1

Follow

1802

Followers

概要

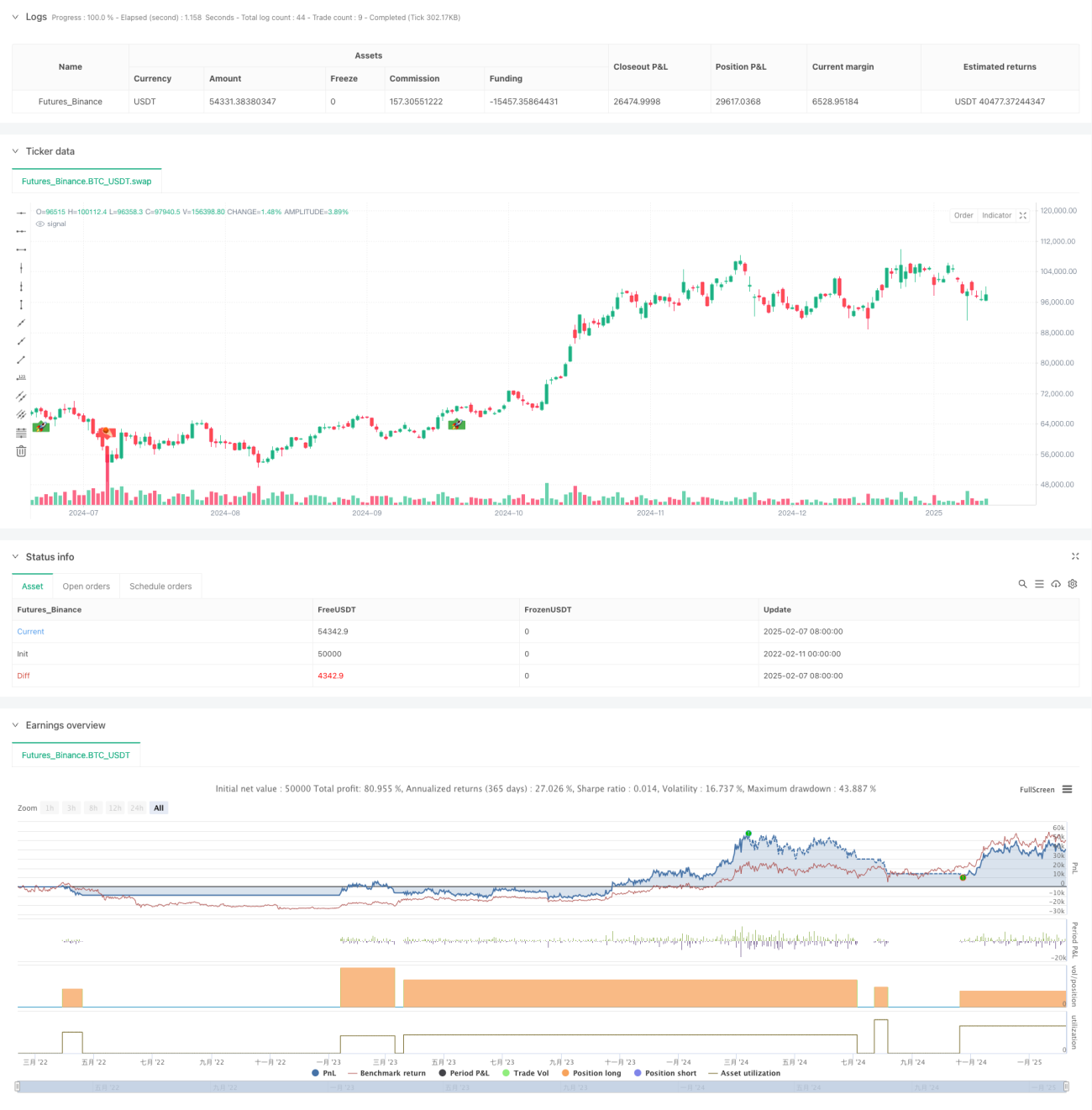

これはケルトナーチャネル(Keltner Channel)をベースにした柔軟な取引戦略です。この戦略はロング・ショート両方向の取引をサポートし、価格がチャネルの上限・下限をブレイクする動きを監視して取引を行います。戦略の中核は、移動平均線(MA)を使用して価格チャネルを構築し、真実の変動幅(ATR)を組み合わせてチャネル幅を動的に調整することで、様々な市場環境下でも適応性を維持することにあります。

戦略の原理

戦略は主に以下の基本原理に基づいています。

- EMAまたはSMAを用いて価格の中心的なトレンドを計算し、チャネルのミドルバンドを形成する

- ATR、TR、またはレンジを使用してボラティリティを計算し、チャネルの上限・下限を構築する

- 価格が上限をブレイクした際にロングシグナル、下限をブレイクした際にショートシグナルを発生させる

- ストップ注文の仕組みを利用してエントリーとエグジットを行い、取引執行の信頼性を高める

- 柔軟な取引モードの選択をサポート:ロングのみ、ショートのみ、または両方向の取引

戦略の優位性

- 適応性が高い - ATRによりチャネル幅を動的に調整するため、様々な市場のボラティリティ環境に適応可能

- リスク管理が充実 - ストップ注文の仕組みで取引を行い、リスクを効果的に管理

- 操作の柔軟性 - 複数の取引モードをサポートし、市場特性や取引スタンスに応じて調整可能

- 有効性が確認済み - 暗号資産や株式市場で良好なパフォーマンスを示し、特にボラティリティの高い市場で効果的

- 視認性が高い - 取引シグナルやポジション状況を直感的に表示

戦略のリスク

- レンジ相場リスク - 横ばいのレンジ相場では、頻繁に偽のブレイクアウトシグナルが発生する可能性がある

- スリッページリスク - 流動性が低い市場では、ストップ注文が大きなスリッページに直面する可能性がある

- トレンド反転リスク - トレンドが急反転した場合、大きな損失を被る可能性がある

- パラメータ感応性 - チャネルパラメータの選択が戦略のパフォーマンスに大きな影響を与える

戦略の最適化方向

- トレンドフィルターの導入 - トレンド判断指標を追加することで偽のブレイクアウトシグナルを低減

- 動的パラメータ最適化 - 市場のボラティリティ状況に応じてチャネルパラメータを動的に調整

- ストップ仕組みの改善 - トレーリングストップ機能を追加し、利益をより確実に保護

- 出来高確認の追加 - 出来高インジケーターと組み合わせることでシグナルの信頼性を向上

- ポジション管理の最適化 - 動的なポジション管理を導入し、リスクをより適切にコントロール

まとめ

本戦略は設計がしっかりとしており、ロジックが明確な取引システムです。ケルトナーチャネルと複数のテクニカル指標を柔軟に活用することで、市場機会を効果的に捉えます。カスタマイズ性が高く、異なるリスク選好を持つトレーダーに適しています。継続的な最適化と改良により、様々な市場環境下で安定したパフォーマンスを発揮することが期待されます。

Source

Pine

/*backtest

start: 2022-02-11 00:00:00

end: 2025-02-08 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy(title = "Jaakko's Keltner Strategy", overlay = true, initial_capital = 10000, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

// ──────────────────────────────────────────────────────────────────────────────Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1