高级な多重トレンド確認のEMA需給ゾーン動的アービトラージ戦略

1

Follow

1802

Followers

概要

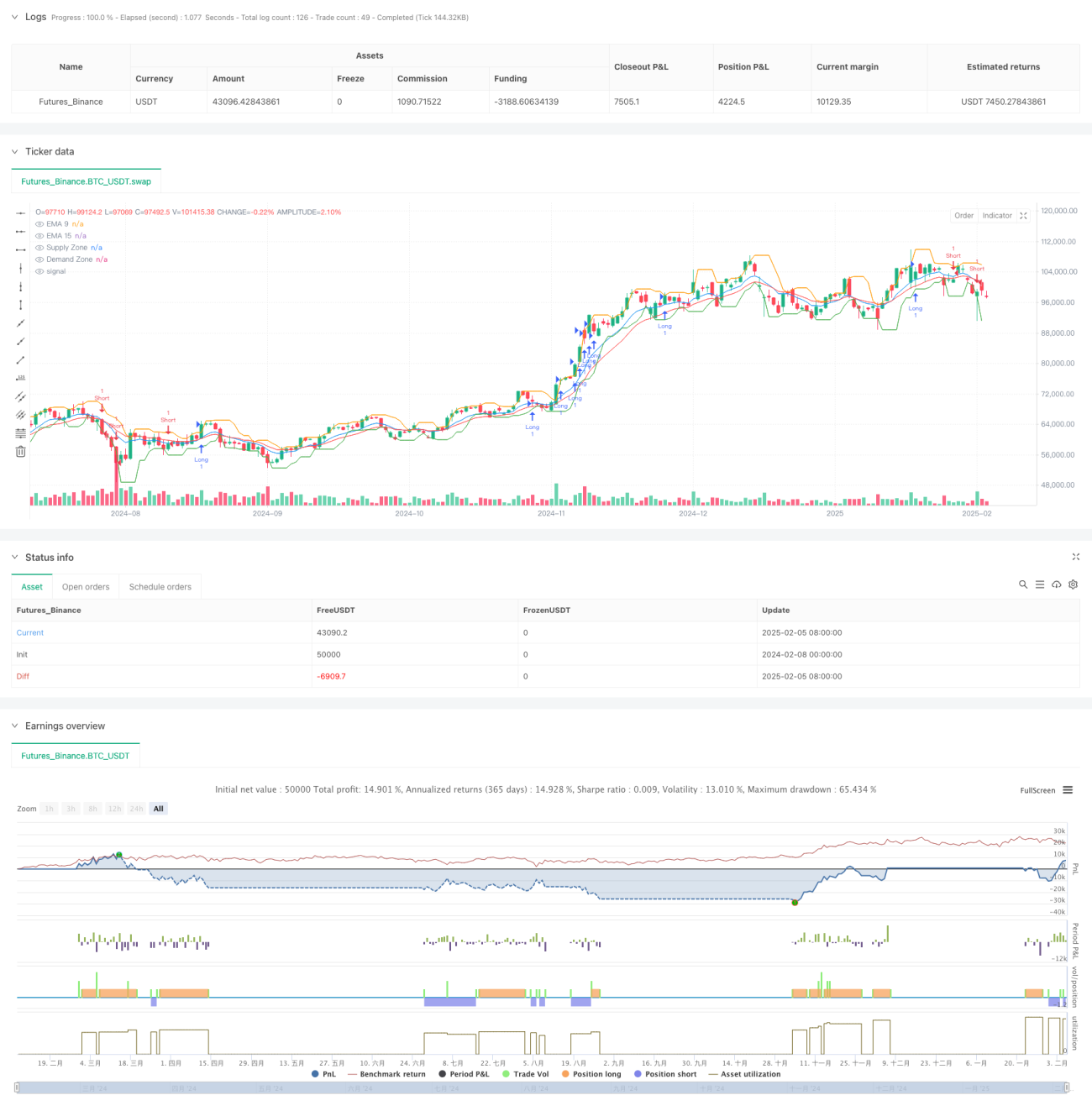

この戦略は、移動平均線(EMA)、需給ゾーン、取引量を組み合わせた高度な適応的アービトラージ戦略です。複数のテクニカル指標のクロス確認により市場トレンドを識別し、重要な需給ゾーン付近で取引を行います。戦略は動的なストップロスと利確目標を採用し、ATR指標によって市場のボラティリティに適応します。

戦略原理

戦略の中核ロジックは以下の主要要素に基づいています。

- 9期間および15期間のEMAのトレンド方向を主要な取引シグナルとして使用

- より高い時間枠(15分足)の需給ゾーンを通じて重要な価格レベルを決定

- 取引量確認を利用してトレンドの有効性を検証

- ATRに基づく動的なストップロスと利確目標を使用してリスクを管理

- 複数の条件が同時に満たされた場合にのみ取引を行う

具体的には、9期間EMAが3期間連続で上昇し、15期間EMAも上昇トレンドにあり、価格が需要ゾーンより上に位置し、かつ20期間の取引量移動平均線が50期間の取引量移動平均線より大きい場合、システムはロングシグナルを発します。ショートシグナルのロジックはその逆です。

戦略の優位性

- 多重確認メカニズムにより取引の信頼性が大幅に向上

- 動的なストップロスと利確目標は異なる市場環境に適応可能

- 需給ゾーンのフィルタリングにより不利な価格帯での取引を回避

- 取引量確認により追加のトレンド検証を提供

- リスクリワード比は市場状況に応じて柔軟に調整可能

- 戦略は優れた適応性を持ち、様々な市場条件に適合

戦略リスク

- 高ボラティリティ市場では偽シグナルが発生する可能性がある

- 多重確認条件により一部の取引機会を逃す可能性がある

- 需給ゾーンの識別に遅延が生じる可能性がある

- レンジ相場では頻繁な取引シグナルが発生する可能性がある

リスク管理策:

- 動的ATRストップロスを使用して市場の変動に適応

- 取引量確認により偽シグナルをフィルタリング

- 厳格なリスクリワード比管理を実施

- 重要な価格ゾーン付近で取引を実行

戦略最適化の方向性

- 適応型EMA期間を導入し、市場のボラティリティに応じて自動調整可能にする

- 市場状態識別モジュールを追加し、異なる市場環境で異なるパラメータを使用する

- 需給ゾーンの計算方法を最適化し、識別精度を向上させる

- より多くの市場ミクロ構造分析を追加する

- 動的なリスクリワード比調整メカニズムを開発する

まとめ

これは複数のテクニカル分析ツールを融合した完全な取引システムであり、多重確認メカニズムにより取引の信頼性を高めています。戦略の強みはその適応性とリスク管理能力にありますが、同時に異なる市場環境でのパフォーマンスの差異に注意する必要があります。提案された最適化の方向性により、この戦略にはさらなる向上の余地があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1