モメンタム適応型ガウスチャネルマルチ周期戦略

1

Follow

1802

Followers

概要

本戦略は、ガウシアンチャネルとストキャスティックRSIを基盤としたモメンタム取引システムであり、季節性フィルターとボラティリティ管理を組み合わせたものです。適応型ガウシアンチャネルを用いて市場トレンドを識別し、ストキャスティックRSIで勢いを確認し、特定の季節的ウィンドウ内で取引を実行します。また、ATR(平均真のレンジ)に基づくポジション管理を統合し、各取引のリスクエクスポージャーを制御します。

戦略の原理

本戦略の核心は、多極点ガウシアンフィルターに基づく価格チャネルです。このチャネルは、HLC3価格のガウシアンフィルター値と真の変動幅(TR)のフィルター結果を組み合わせることで、動的な上下の軌道を形成します。取引シグナルは以下の条件を全て満たすことで生成されます:

- 価格が上軌道を突破し、主要フィルタートレンドが上昇

- ストキャスティックRSI指標が買われ過ぎ状態を示す

- 現在時刻が事前設定された季節的ウィンドウ内にある

- ポジションサイズはATRに基づいて動的に計算

決済シグナルは、価格が下軌道を下回ったことでトリガーされます。システム全体は多重フィルター機構により、取引の安定性を高めています。

戦略の利点

- ガウシアンフィルターは優れたノイズ除去能力を持ち、実際の市場トレンドを効果的に捕捉

- 多極点設計により、より精度の高い価格チャネル境界を提供

- モメンタムとトレンド指標を統合し、シグナル信頼性を向上

- 季節的フィルターにより、好ましくない市場環境を回避

- 動的なポジション管理によりリスクの一貫性を確保

- システムパラメータは様々な市場条件に応じて最適化可能

戦略のリスク

- ガウシアンフィルターの計算が複雑で、実行遅延が発生する可能性

- 多重フィルター条件により、重要な取引機会を逃す可能性

- システムはパラメータ設定に敏感で、慎重な最適化が必要

- 季節的ウィンドウの固定設定は市場環境変化に適応できない可能性

- 高ボラティリティ期間中は、ATRベースのポジション管理が保守的すぎる可能性

戦略の最適化方向性

- 適応型の季節的ウィンドウを導入し、市場条件に応じて取引時間を動的に調整

- ガウシアンフィルターの計算効率を最適化し、実行遅延を低減

- 市場ボラティリティ調整機構を追加し、異なる市場環境でフィルター条件を調整

- より柔軟なポジション管理システムを開発し、リスクとリターンのバランスを図る

- 複数時間枠の分析を追加し、シグナル信頼性を向上

まとめ

本戦略は、複数層のフィルターとリスク管理機構により取引の安定性を高めた、堅牢なトレンドフォローシステムです。改善の余地はあるものの、全体の設計思想は現代のクオンツ取引の要件に合致しています。戦略の成功の鍵は、パラメータの精度の高い調整と市場環境への適応力にあります。

Source

Pine

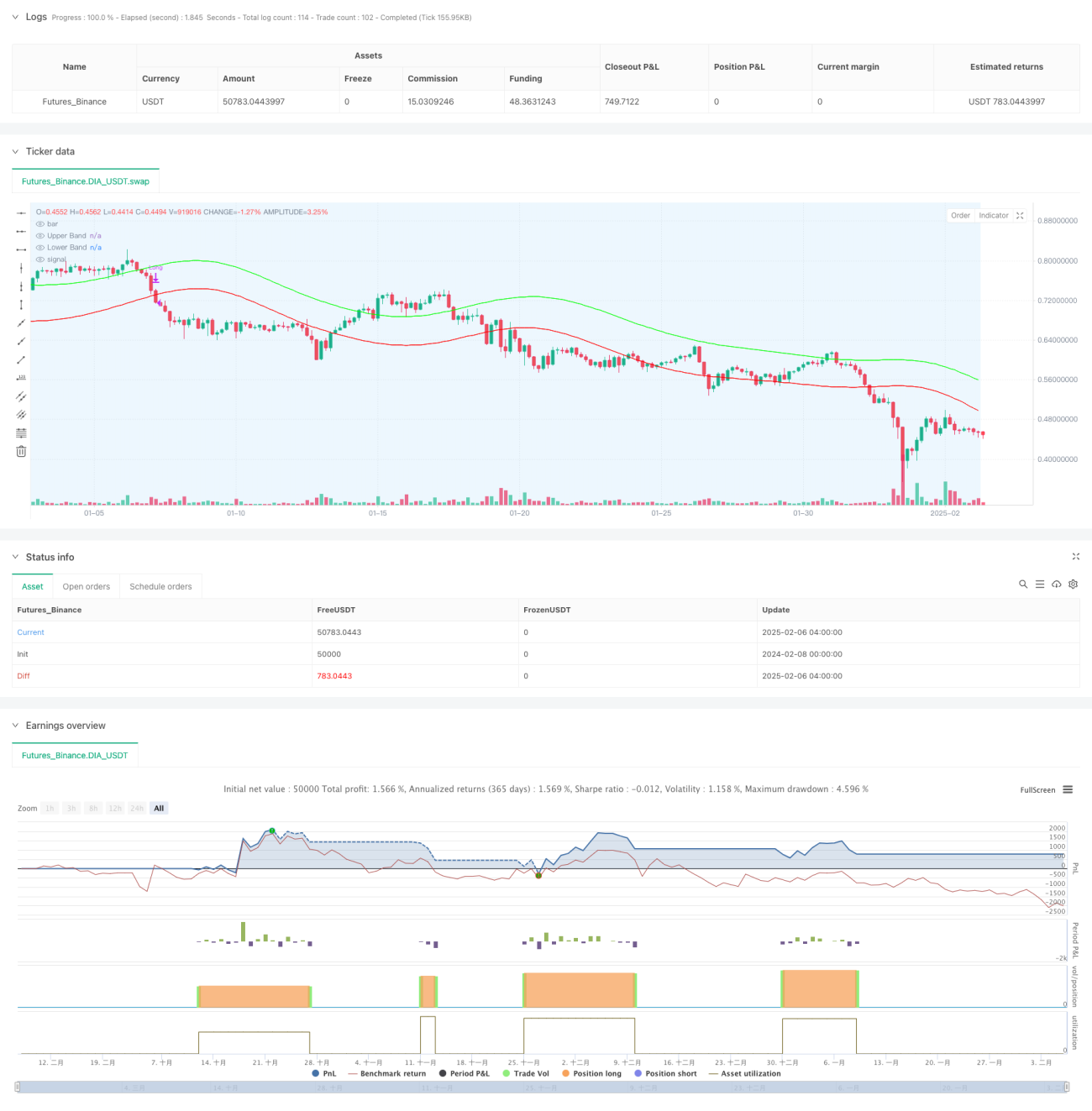

/*backtest

start: 2024-02-08 00:00:00

end: 2025-02-06 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"DIA_USDT"}]

*/

//@version=6

strategy("Demo GPT - Gold Gaussian Strategy", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1)

// ====== INPUTS ======Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1