フィボナッチ数列に基づく適応的ボリンジャーバンド戦略の解説

1

Follow

1802

Followers

概要

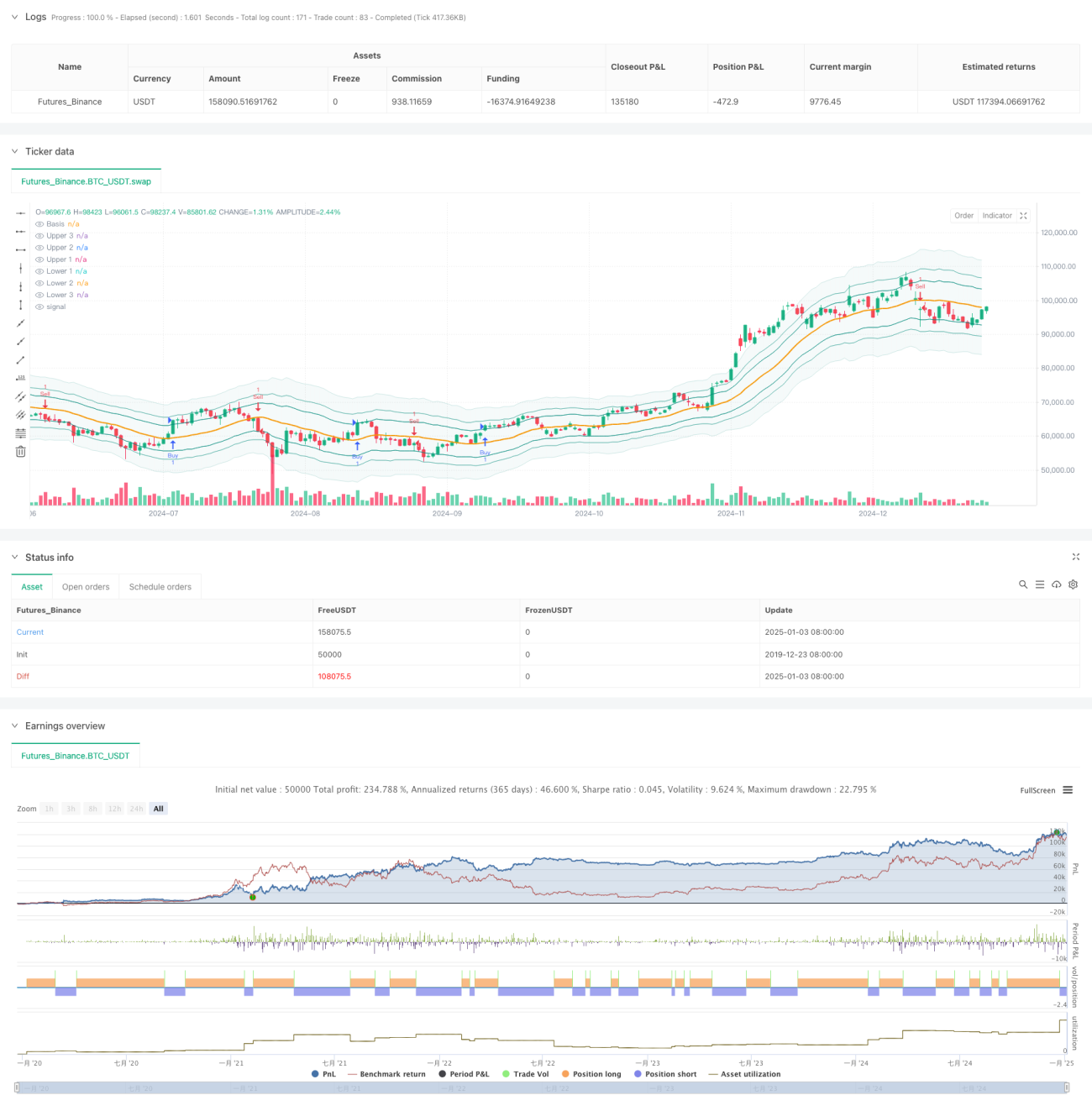

本戦略は、フィボナッチ数列とボリンジャーバンドを組み合わせた革新的な取引システムです。従来のボリンジャーバンドの標準偏差倍率をフィボナッチ比率(1.618、2.618、4.236)に置き換えることで、独自の価格変動レンジ判断システムを構築しています。戦略には、利益確定・損切りの設定や取引時間枠フィルターなどの完全な取引管理機能が含まれており、実用性と柔軟性に優れています。

戦略の原理

戦略の中核ロジックは、価格とフィボナッチボリンジャーバンドの相互作用に基づいています。まず、価格の単純移動平均線(SMA)を中央バンドとして計算し、ATRに異なるフィボナッチ比率を乗じて上下のバンドを形成します。価格がユーザーが選択したフィボナッチ帯域を突破した場合、取引シグナルが生成されます。具体的には、最安値が目標買い帯域を下回り、最高値がその帯域を上回った場合にロングシグナルが発生し、最安値が目標売り帯域を下回り、最高値がその帯域を上回った場合にショートシグナルが発生します。

戦略の優位性

- 適応性の高さ:ATRを使用してバンド幅を動的に調整するため、様々な市場環境に適応できます。

- 柔軟性の高さ:ユーザーは取引スタイルに応じて異なるフィボナッチ帯域を取引シグナルとして選択できます。

- リスク管理の充実:利益確定・損切り機能や時間フィルター機能が組み込まれており、リスクを効果的にコントロールできます。

- 視覚的な直感性:異なる透明度の帯域表示により、トレーダーが市場構造を理解しやすくなります。

- 計算ロジックの明確さ:古典的なテクニカル指標の組み合わせを使用しており、理解とメンテナンスが容易です。

戦略のリスク

- 偽のブレイクアウトリスク:価格が突破した直後に反落し、偽のシグナルが発生する可能性があります。

- パラメータ感度:異なるフィボナッチ比率の選択が戦略のパフォーマンスに大きく影響します。

- 時間依存性:取引時間枠を有効にした場合、重要な取引機会を逃す可能性があります。

- 市場環境依存性:レンジ相場では過剰な取引シグナルが発生する可能性があります。

戦略の最適化方向性

- シグナル確認メカニズム:出来高やモメンタム指標をブレイクアウトの確認として追加することを推奨します。

- 動的パラメータ最適化:市場のボラティリティに応じてフィボナッチ比率を自動調整できます。

- 市場環境フィルター:トレンド判断機能を追加し、異なる市場環境で異なるパラメータを使用します。

- シグナル重み付けシステム:複数の時間枠分析を構築し、シグナルの信頼性を高めます。

- ポジション管理最適化:市場のボラティリティやシグナルの強さに応じてポジションサイズを動的に調整します。

まとめ

本戦略は、古典的なテクニカル分析ツールを革新的に組み合わせたもので、フィボナッチ数列を用いて従来のボリンジャーバンド戦略を最適化しています。主な優位性は適応性と柔軟性にありますが、使用時にはパラメータの選択と市場環境とのマッチングに注意が必要です。追加の確認指標やシグナル生成メカニズムの最適化により、本戦略にはさらに改良の余地があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1