1

Follow

1802

Followers

概要

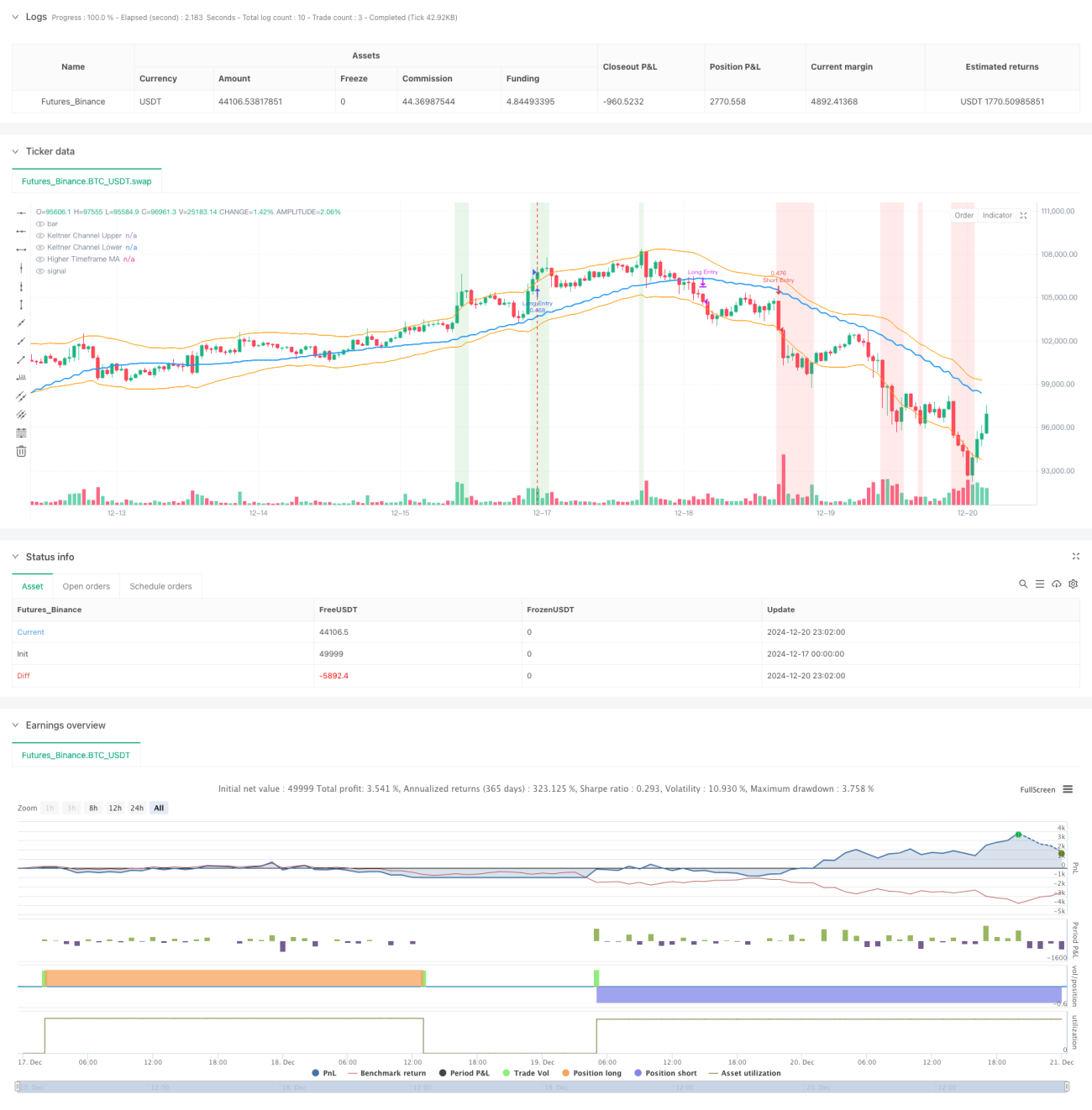

本戦略は、ケルトナーチャネル(Keltner Channel)と動的なサポート・レジスタンスラインを組み合わせた複合取引システムです。複数の時間枠の分析に移動平均線とボラティリティ指標を組み合わせることで、総合的な取引判断の枠組みを構築しています。戦略の核心は、価格が重要なテクニカル水準をブレイクするタイミングを識別し、市場のトレンドやボラティリティを考慮することで、確率の高い取引機会を捉えることにあります。

戦略の仕組み

戦略は多層のテクニカル指標体系を用いて分析を行います:

- 21期間のケルトナーチャネルを主たるトレンド判断ツールとして使用し、チャネル幅はATR値で決定します。

- 左側21本、右側8本のローソク足から重要なサポート・レジスタンスラインを算出します。

- 上位時間枠の移動平均線をトレンドフィルターとして導入します。

- 短期(5期間)と長期(30期間)の移動平均線を組み合わせてエントリーのタイミングを判断します。

- ATRを利用してストップロス水準を動的に調整します。

戦略のメリット

- 多角的なテクニカル指標が相互に検証し合うことで、偽シグナルを効果的に低減します。

- 動的なサポート・レジスタンスラインがリアルタイムで更新され、市場の変化に適応します。

- 上位時間枠の分析により、副次的な相場変動をフィルタリングします。

- 異なる時間枠に応じてストップロスパラメータを柔軟に調整できます。

- パーセンテージポジション管理を採用し、リスクを効果的にコントロールします。

戦略のリスク

- レンジ相場では取引シグナルが頻発する可能性があります。

- 複数の指標による検証により、一部の取引機会を逃す可能性があります。

- パラメータ最適化にはオーバーフィッティングのリスクがあります。

- 高ボラティリティ環境ではストップロス水準が広くなりすぎる可能性があります。

- 市場が急変した場合、サポート・レジスタンスラインが機能しなくなる可能性があります。

戦略の最適化方向

- 出来高指標を導入し、ブレイクの確度を補助的に判断します。

- 市場のボラティリティ分析モジュールを追加し、パラメータを動的に調整します。

- サポート・レジスタンスラインの算出方法を最適化し、精度を向上させます。

- トレンドの強さを判断する要素を追加し、エントリー条件を細分化します。

- ポジション管理システムを強化し、より緻密なリスクコントロールを実現します。

まとめ

本戦略は、構造が完備され、論理が厳密な定量取引戦略です。多層のテクニカル指標を組み合わせることで、取引シグナルの信頼性を確保しつつ、リスクの効果的なコントロールを実現しています。戦略の拡張性は高く、継続的な最適化と改善により、さまざまな市場環境で安定したパフォーマンスを発揮することが期待できます。

Source

Pine

/*backtest

start: 2024-12-17 00:00:00

end: 2024-12-21 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © sathcm

//@version=5

strategy("KMS", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.05, slippage=3)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1