ボルバー・インジケーターと出来高分位数フィルターに基づく多段階動的利確取引戦略

1

Follow

1802

Followers

概要

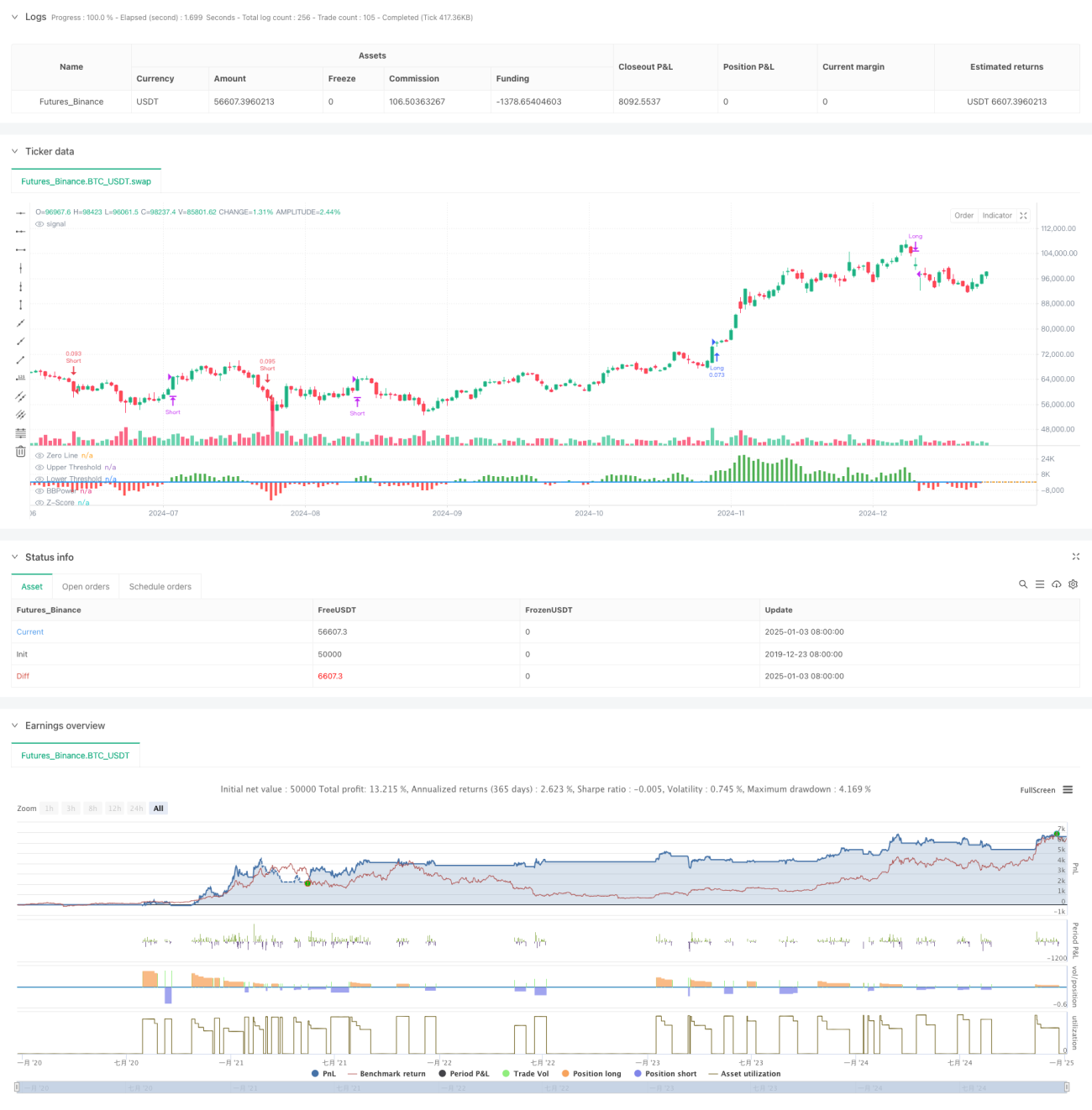

本戦略は、ブルベアパワー(Bull Bear Power)指標と出来高分位数に基づく多段階動的利確システムを組み合わせた、量化取引戦略です。価格、出来高、モメンタムなどの多次元データを分析することで、適応性が高くリスク管理可能な取引システムを構築します。中核となるロジックは、BBP指標のZスコア標準化値を取引シグナルのトリガー条件として使用し、同時に出来高分位数分析を活用して利確水準を動的に調整することで、市場の異なる変動状態を正確に捉えることです。

戦略の原理

戦略の中核計算は以下の主要部分から構成されます:

- BBP指標の計算:最高価格とEMAの差(強気の力)と最低価格とEMAの差(弱気の力)の和により、市場の力関係を測定します。

- Zスコア標準化:BBP値を標準化し、現在の市場の強弱度合いの乖離水準を判断します。

- 出来高分析:現在の出来高が移動平均に対する倍率を計算し、市場の活発度を判断します。

- 分位数分析:価格と出来高の過去分位数を計算し、市場状態の確率分布における位置を特定します。

- 動的利確:ATR、出来高分位数、価格分位数を総合的に評価したスコアに基づき、利確距離を動的に調整します。

戦略の優位性

- 多次元分析:価格モメンタム、出来高、市場ポジションを総合的に考慮し、より包括的な市場視点を提供します。

- 高い適応性:動的に調整される利確メカニズムにより、様々な市場環境に適応可能です。

- リスク分散:多段階利確戦略を採用し、異なる価格水準で利益を確定します。

- 確率的優位性:Zスコアと分位数分析により、統計的に有意な優位性を持ちます。

- 拡張性:戦略フレームワークは拡張性に優れ、必要に応じて新たな分析次元を追加可能です。

戦略のリスク

- パラメータ感応性:戦略は複数のパラメータを含み、市場環境に応じた最適化が必要です。

- 市場環境依存性:激しい変動やトレンド転換期にはパフォーマンスが低下する可能性があります。

- 執行スリッページ:多段階利確注文は執行スリッページの影響を受け、実質的な収益に影響を与える可能性があります。

- 計算の複雑性:複数の指標をリアルタイム計算するため、システム負荷が生じる可能性があります。

- 偽シグナルのリスク:レンジ相場では誤った取引シグナルが発生する可能性があります。

最適化の方向性

- パラメータの適応化:機械学習手法を導入し、パラメータの自動最適化を実現します。

- 市場予測:市場環境分類モジュールを追加し、不利な取引環境を事前に識別します。

- ストップロスの最適化:動的ストップロスメカニズムを導入し、リスク管理の精度を向上させます。

- シグナルフィルター:トレンド強度フィルターを追加し、偽シグナルを低減します。

- ポジション管理:ポジション配分アルゴリズムを最適化し、資金効率を向上させます。

まとめ

本戦略は、伝統的なBBP指標と現代的な量化分析手法を組み合わせることで、理論的な基盤が確かで実用性の高い取引システムを構築しています。多段階利確と動的調整メカニズムにより、収益とリスクのバランスを良好に保っています。一定のパラメータ最適化の難しさはあるものの、戦略フレームワークの拡張性により、今後の最適化の余地が十分にあります。実際の運用においては、トレーダーは自身の市場特性とリスク選好に応じて、調整を加えることを推奨します。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The BBP Strategy with Volume-Percentile TP by PresentTrading emerges as a sophisticated approach that integrates multiple analytical layers to enhance trading precision and profitability. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1