1

Follow

1802

Followers

概要

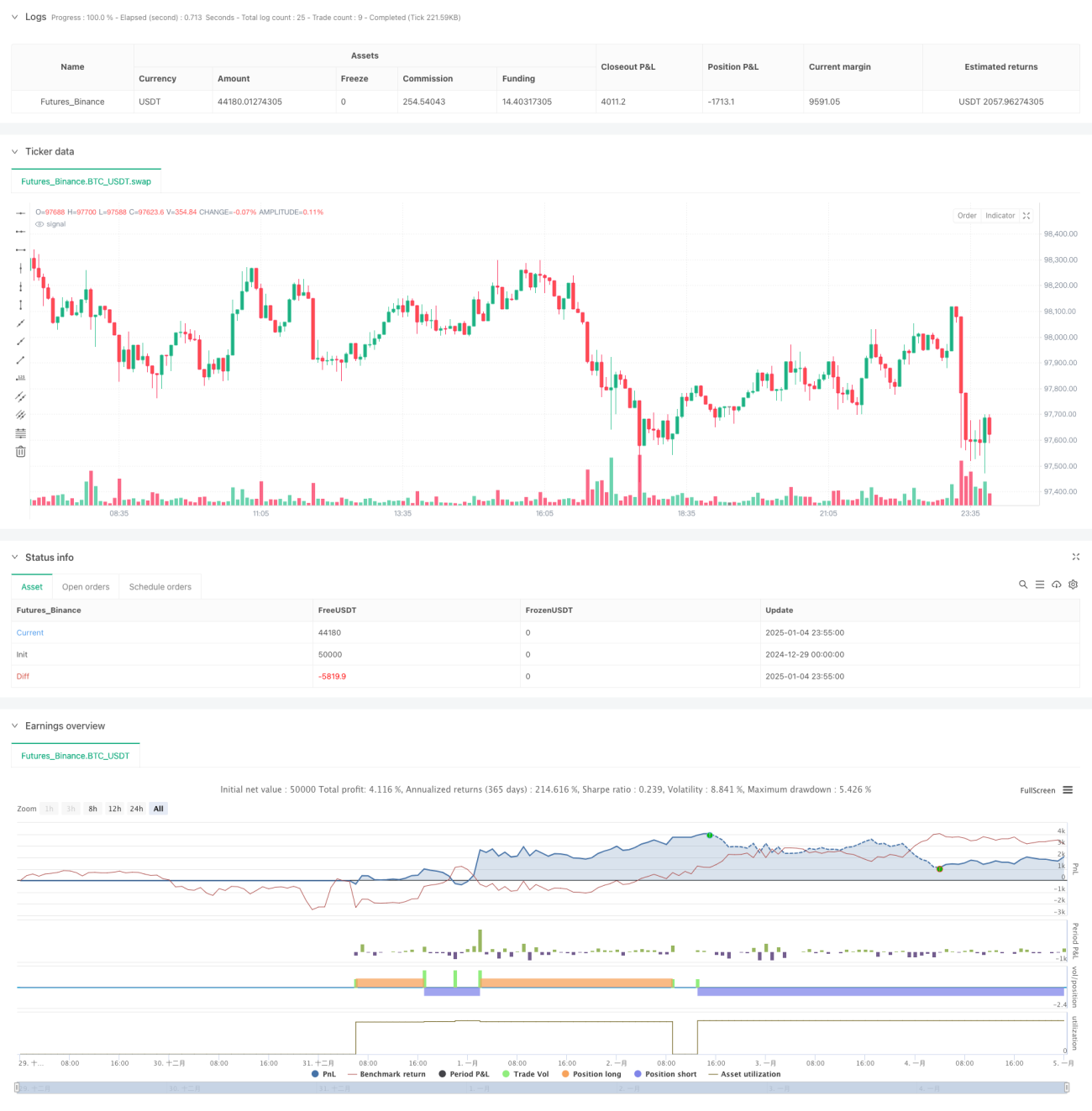

本戦略は、RSI(相対力指数)とCCI(順勢指標)を組み合わせた二重テクニカル分析取引システムです。これら2つの古典的指標の買われすぎ/売られすぎシグナルに、リスクリワード比と固定ストップロスを組み合わせることで、完全な取引判断フレームワークを構築します。戦略の核は、二重指標のクロス確認により取引シグナルの信頼性を高め、同時に堅牢なリスク管理体制を組み込んでいる点です。

戦略原理

本戦略は主に以下の核心原理に基づいて動作します:

- 14期間のRSI指標と20期間のCCI指標をシグナル生成の基盤として使用

- エントリーシグナルのトリガー条件:

- ロングエントリー:RSIが20未満(売られすぎ)かつCCIが-200未満

- ショートエントリー:RSIが80超(買われすぎ)かつCCIが200超

- リスク管理体制:

- 固定パーセンテージストップロス(デフォルト1%)を採用

- リスクリワード比(デフォルト2.0)に基づき利確位置を自動計算

- 可視化システム:

- チャート上に売買シグナルポイントをマーク

- ストップロス・利確ラインを描画

戦略の強み

- シグナルの信頼性が高い:RSIとCCIの二重確認メカニズムにより、偽シグナルを効果的にフィルタリング

- リスク管理が充実:固定ストップロスと動的利確の二重保護メカニズムを統合

- パラメータ調整が柔軟:主要指標のパラメータは市場特性に応じて最適化可能

- 視覚的フィードバックが明瞭:取引シグナルとリスク管理位置を直感的に表示

- 自動化度が高い:シグナル生成からポジション管理まで全自動実行

戦略のリスク

- シグナルの遅延性:テクニカル指標は本質的に遅延を持つため、最適なエントリーポイントを逃す可能性

- レンジ相場に不向き:ボックス相場では多くの偽シグナルが発生する可能性

- 固定ストップロスのリスク:一律のストップロス率はすべての市場環境に適切とは限らない

- パラメータ依存性:事前設定パラメータへの過度な依存により、市場環境変化時にパフォーマンスが低下する可能性

解決策:

- 市場ボラティリティに応じてパラメータを動的に調整

- トレンドフィルターを追加し、レンジ相場での偽シグナルを低減

- 適応型ストップロスメカニズムを導入

戦略の最適化方向性

- ボラティリティ指標の導入:

- ATRなどの指標を用いてストップロス距離を動的に調整

- ボラティリティに応じてRSI・CCIのトリガー閾値を調整

- トレンド確認メカニズムの追加:

- 移動平均線をトレンドフィルターとして追加

- トレンド強度指標を導入してエントリータイミングを最適化

- リスク管理の充実:

- 動的リスクリワード比の計算を実現

- 部分利確メカニズムを追加

- シグナル生成の最適化:

- 出来高確認メカニズムを追加

- 価格構造分析を導入

まとめ

本戦略は、古典的テクニカル指標と現代的なリスク管理コンセプトを組み合わせた完全な取引システムです。二重テクニカル指標の確認メカニズムによりシグナルの信頼性を高め、厳格なリスク管理措置と組み合わせることで、論理的で実用性の高い取引戦略を形成しています。一定の限界はあるものの、継続的な最適化と改善により、本戦略は実戦での応用可能性を有しています。今後、ボラティリティ感知、トレンド確認、リスク管理などの面で最適化を進めることで、戦略の安定性と実用性がさらに向上することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1