多重移動平均線クロスとカマリラサポートレジスタンスを組み合わせたトレンド取引システム

1

Follow

1802

Followers

概要

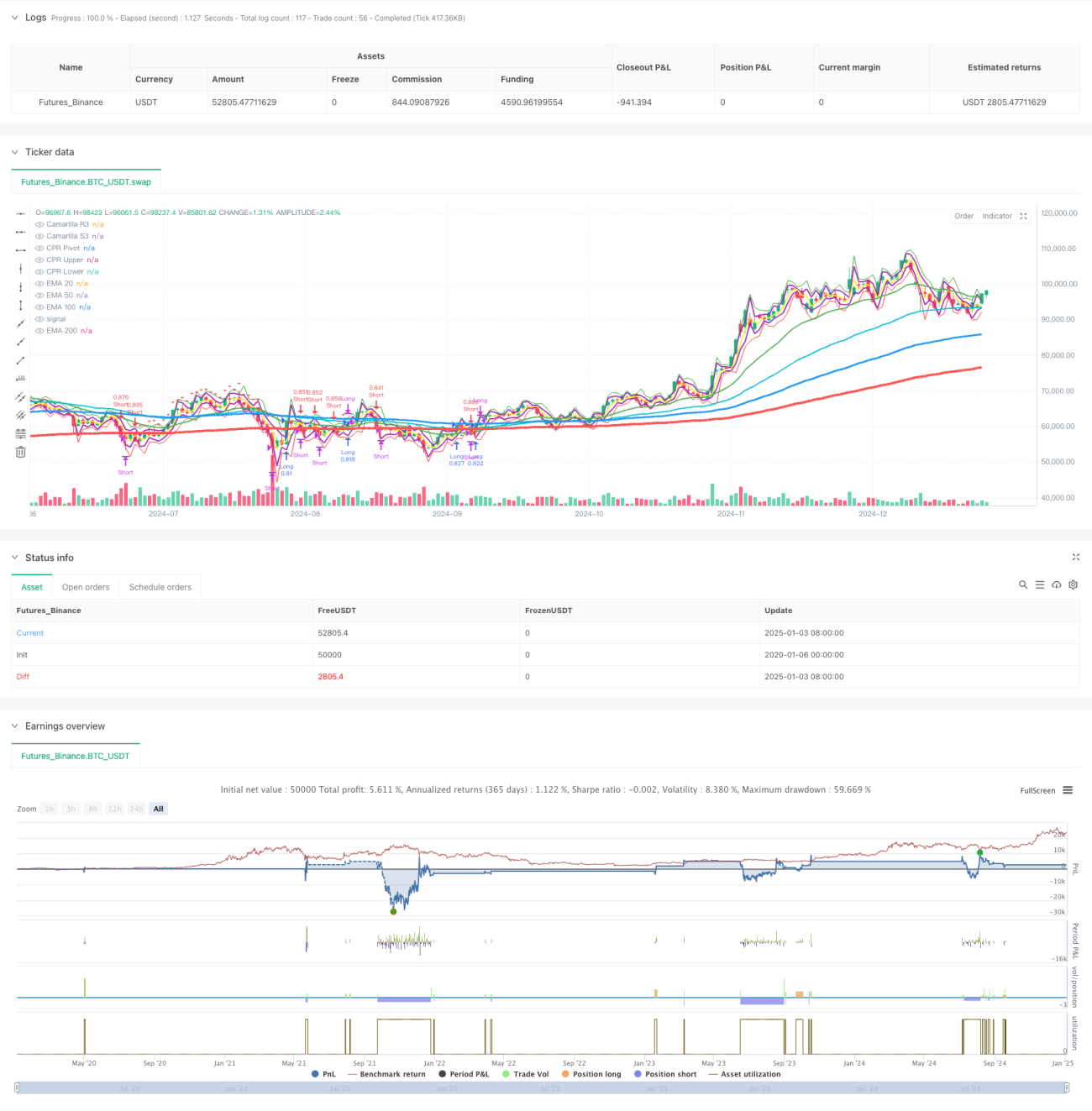

本戦略は、複数の指数移動平均線(EMA)、カマリラサポートレジスタンスレベル、および中心範囲(CPR)を組み合わせたトレンドフォロー型取引システムです。この戦略は、価格と複数の移動平均線の関係および重要な価格帯を分析することで、市場のトレンドと潜在的な取引機会を識別します。システムでは、パーセンテージポジションサイズや多様なエグジットメカニズムを含む、厳格な資金管理とリスク管理対策を採用しています。

戦略の原理

戦略は主に以下のコアコンポーネントに基づいています:

- 複数移動平均線システム(EMA20/50/100/200)は、トレンドの方向性と強さを確認するために使用されます。

- カマリラサポートレジスタンスレベル(R3/S3)は、重要な価格水準を特定するために使用されます。

- 中心範囲(CPR)は、日中の取引範囲を決定するために使用されます。

- エントリーシグナルは、価格とEMA200のクロス、およびEMA20の確認に基づいています。

- エグジット戦略は、固定ポイントとパーセンテージ移動の2つのモードを含みます。

- 資金管理システムは、口座規模に応じてポジションサイズを動的に調整します。

戦略の利点

- 多次元的なテクニカル指標の組み合わせにより、より信頼性の高い取引シグナルを提供します。

- 柔軟なエグジットメカニズムにより、さまざまな市場環境に適応します。

- 堅牢な資金管理システムがリスクを効果的に制御します。

- トレンドフォロー特性により、大きな相場変動を捉えることができます。

- 視覚化コンポーネントにより、トレーダーが市場構造を理解しやすくなります。

戦略のリスク

- レンジ相場では偽のシグナルが発生する可能性があります。

- 複数の指標により取引シグナルが遅れる可能性があります。

- 固定エグジットポイントは、ボラティリティの高い市場ではパフォーマンスが低下する可能性があります。

- ドローダウンに耐えるためには、ある程度の資金規模が必要です。

- 取引コストが戦略全体のリターンに影響を与える可能性があります。

戦略の最適化方向

- ボラティリティ指標を導入して、エントリー/エグジットパラメータを動的に調整します。

- 市場状態認識モジュールを追加して、さまざまな市場環境に適応します。

- 資金管理システムを最適化し、動的なポジション管理を導入します。

- 取引時間フィルターを追加して、シグナル品質を向上させます。

- 出来高分析を追加して、シグナルの信頼性を高めることを検討します。

まとめ

本戦略は、複数の古典的なテクニカル分析ツールを統合することで、完全な取引システムを構築しています。このシステムの利点は、多次元的な市場分析と厳格なリスク管理にありますが、同時にさまざまな市場環境への適応性に注意を払う必要があります。継続的な最適化と改善を通じて、戦略は安定性を維持しつつ収益性を向上させることが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1