概要

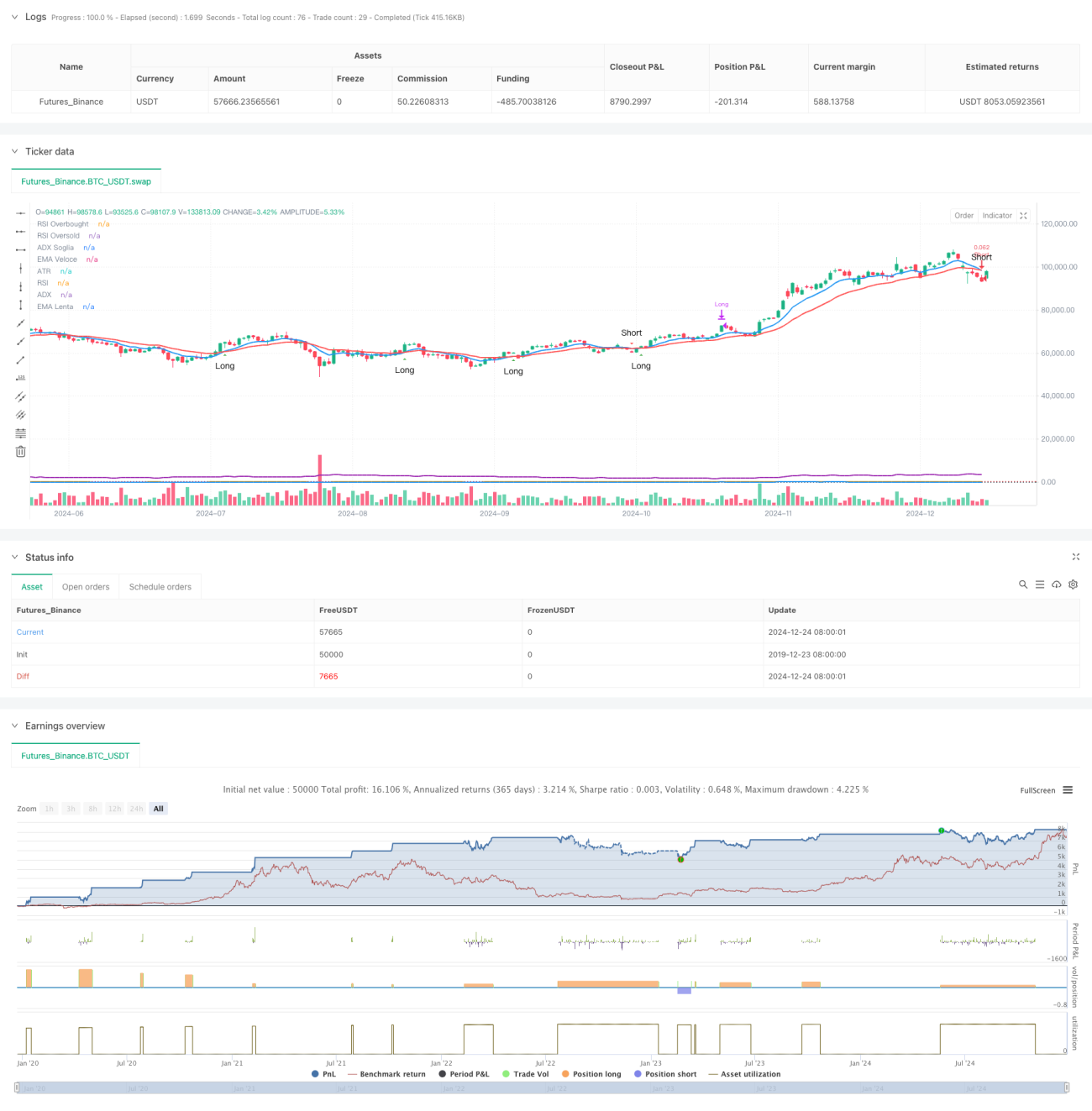

本戦略は、15分足の時間枠に基づく高頻度取引戦略です。指数移動平均線(EMA)、相対力指数(RSI)、平均方向性指数(ADX)、平均真のレンジ(ATR)など、複数のテクニカル指標を組み合わせ、それらの指標の相乗効果により取引シグナルを正確に捉え、リスクを動的に管理します。戦略は明確な可視化デザインを採用しており、トレーダーが市場状況や取引シグナルをリアルタイムで監視しやすくなっています。

戦略の原理

戦略の中核ロジックは、短期EMA(9期間)と長期EMA(21期間)のクロスにより取引シグナルを生成することです。RSI(14期間)は過剰な買われすぎ・売られすぎ領域をフィルタリングし、ADX(14期間)はトレンドの強さを確認し、ATR(14期間)は動的なストップロスと利益目標の設定に使用します。複数のテクニカル指標を組み合わせることで、取引シグナルの信頼性を確保しています。エントリー条件は以下の通りです:ロングは短期EMAが長期EMAを上抜け、かつRSIが70未満、ADXが20超。ショートは短期EMAが長期EMAを下抜け、かつRSIが30超、ADXが20超。エグジットにはATRに基づく動的ストップロスと利益目標の設定を使用します。

戦略の優位性

- シグナルの信頼性が高い:複数のテクニカル指標のクロス検証により、取引シグナルの精度が大幅に向上

- リスク管理が柔軟:ATRに基づく動的ストップロスと利益目標設定により、市場のボラティリティに応じて自動調整

- 取引機会が十分:15分足の時間枠により、豊富な取引機会を提供

- 可視化度が高い:明確なチャートレイアウトとシグナル表示により迅速な意思決定が可能

- 自動化度が高い:完全なシグナルシステムにより自動売買実行をサポート

戦略のリスク

- 市場変動リスク:高頻度取引は急激な変動相場でスリッページのリスクに直面する可能性

- 偽のブレイクアウトリスク:短期サイクルでは偽のシグナルが発生する可能性があり、ADXでフィルタリングする必要がある

- 資金管理リスク:頻繁な取引により手数料が累積する可能性があり、適切なポジション管理が必要

- テクニカルリスク:複数の指標が特定の市場条件下で矛盾したシグナルを生成する可能性

- 実行リスク:自動売買システムは安定したネットワーク環境と実行条件を必要とする

戦略の最適化方向性

- 指標パラメータの最適化:バックテストを通じて各指標パラメータを最適化し、特定の市場条件に適応させる

- シグナルフィルターの強化:出来高指標を補助的なフィルター条件として追加可能

- リスク管理の改善:動的ポジション管理システムを導入し、市場変動に応じて取引規模を調整

- 時間枠の最適化:市場局面に応じて取引時間枠を動的に調整

- ストップロス戦略の最適化:トレーリングストップ機構を導入し、利益保護能力を向上

まとめ

本戦略は、複数のテクニカル指標の相乗効果により、高頻度取引におけるシグナル捕捉とリスク管理のバランスを実現しています。明確な可視化デザインと完全な自動化サポートにより、実用性が高いといえます。継続的な最適化とリスク管理の改善により、戦略はさまざまな市場環境で安定したパフォーマンスを発揮することが期待されます。一定のリスクは存在しますが、適切なパラメータ設定とリスク管理措置により、これらのリスクは制御可能です。戦略を成功させるには、トレーダーが市場を深く理解し、リスクに継続的に注意を払うことが必要です。

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-25 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Scalping BTC Ottimizzato - Grafica Chiara", shorttitle="Scalp BTC Opt", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// === 📊 INPUTS ===- 1