1

Follow

1802

Followers

概要

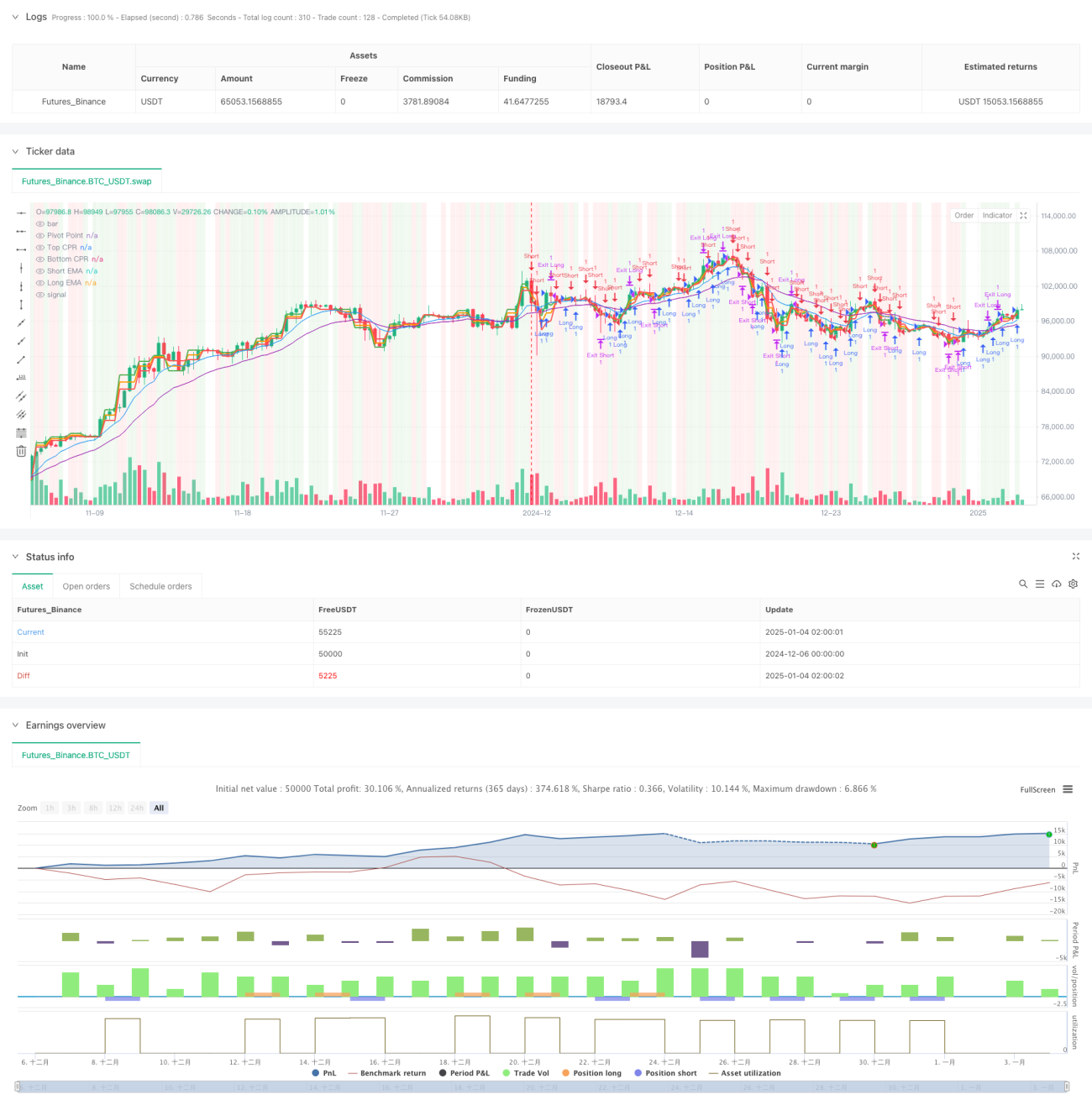

本戦略は、中枢点参考(CPR)、指数移動平均(EMA)、相対力指数(RSI)、およびブレイクアウトロジックを組み合わせた総合的なトレーディングシステムです。ATRを使用した動的トレーリングストップ機構を採用し、複数のテクニカル指標を連携させて市場のトレンドと取引機会を特定し、リスクの動的管理を実現します。本戦略はデイトレードおよび短期取引に適しており、適応性とリスク管理能力に優れています。

戦略の原理

戦略は主に以下のコアコンポーネントに基づいています:

- CPR指標は重要なサポート・レジスタンスレベルを特定するために使用され、日次サイクルのピボットポイント、上限、下限を計算します。

- デュアルEMAシステム(9日と21日)はトレンド方向を判断するために使用され、ゴールデンクロス・デッドクロスによって取引シグナルを生成します。

- RSI指標(14日)は市場の買われすぎ・売られすぎ状態を確認し、取引フィルターとして機能します。

- ブレイクアウトロジックは、価格のピボットポイント突破を組み合わせて取引シグナルを確定します。

- ATR指標は動的トレーリングストップを設定するために使用され、市場のボラティリティに応じてストップ距離を適応的に調整します。

戦略の利点

- 複数のテクニカル指標を総合的に活用することで、シグナルの信頼性が向上します。

- 動的トレーリングストップ機構により、利益を効果的に確保しリスクを制御できます。

- CPR指標は重要な価格参照点を提供し、市場構造の正確な把握に役立ちます。

- 戦略は適応性に優れており、異なる市場環境に応じてパラメータを調整できます。

- RSIフィルターとブレイクアウト確認により、取引シグナルの品質が向上します。

戦略のリスク

- 複数の指標はレンジ相場でラグや誤ったシグナルを生じる可能性があります。

- トレーリングストップは高ボラティリティ期間中に早期にトリガーされる可能性があります。

- パラメータ最適化には市場特性を考慮する必要があり、不適切なパラメータ設定は戦略のパフォーマンスに影響を与える可能性があります。

- シグナルの競合が発生した場合、意思決定の正確性に影響を与える可能性があります。

戦略の最適化方向

- 出来高指標を導入して価格ブレイクアウトの有効性を確認します。

- トレンド強度フィルターを追加し、トレンドフォローの精度を高めます。

- ストップロスパラメータの動的調整メカニズムを最適化し、保護効果を向上させます。

- 市場ボラティリティ適応メカニズムを追加し、取引パラメータを動的に調整します。

- センチメント指標の組み込みを検討し、市場タイミングの判断を改善します。

まとめ

本戦略は複数のテクニカル指標を連携させることで、比較的完全なトレーディングシステムを構築しています。動的ストップ機構と多面的なシグナル確認により、良好なリスク・リターン特性を提供します。戦略の最適化余地は主にシグナル品質の向上とリスク管理の完成にあります。継続的な最適化と調整により、本戦略はさまざまな市場環境で安定したパフォーマンスを維持することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1