1

Follow

1802

Followers

概要

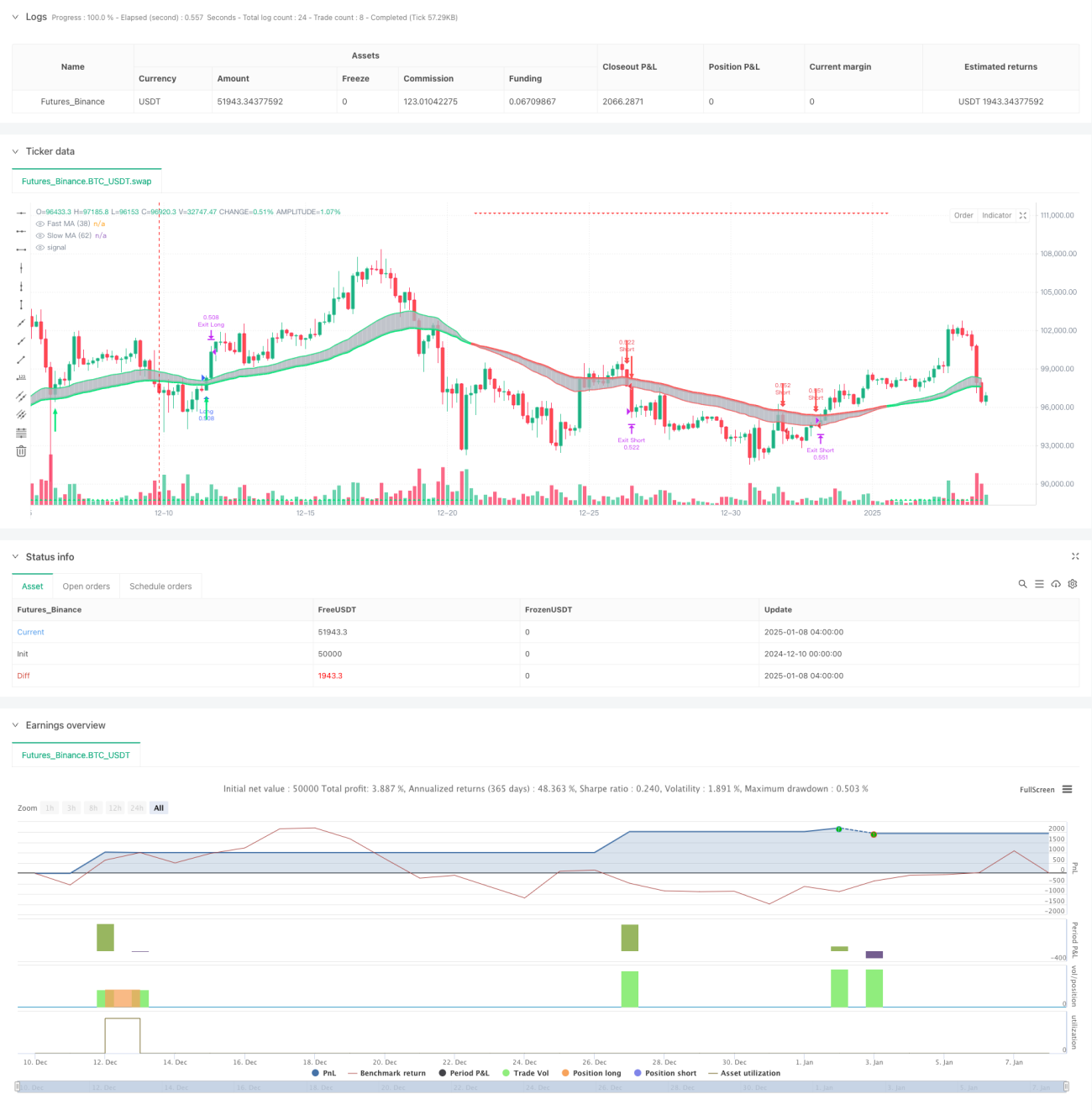

本戦略は、二重移動平均線システムとATR動的ストップロスを組み合わせたトレンドフォロー型取引システムです。38期間と62期間の指数平滑移動平均線(EMA)を用いて市場トレンドを識別し、価格と短期EMAのクロスによりエントリーシグナルを決定し、ATR指標による動的ストップロス管理を行います。また、攻撃的モードと保守的モードの2つの取引モードを提供し、異なるリスク選好のトレーダーに対応します。

戦略の原理

戦略の核となるロジックは以下の主要要素に基づいています:

- トレンド判定:38期間と62期間のEMAの位置関係により現在の市場トレンドを判断します。短期EMAが長期EMAの上にある場合は上昇トレンド、その逆は下降トレンドとします。

- エントリーシグナル:上昇トレンドにおいて、価格が下から短期EMAを突破したときにロングシグナルが発生します。下降トレンドにおいて、価格が上から短期EMAを下回ったときにショートシグナルが発生します。

- リスク管理:ATRに基づく動的ストップロスシステムを採用し、価格が有利に動くにつれてストップロス位置も調整され、既存の利益を保護すると同時に早期離脱を防ぎます。また、固定比率のストップロスと利確目標も設定します。

戦略の利点

- 優れたトレンドフォロー性能:二重移動平均線システムにより、中長期トレンドを効果的に捉え、レンジ相場での頻繁な取引を回避できます。

- 充実したリスク管理:固定ストップロスと動的ストップロスを組み合わせることで、最大リスクを制限しつつ利益を保護します。

- 適応性の高さ:攻撃的モードと保守的モードの2つの取引モードを提供し、市場環境や個人のリスク選好に応じて柔軟に調整できます。

- 明確な視覚的フィードバック:異なる色のローソク足や矢印マークにより、市場の状態や取引シグナルを直感的に表示します。

戦略のリスク

- トレンド転換リスク:トレンド転換点では連続ストップロスが発生する可能性があります。トレンドが明確になった時点での取引を推奨します。

- スリッページリスク:市場の変動が激しい場合、実際の約定価格がシグナル価格と大きく乖離する可能性があります。ストップロス範囲を適度に広げるべきです。

- パラメータ感応性:移動平均線の期間やATR倍率の選択は戦略のパフォーマンスに大きく影響します。市場環境に応じて最適化する必要があります。

戦略の最適化方向

- トレンド強度フィルターの追加:ADXなどのトレンド強度指標を導入し、トレンドが明確な場合のみエントリーします。

- ストップロスメカニズムの最適化:ボラティリティに応じてATR倍率を動的に調整し、ストップロスの適応性を高めます。

- 出来高確認の追加:エントリーシグナル発生時に出来高分析を組み合わせ、シグナルの信頼性を向上させます。

- 市場環境分類:市場環境(トレンド/レンジ)に応じて戦略パラメータを動的に調整します。

まとめ

本戦略は、古典的な二重移動平均線システムと最新の動的ストップロス技術を組み合わせることで、包括的なトレンドフォロー型取引システムを構築しています。リスク管理の充実と適応性の高さが戦略の利点ですが、トレーダーは具体的な市場環境に応じてパラメータの最適化とリスク管理を行う必要があります。提案された最適化方向に従うことで、戦略の安定性と収益性のさらなる向上が期待できます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1