1

Follow

1802

Followers

概要

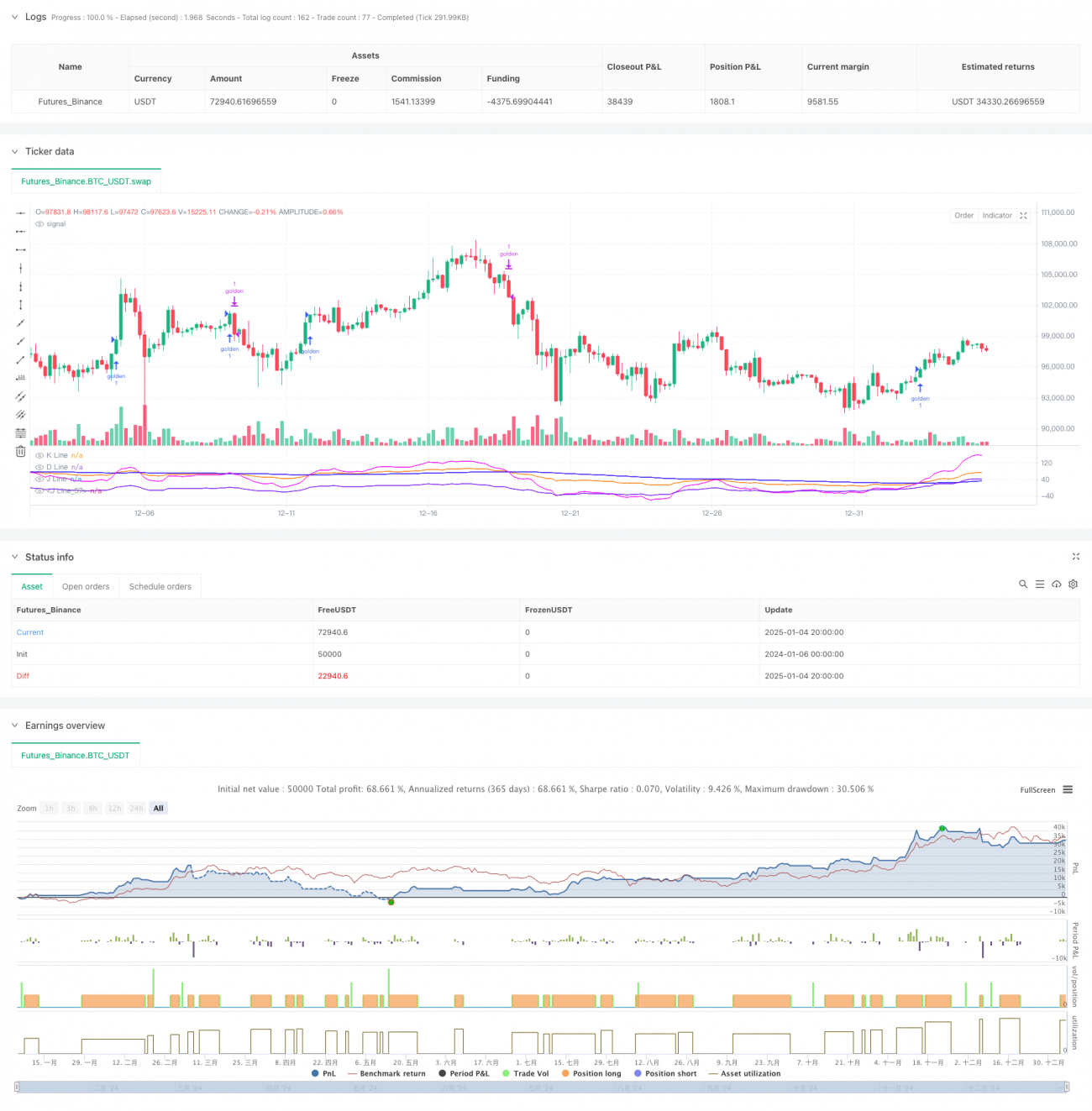

本戦略は、KDJインジケーターに基づく高度な取引システムであり、K線、D線、J線のクロスパターンを詳細に分析することで市場トレンドを捉えます。戦略にはカスタムのBCWSMA平滑化アルゴリズムが組み込まれており、確率的指標の最適化計算によって信号の信頼性を向上させています。また、ストップロスやトレーリングストップロスといった厳格なリスク管理メカニズムを採用し、堅実な資金管理を実現しています。

戦略原理

戦略の核となるロジックは、以下の主要要素に基づいています。

- カスタムBCWSMA(加重移動平均)アルゴリズムを使用してKDJインジケーターを計算し、指標の平滑性と安定性を向上させます。

- RSV(未成熟確率値)の計算により、価格を0~100の範囲の数値に変換し、高値と安値の間での価格位置をより適切に反映します。

- 独自のJ線とJ5線(派生指標)のクロス検証メカニズムを設計し、多重確認によって取引シグナルの精度を高めます。

- 持続性に基づくトレンド確認メカニズムを確立し、J線がD線より上に3日連続で維持された場合にのみトレンドの有効性を確認します。

- パーセンテージストップロスとトレーリングストップロスを組み合わせた複合リスク管理システムを統合しています。

戦略の優位性

- シグナル生成メカニズムが先進的:複数のテクニカル指標のクロス検証により、偽のシグナルの影響を大幅に低減します。

- リスク管理が充実:固定ストップロスやトレーリングストップロスなど、多層的なリスク管理メカニズムを採用し、下落リスクを効果的に抑制します。

- パラメータの調整が容易:KDJ期間、シグナル平滑化係数などの主要パラメータは、市場状況に応じて柔軟に調整可能です。

- 計算効率が高い:最適化されたBCWSMAアルゴリズムを使用することで、計算の複雑さを抑え、戦略実行の効率を向上させます。

- 適応性が良好:異なる市場環境に適応でき、パラメータ調整によって戦略パフォーマンスを最適化できます。

戦略のリスク

- 相場変動リスク:レンジ相場では頻繁な偽のブレイクアウトシグナルが発生し、取引コストが増加する可能性があります。

- ラグリスク:移動平均による平滑化処理のため、シグナルにある程度の遅れが生じる可能性があります。

- パラメータ感応度:戦略の効果はパラメータ設定に大きく依存し、不適切なパラメータ設定は戦略のパフォーマンスを著しく低下させる可能性があります。

- 市場環境依存性:特定の市場環境では、戦略のパフォーマンスが十分に発揮されない場合があります。

戦略の最適化方向

- シグナルフィルタリングメカニズムの最適化:出来高やボラティリティなどの補助指標を導入することで、シグナルの信頼性を高めることができます。

- 動的パラメータ調整:市場の変動状況に応じてKDJパラメータやストップロスパラメータを動的に調整します。

- 市場環境の識別:市場環境判断モジュールを追加し、異なる市場環境で異なる取引戦略を採用します。

- リスク管理の強化:最大ドローダウン制御やポジション保有期間制限などの追加リスク管理手段を導入できます。

- パフォーマンスの最適化:BCWSMAアルゴリズムをさらに最適化し、計算効率を向上させます。

まとめ

本戦略は、革新的なテクニカル指標の組み合わせと厳格なリスク管理により、完全な取引システムを構築しています。戦略の主な強みは、多重シグナル確認メカニズムと充実したリスク管理システムですが、パラメータ最適化や市場環境への適応性にも注意が必要です。継続的な最適化と改良により、本戦略は様々な市場環境で安定したパフォーマンスを維持できる可能性があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1