ダイナミックトレーディング理論における指数移動平均と累積出来高期間のクロス戦略

1

Follow

1802

Followers

概要

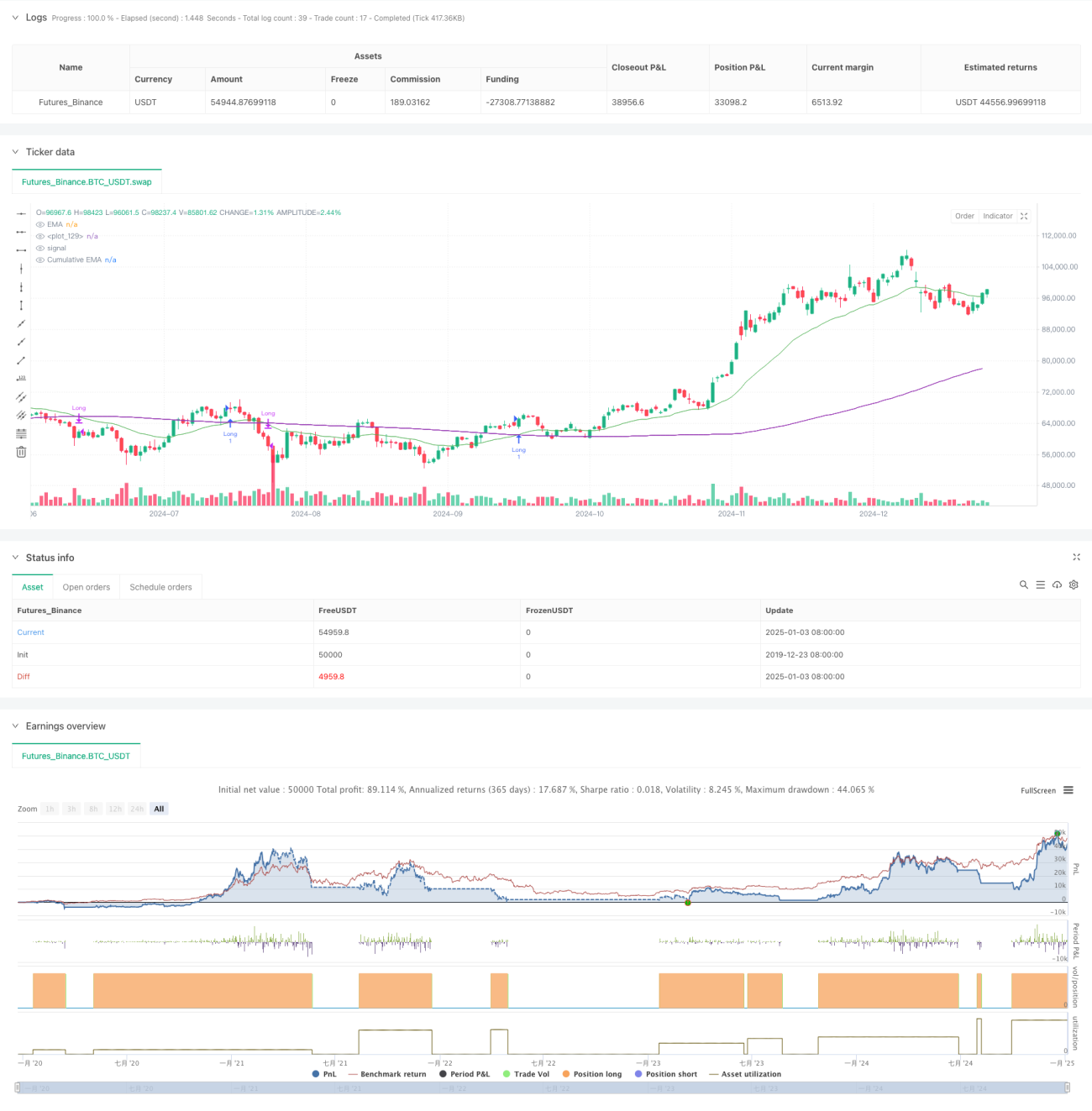

本戦略は、指数移動平均線(EMA)と累積出来高周期(CVP)を組み合わせた取引システムです。価格の指数移動平均と累積出来高加重価格のクロスを分析することで、市場トレンドの転換点を捉えます。戦略には時間フィルターが組み込まれており、取引時間帯を制限したり、取引時間終了時に自動的にポジションをクローズすることが可能です。また、逆クロスによるエグジットとカスタムCVPによるエグジットの2種類の異なるエグジット方法を提供し、柔軟性と適応性に優れています。

戦略の原理

戦略の中核ロジックは以下の主要な計算に基づきます:

- 平均価格(AVWP)の計算:高値、安値、終値の算術平均に出来高を乗じます。

- 累積出来高周期値の計算:設定された期間内で出来高加重価格を累積し、累積出来高で除算します。

- 終値のEMAとCVPのEMAをそれぞれ計算します。

- 価格EMAがCVPのEMAを上抜けた場合にロングシグナル、価格EMAがCVPのEMAを下抜けた場合にショートシグナルが発生します。

- エグジットシグナルは、逆クロスシグナル、またはカスタムCVP期間に基づくクロスシグナルとすることができます。

戦略の優位性

- シグナルシステムの堅牢性:価格トレンドと出来高情報を組み合わせることで、市場の動きをより正確に判断できます。

- 適応性の高さ:EMA期間やCVP期間を調整することで、様々な市場環境に適応できます。

- リスク管理の充実:時間フィルターを内蔵しており、不適切な取引時間帯の取引を回避できます。

- エグジットメカニズムの柔軟性:2種類の異なるエグジット方法を提供し、市場特性に応じて適切な方法を選択できます。

- 視覚化効果の高さ:シグナルマーカーやトレンド領域の塗りつぶしを含む、明確なグラフィカルインターフェースを提供します。

戦略のリスク

- 遅延リスク:EMA自体に一定の遅延があるため、エントリーやエグジットのタイミングがやや遅れる可能性があります。

- レンジ相場のリスク:横ばいのレンジ相場では、偽のシグナルが発生する可能性があります。

- パラメータ感応性:異なるパラメータの組み合わせにより、戦略のパフォーマンスが大きく異なる可能性があります。

- 流動性リスク:流動性の低い市場では、CVPの計算が正確でない可能性があります。

- タイムゾーン依存:戦略はニューヨーク時間を時間フィルターとして使用するため、異なる市場の取引時間の違いに注意が必要です。

戦略の最適化方向

- ボラティリティフィルターの導入:市場のボラティリティに応じて戦略パラメータを調整し、適応性を向上させます。

- 時間フィルターの最適化:複数の時間枠を追加し、取引時間帯をより細かく制御します。

- 出来高の品質評価の追加:出来高分析指標を取り入れ、質の低い出来高シグナルをフィルタリングします。

- 動的パラメータ調整:適応型パラメータシステムを開発し、市場条件に応じてEMAおよびCVP期間を自動調整します。

- 市場センチメント指標の追加:他のテクニカル指標と組み合わせて取引シグナルを確認します。

まとめ

本戦略は、構造が完全でロジックが明確な定量取引戦略です。EMAとCVPの利点を組み合わせることで、トレンドを捉えつつリスク管理に重点を置いた取引システムを構築しています。戦略のカスタマイズ性は高く、様々な市場環境での使用に適しています。最適化の提案を実施することで、戦略のパフォーマンスをさらに向上させる余地があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1