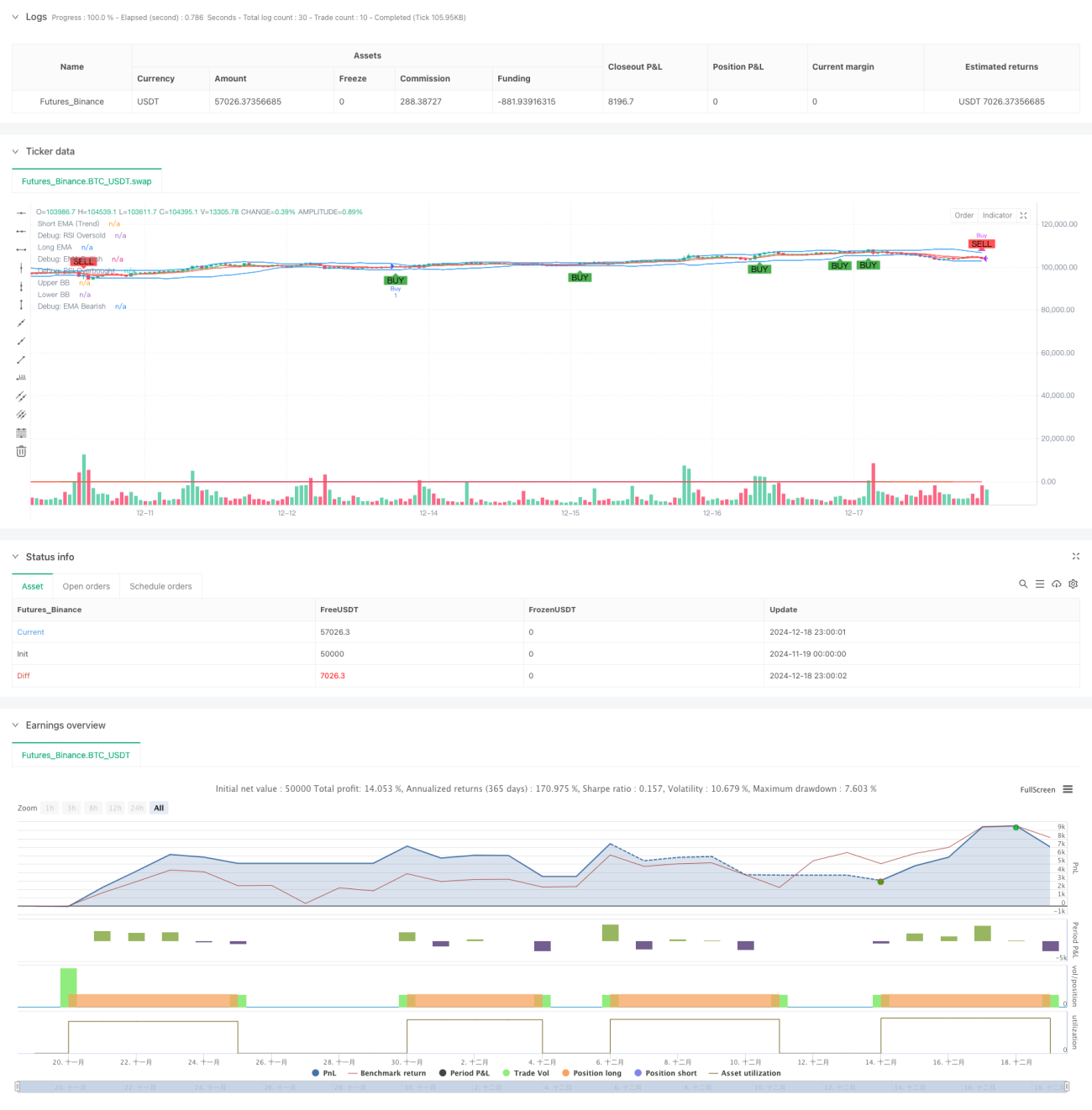

この戦略は、複数のテクニカル指標を組み合わせた総合的な取引システムであり、主に市場のモメンタムとトレンドの変化を動的に監視し、取引機会を捉えることを目的としています。戦略は、移動平均線システム(EMA)、相対力指数(RSI)、移動平均収束拡散法(MACD)、ボリンジャーバンド(BB)などの複数の指標を統合し、さらに真の変動幅(ATR)に基づく動的ストップロス機構を導入することで、市場を多次元的に分析し、リスクを管理します。

戦略の原理

戦略は多層的なシグナル確認メカニズムを採用しており、主に以下の側面から構成されています:

- トレンド判断:7期間と14期間のEMAのクロスを使用して市場のトレンド方向を判断します。

- モメンタム分析:RSI指標を通じて市場の買われすぎ・売られすぎ状態を監視し、30/70の動的しきい値を設定します。

- トレンド強度の確認:ADX指標を導入してトレンドの強さを判断し、ADX>25の場合に強いトレンドの存在を確認します。

- 変動範囲の判断:ボリンジャーバンドを用いて価格変動範囲を定義し、価格がバンドに触れる状況に応じて取引シグナルを生成します。

- 出来高の検証:動的な出来高移動平均線を用いてフィルタリングし、取引が十分な市場活性度のもとで行われることを保証します。

- リスク管理:ATR指標に基づく動的ストップロス戦略で、ストップロスの距離はATRの1.5倍です。

戦略の利点

- 多次元的なシグナル検証により、誤ったシグナルを効果的に低減できます。

- 動的ストップロス機構により、戦略のリスク適応能力が向上します。

- 出来高とトレンド強度の分析を組み合わせることで、取引の信頼性が高まります。

- 指標パラメータが調整可能であり、適応性に優れています。

- 完全なエントリーとエグジットのメカニズムを備え、取引ロジックが明確です。

- 標準的なテクニカル指標を使用しているため、理解と保守が容易です。

戦略のリスク

- 複数の指標により、シグナルが遅れる可能性があります。

- パラメータの最適化には過学習のリスクが伴う可能性があります。

- 横ばい相場では頻繁な取引が発生する可能性があります。

- 複雑なシグナルシステムにより計算負荷が増大する可能性があります。

- 戦略の有効性を検証するためには、十分なサンプル量が必要です。

戦略の最適化の方向性

- 市場のボラティリティに適応するメカニズムを導入し、指標パラメータを動的に調整します。

- 時間フィルターを追加し、不利な時間帯の取引を回避します。

- 利益確定戦略を最適化し、トレーリングストップを検討します。

- 取引コストを考慮し、エントリー・エグジット条件を最適化します。

- ポジション管理メカニズムを導入し、ポジションサイズを動的に調整します。

まとめ

本戦略は、複数の指標を協調させることで、比較的完成度の高い取引システムを構築しています。中核となる利点は、多次元的なシグナル確認メカニズムと動的なリスク管理システムにありますが、パラメータの最適化や市場適応性の問題にも注意が必要です。継続的な最適化と調整により、本戦略は様々な市場環境で安定したパフォーマンスを発揮することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1