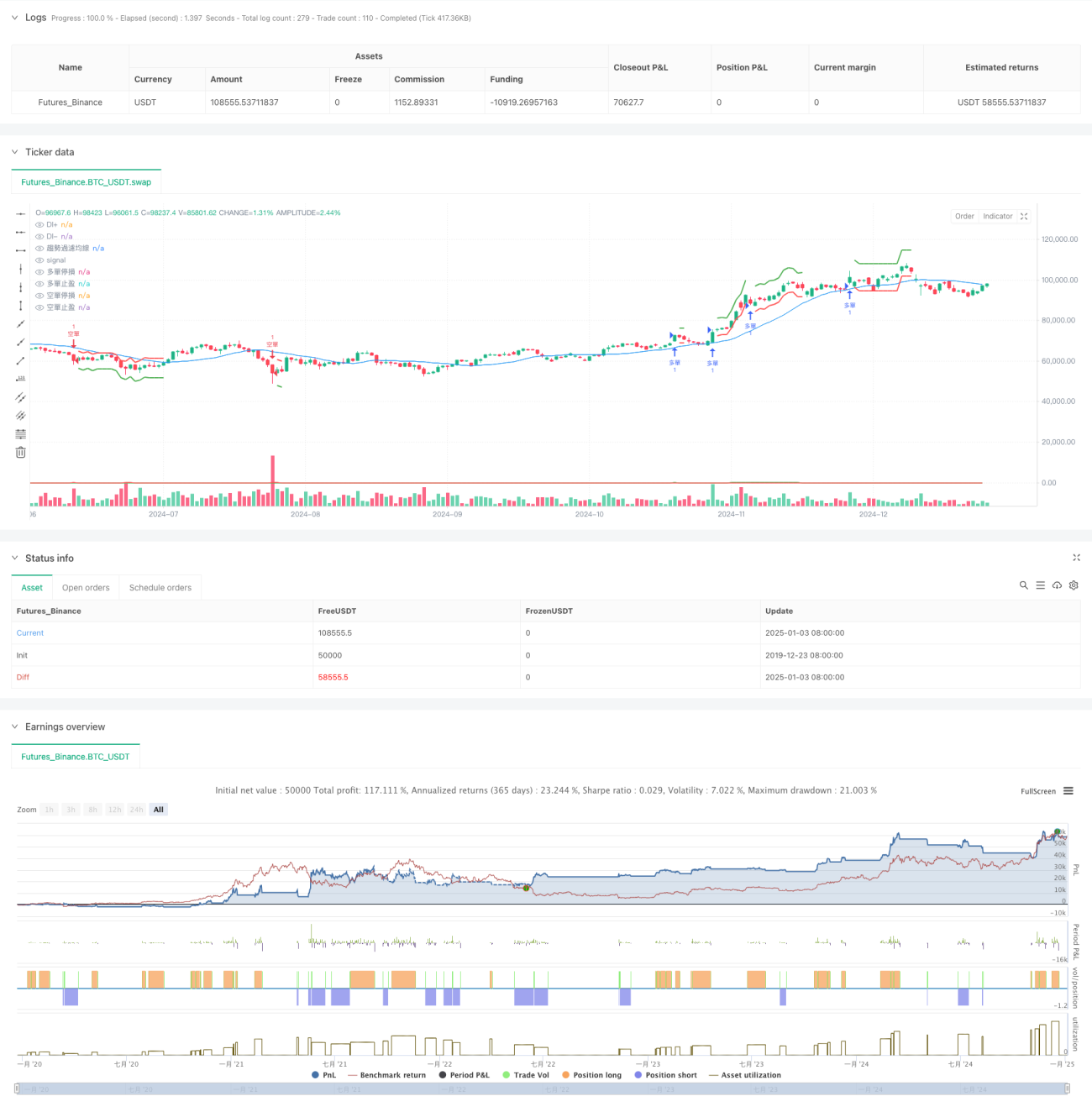

概要

本戦略は、方向性指標(DMI)と平均真実レンジ(ATR)を組み合わせたトレンドフォローシステムです。戦略の核は、DI+とDI-の指標を用いて市場のトレンド方向と強さを識別し、ATRを利用して利確・損切りの位置を動的に調整することです。トレンドフィルター移動平均線を補助確認として導入することで、シグナルの信頼性をさらに高めています。市場のボラティリティを十分に考慮した設計であり、適応性に優れています。

戦略の原理

戦略は以下の核心メカニズムに基づいて動作します:

- DI+およびDI-指標を使用してトレンドの方向と強さを測定します。DI+がDI-より高く、その差が閾値を超えた場合、上昇トレンドが成立していることを示し、逆の場合は下降トレンドを確認します。

- トレンドフィルター移動平均線(SMA)をトレンド確認ツールとして導入します。価格と移動平均線の位置が相互に確認された場合のみシグナルが発生します。

- ATR指標を利用して損切りと利確の位置を動的に計算し、リスク管理が異なる市場環境に適応できるようにします。

- 取引執行時に時間制限を厳守し、過度に頻繁な取引を避けます。

戦略の優位性

- 動的調整能力が高い – ATRにより市場のボラティリティに自己適応します。

- リスク管理が充実 – ボラティリティに基づく動的な損切り・利確メカニズムを設定しています。

- シグナルの信頼性が高い – 複数の指標によるクロス検証により、偽シグナルを低減します。

- パラメータが柔軟に調整可能 – 戦略パラメータは市場特性に応じて最適化できます。

- 執行ロジックが明確 – エントリーおよびエグジット条件が明確で、実運用に適しています。

戦略のリスク

-

レンジ相場のリスク – ボックス相場では連続した損切りが発生する可能性があります。

対策: レンジ指標によるフィルターを追加するか、パラメータ閾値を調整することを推奨します。 -

スリッページリスク – ボラティリティが高い局面では大きなスリッページに直面する可能性があります。

対策: 損切り幅をやや広く設定し、スリッページの余地を残すことを推奨します。 -

偽ブレイクアウトのリスク – トレンド転換点で誤判定が生じる可能性があります。

対策: 出来高などの指標と組み合わせてシグナルを確認することを推奨します。 -

パラメータ感応度 – 異なるパラメータの組み合わせで結果に大きな差が出ます。

対策: バックテストを通じて安定性の高いパラメータ範囲を見つけることを推奨します。

戦略の最適化方向

-

シグナル最適化 – ADX指標を導入してトレンド強度を評価するか、出来高確認メカニズムを追加することが考えられます。

-

ポジション管理 – トレンド強度に基づいて保有ポジションサイズを動的に調整し、より細やかなリスク管理を実現します。

-

時間軸 – 複数の時間足分析を検討し、シグナルの信頼性を高めます。

-

市場適応性 – 銘柄特性に応じて自己適応型パラメータ調整メカニズムを開発することが可能です。

まとめ

本戦略は、方向性指標とボラティリティ指標を組み合わせることで、トレンドの動的フォローとリスク管理を実現しています。実用性と運用可能性を重視した設計であり、市場への適応力も高いです。パラメータ最適化やシグナル改善により、さらなる向上の余地があります。投資家は実運用時に十分なテストを行い、具体的な市場特性に応じて調整することを推奨します。

- 1