標準化対数収益に基づく適応的動的取引戦略

1

Follow

1802

Followers

概要

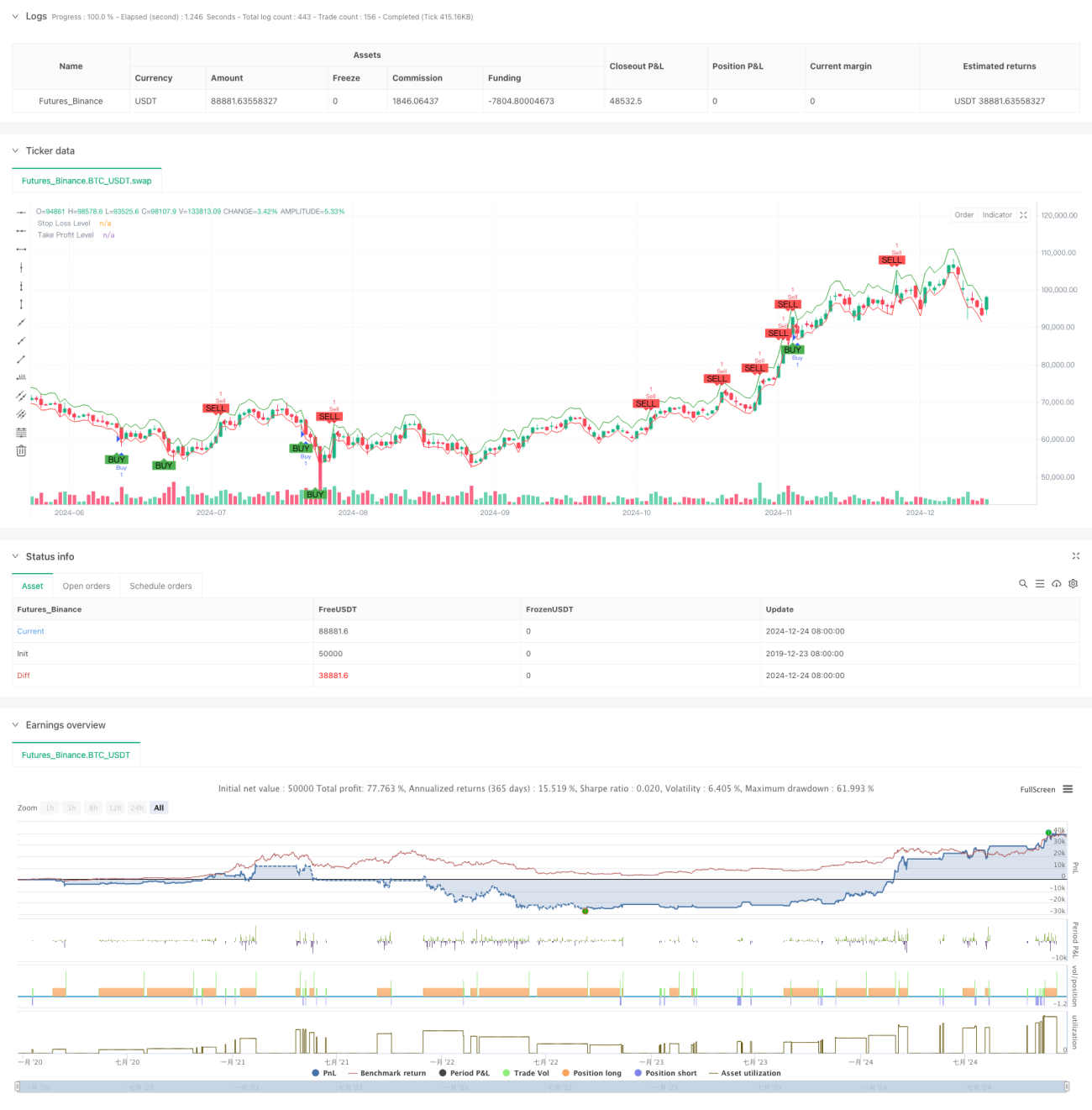

本戦略は、Shiryaev-Zhou指数(SZI)に基づく適応型取引システムです。対数収益率の標準化スコアを計算し、市場の買われ過ぎ・売られ過ぎ状態を特定することで、価格の平均回帰機会を捉えます。動的なストップロスと利益確定目標を組み合わせ、リスクの精密な制御を実現します。

戦略の原理

戦略の中核は、対数収益率のローリング統計特性を用いて標準化指標を構築することです。具体的な手順は以下の通りです。

- 対数収益率を計算し、収益率の正規化処理を実現

- 50期間のウィンドウでローリング平均と標準偏差を計算

- SZI指標を構築: (対数収益率 - ローリング平均) / ローリング標準偏差

- SZIが -2.0 を下回ったときにロングシグナル、2.0 を上回ったときにショートシグナルを生成

- エントリー価格に基づく2%のストップロスと4%の利確水準を設定

戦略の利点

- 理論的基盤がしっかりしている: 対数正規分布の仮定に基づき、統計学的に優れたサポートがある

- 適応性が高い: ローリングウィンドウによる計算で、市場の変動特性の変化に適応可能

- リスク管理が充実: パーセンテージベースのストップロス戦略を採用し、各取引のリスクを精密に制御

- 視覚化に優しい: チャート上に取引シグナルとリスク管理水準を明確に表示

戦略のリスク

- パラメータ感応度: ローリングウィンドウの長さと閾値の選択が戦略のパフォーマンスに大きく影響する

- 市場環境依存: トレンド相場では頻繁な偽シグナルが発生する可能性がある

- スリッページの影響: 急激な変動時には、実際の約定価格が理想水準から大きく乖離する可能性がある

- 計算遅延: 統計指標のリアルタイム計算により、シグナルに遅延が生じる可能性がある

戦略の最適化方向

- 動的閾値: 市場のボラティリティに応じてシグナル閾値を動的に調整することを検討

- 複数時間枠: 複数の時間枠のシグナル確認メカニズムを導入

- ボラティリティフィルター: 極端な変動期間中は取引を停止またはポジションを調整

- シグナル確認: 出来高やモメンタムなどの補助指標を追加してシグナルを確認

- ポジション管理: ボラティリティに基づく動的なポジション管理を実現

まとめ

本戦略は、堅固な統計学に基づく定量取引戦略であり、標準化された対数収益率を通じて価格変動の機会を捉えます。主な利点は適応性と充実したリスク管理ですが、パラメータ選択や市場環境への適応性には最適化の余地があります。動的閾値と多次元のシグナル確認メカニズムを導入することで、戦略の安定性と信頼性がさらに向上することが期待されます。

Source

Pine

Strategy parameters

Comment

All comments (0)

No data

- 1