動的トレンド追跡と移動平均線補助によるSuperTrend三重最適化戦略

1

Follow

1802

Followers

概要

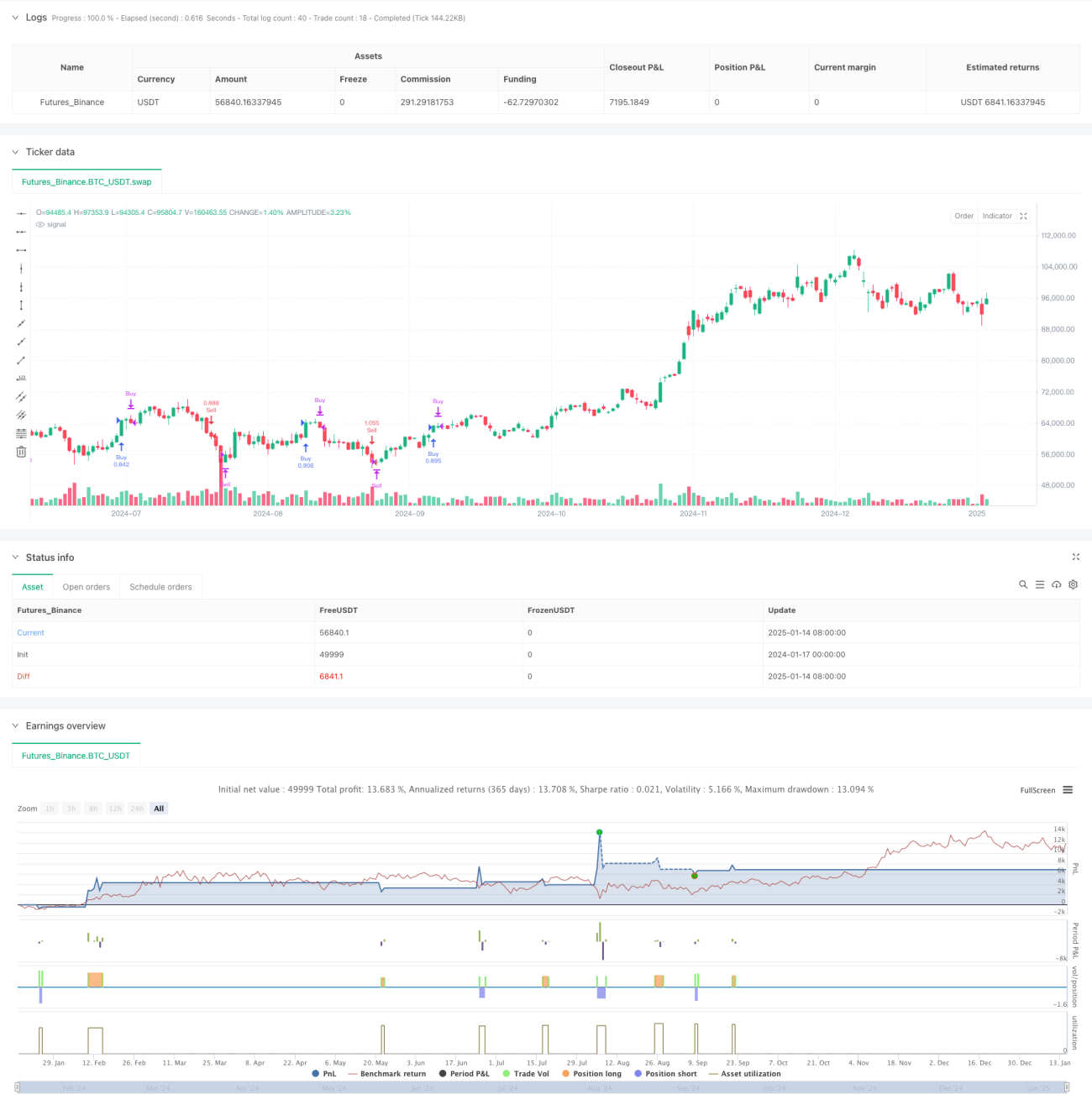

本戦略は、SuperTrend指標、指数移動平均線(EMA)、および平均真のレンジ(ATR)に基づくトレンドフォロー戦略です。複数のテクニカル指標を組み合わせ、初期ストップロスとトレーリングストップロスを併用することで、市場トレンドの動的追跡とリスク管理を実現します。戦略の中核は、SuperTrend指標でトレンド方向の変化を捉え、EMAでトレンドを確認し、二重のストップロス機構で利益を保護することにあります。

戦略の原理

戦略は以下の主要コンポーネントで動作します:

- SuperTrend指標はトレンド方向の変化を識別するために使用され、ATR期間16、係数3.02で計算されます

- 49期間のEMAはトレンドフィルターとして機能し、トレンド方向を確認します

- 初期ストップロスは50ポイントに設定され、各取引に基本的な保護を提供します

- トレーリングストップロスは利益が70ポイントに達した後に発動し、価格変動を動的に追跡します

SuperTrend方向が下向きに転換し、終値がEMAより上にある場合、ポジションがない状態で買いシグナルが発生します。逆に、SuperTrend方向が上向きに転換し、終値がEMAより下にある場合、売りシグナルが発生します。

戦略のメリット

- 多重確認メカニズム:SuperTrendとEMAの併用により、偽シグナルの影響を低減

- 充実したリスク管理:固定ストップロスと動的トレーリングストップロスの二重機構

- 柔軟なポジション管理:戦略はデフォルトで口座純資産の15%を保有比率とし、必要に応じて調整可能

- トレンド適応性:異なる市場環境に適応し、特に変動の大きな市場に適する

- パラメータ最適化可能性:主要パラメータは市場特性に応じて最適化調整可能

戦略のリスク

- レンジ相場リスク:横ばい相場では頻繁に取引が発生し、連続ストップロスにつながる可能性

- スリッページリスク:急激な相場変動時、ストップロスの執行価格が想定から大きく乖離する可能性

- パラメータ感応度:戦略効果はパラメータ設定に敏感で、市場環境によって調整が必要

- トレンド転換リスク:トレンド転換点では大きなドローダウンが発生してからストップロスが発動する可能性

- 資金管理リスク:固定比率のポジション管理は急激な変動時に大きなリスクをもたらす可能性

戦略の最適化方向

- 動的パラメータ調整:市場ボラティリティに応じてSuperTrendとEMAのパラメータを自動調整

- 市場環境フィルター:市場環境判断メカニズムを追加し、不適切な市場では取引を停止

- ストップロス最適化:ATRベースの動的ストップロス設定を導入し、市場変動に適応

- ポジション管理最適化:ボラティリティベースの動的ポジション管理システムを開発

- 利確目標の追加:市場変動に基づく動的利益確定目標を設定

まとめ

本戦略は、複数のテクニカル指標とリスク管理メカニズムを組み合わせた完全な取引戦略です。SuperTrendでトレンドを捉え、EMAで方向を確認し、二重のストップロス機構を併用することで、良好なリスクリターン比を実現します。最適化の余地は主にパラメータの動的調整、市場環境の判断、リスク管理システムの改善にあります。実際の運用では、十分な過去データによるバックテストを実施し、取引対象の特性に応じてパラメータを調整することを推奨します。

Source

Pine

/*backtest

start: 2024-01-17 00:00:00

end: 2025-01-15 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

//@version=5

strategy(" nifty supertrend triton", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input parametersStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1