1

Follow

1802

Followers

概要

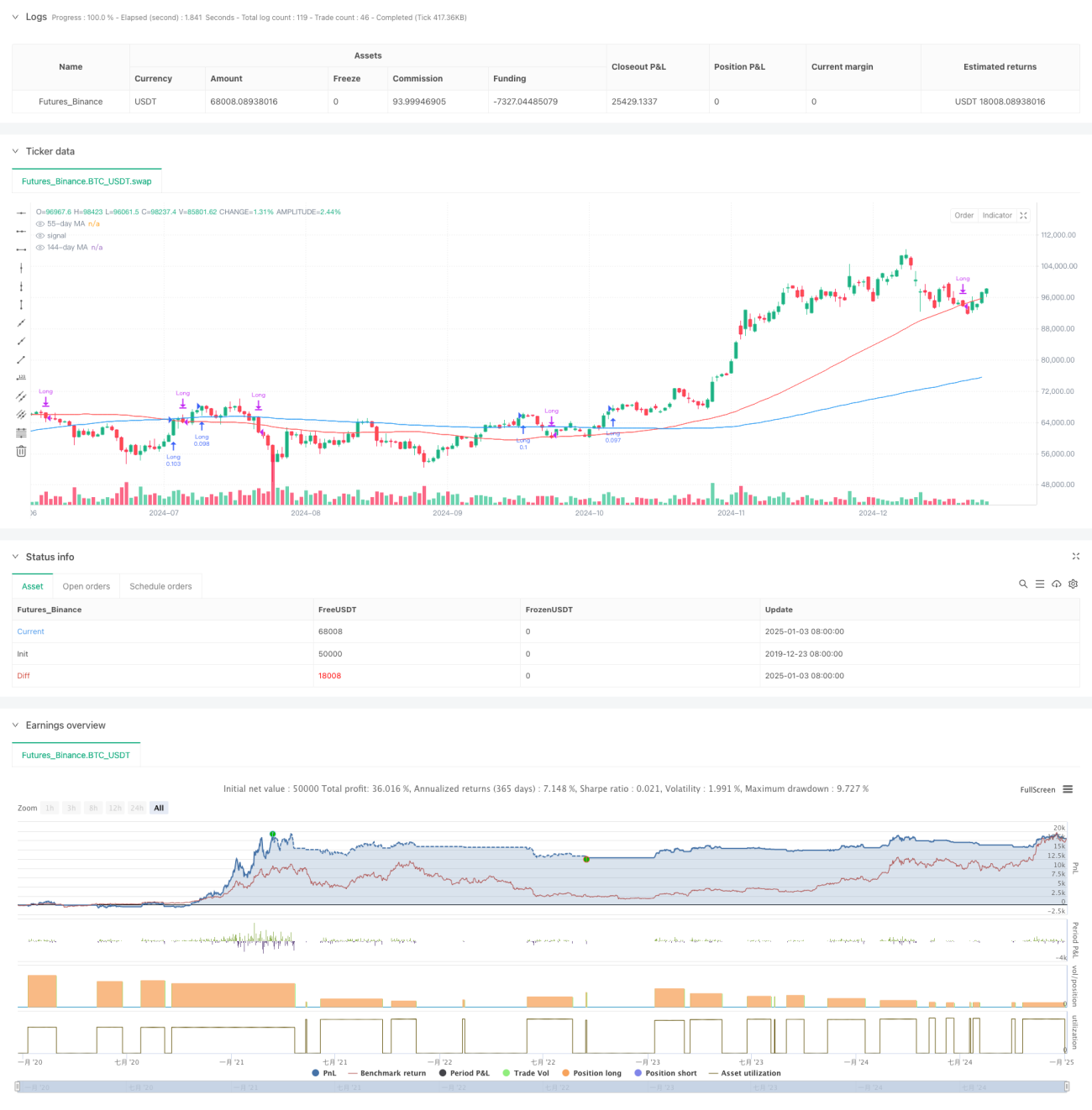

本戦略は、相対力指数(RSI)、移動平均線(MA)、および価格モメンタムを組み合わせた総合取引システムです。主にRSIのトレンド変化、複数時間枠の移動平均線のゴールデンクロス/デッドクロス、価格モメンタムの変化を監視して、潜在的な取引機会を特定します。特にRSIの上昇トレンドと価格の連続上昇に注目し、多重確認によって取引の精度を高めています。

戦略の原理

戦略のコアロジックは以下の主要コンポーネントに基づいています。

- RSIトレンド分析:期間13のRSIとその移動平均線を使用して価格の強さを確認

- 価格モメンタム確認:連続3回の高値更新(Higher Highs)の形成を要求し、上昇トレンドの持続性を検証

- 多重移動平均線システム:21日、55日、144日の移動平均線をトレンドフィルターとして使用

- 資金管理:1回の取引で口座資産の10%をポジションサイズとして使用

買い条件:RSIがその平均値を上回る、価格が連続高値を形成、RSIが上昇トレンドを維持していること

売り条件:価格が55日移動平均線を下回る、またはRSIが平均値を下回りかつ価格が55日移動平均線を下回ること

戦略の優位性

- 多重確認メカニズム:RSI、価格モメンタム、移動平均線システムによる多重検証で、取引シグナルの信頼性を向上

- トレンド追随能力:中長期的なトレンドを効果的に捉え、フェイクブレイクアウトを回避

- リスク管理が充実:ポジション管理と明確なストップロス条件によるリスクコントロール

- 適応性が高い:異なる時間枠や市場環境に適用可能

- 合理的な資金管理:口座資産の割合に基づくポジションサイズ管理により、固定ロットのリスクを回避

戦略のリスク

- ラグリスク:移動平均線やRSI指標は本質的に遅延が発生するため、エントリーやエグジットのタイミングがやや遅れる可能性がある

- レンジ相場リスク:ボックス相場では頻繁なフェイクシグナルが発生する恐れがある

- 連続損失リスク:相場の急変時には連続したストップロスに直面する可能性がある

解決策:

- 市場環境フィルターの追加

- 指標パラメータの最適化

- ボラティリティ適応メカニズムの導入

戦略の最適化方向性

- 指標パラメータの最適化:

- 適応型RSI期間の検討

- 市場サイクルに応じた移動平均線パラメータの調整

- 市場環境認識の追加:

- ボラティリティ指標の導入

- トレンド強度フィルターの追加

- リスク管理の強化:

- 動的ストップロスメカニズムの実装

- 利益目標管理の追加

- ポジション管理の最適化:

- シグナル強度に応じたポジションサイズの調整

- 分割建玉と減額メカニズムの実現

まとめ

本戦略は、テクニカル分析指標とモメンタム分析手法を総合的に活用し、比較的完成度の高い取引システムを構築しています。多重確認メカニズムと充実したリスク管理が主な強みですが、市場環境への適応性とパラメータ最適化の課題に注意する必要があります。継続的な最適化と改良により、本戦略は堅牢な取引システムとなる可能性を秘めています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1