1

Follow

1802

Followers

概要

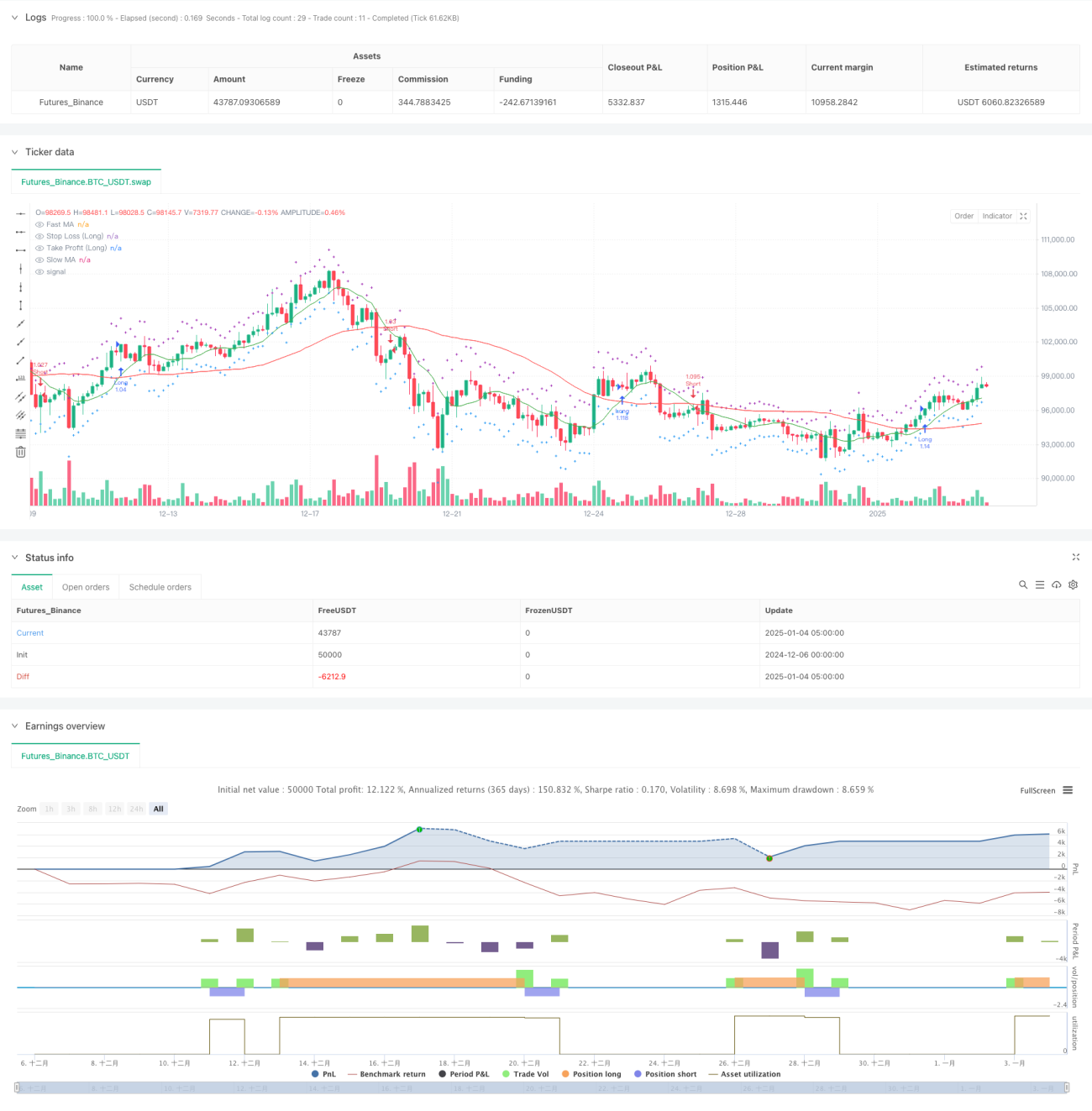

本戦略は、移動平均線のクロスシグナルとATRリスク管理を組み合わせたトレンドフォロー型取引システムです。短期と長期の移動平均線のクロスを利用して市場トレンドを捉え、同時にATR指標でストップロスと利益確定水準を動的に調整し、取引リスクを精密にコントロールします。さらに、資金管理モジュールを備えており、口座残高と事前設定されたリスクパラメータに基づいてポジションサイズを自動調整します。

戦略原理

戦略の核となるロジックは、以下の主要コンポーネントに基づいています。

- トレンド識別システム - 10期間と50期間の単純移動平均線(SMA)のクロスを使用してトレンド方向を判断します。短期移動平均線が長期移動平均線を上回った場合はロングシグナル、下回った場合はショートシグナルを生成します。

- リスク管理システム - 14期間のATR指標に1.5倍の係数を掛けて、動的なストップロスと利益確定目標を設定します。この手法により、市場のボラティリティに応じてリスク管理パラメータを自動調整できます。

- 資金管理システム - リスク許容度(2%)と資金配分比率(100%)を設定することで、1回の取引で使用する資金量を管理し、資金使用の合理性を確保します。

戦略の利点

- 適応性が高い - ATRでストップロスと利益確定水準を動的に調整することで、様々な市場環境に適応できます。

- リスク管理が充実 - パーセンテージリスク管理とATR動的ストップロスを組み合わせることで、二重のリスク防御機構を形成します。

- 操作ルールが明確 - エントリーとエグジットの条件が明確で、実行やバックテストが容易です。

- 資金管理が科学的 - 比率配分メカニズムにより、1回の取引リスクを管理可能な範囲に抑えます。

戦略のリスク

- レンジ相場リスク - 横ばいのレンジ相場では、移動平均線のクロスシグナルが頻発し、連続したストップロスが発生する可能性があります。

- スリッページリスク - 市場が急変動する際、実際の約定価格がシグナル価格と大きく乖離する可能性があります。

- 資金効率のリスク - 100%の資金配分比率では、資金使用効率が柔軟性を欠く可能性があります。

戦略の最適化方向

- トレンドフィルターの追加 - ADXなどのトレンド強度指標を追加し、強いトレンド時のみ取引を実行する。

- 移動平均線パラメータの最適化 - 過去データをテストし、最適な移動平均線期間の組み合わせを探索する。

- 資金管理の改善 - 動的なポジションサイズ調整メカニズムを追加し、口座の損益状況に応じて取引規模を自動調整することを推奨。

- 市場環境フィルターの追加 - ボラティリティ指標を追加し、適切な市場環境でのみ取引を実行する。

まとめ

本戦略は、移動平均線のクロスでトレンドを捉え、ATR動的リスク管理を組み合わせることで、完全なトレンドフォロー型取引システムを実現しています。戦略の利点はその適応性とリスク管理能力にありますが、レンジ相場ではパフォーマンスが低下する可能性があります。トレンドフィルターの追加と資金管理システムの最適化により、戦略全体のパフォーマンスはさらに向上する余地があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1