1

Follow

1802

Followers

概要

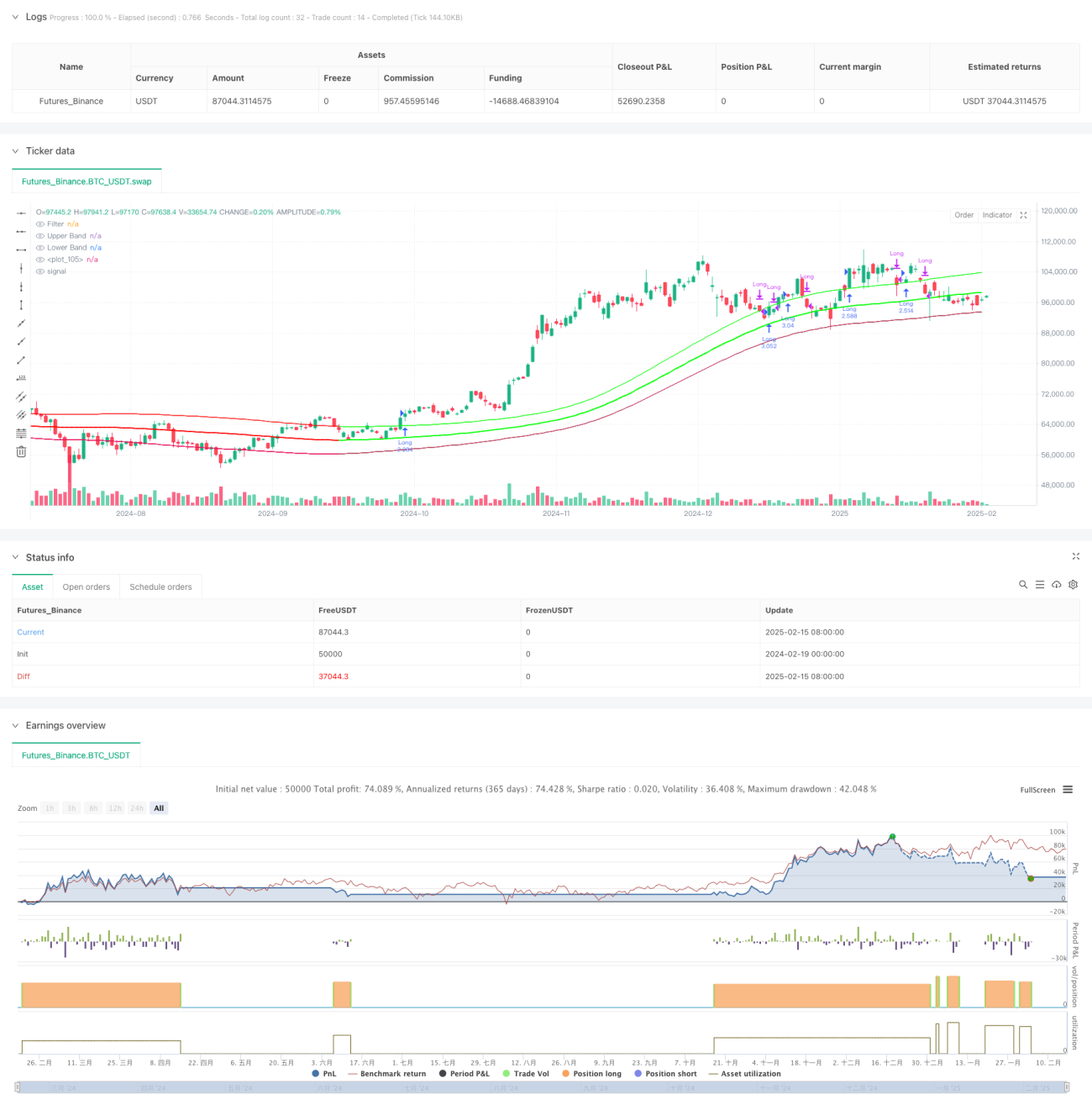

本戦略は、ガウスフィルタとStochRSI指標に基づいたトレンドフォロー型の取引システムです。この戦略では、ガウスチャネルを使用して市場のトレンドを識別し、StochRSI指標の買われ過ぎ/売られ過ぎの領域を組み合わせてエントリータイミングを最適化します。システムは多項式フィッティング手法を用いてガウスチャネルを構築し、上下のバンドの動的調整により価格トレンドを追跡し、市場の動きを正確に追跡します。

戦略原理

戦略の核心は、ガウスフィルタリングアルゴリズムに基づく価格チャネルです。具体的な実装は以下の重要なステップを含みます:

- 多項式関数f_filt9xを使用して9次ガウスフィルタを実装し、極点最適化によりフィルタ効果を向上

- HLC3価格に基づいてメインフィルタ線とボラティリティチャネルを計算

- reducedLagモードを導入してフィルタ遅延を低減、fastResponseモードで応答速度を向上

- StochRSI指標の買われ過ぎ/売られ過ぎ領域(80/20)を利用して取引シグナルを確定

- ガウスチャネルが上向きで価格が上バンドを突破した場合、StochRSI指標と組み合わせてロングシグナルを生成

- 価格が上バンドを下回った場合にポジションをクローズしてエグジット

戦略の利点

- ガウスフィルタは優れたノイズ除去能力を持ち、市場ノイズを効果的に除去可能

- 多項式フィッティングによりトレンドを滑らかに追跡し、偽シグナルを低減

- 遅延最適化と高速応答モードをサポートし、市場特性に応じて柔軟に調整可能

- StochRSI指標と組み合わせてエントリータイミングを最適化し、取引成功率を向上

- 動的なチャネル幅を採用し、市場のボラティリティ変化に適応

戦略リスク

- ガウスフィルタには一定の遅延があり、エントリーやエグジットがタイムリーでない可能性がある

- レンジ相場では頻繁な取引シグナルが発生し、取引コストが増加する可能性がある

- StochRSI指標は特定の市場条件下で遅延シグナルを発生させる可能性がある

- パラメータ最適化プロセスが複雑で、異なる市場環境に応じてパラメータを再調整する必要がある

- システムの計算リソース要求が高く、リアルタイム計算に遅延が生じる可能性がある

戦略最適化の方向性

- 適応型パラメータ最適化メカニズムを導入し、市場状態に応じて動的にパラメータを調整

- 市場環境認識モジュールを追加し、異なる市場条件下で異なるパラメータセットを使用

- ガウスフィルタリングアルゴリズムを最適化し、計算遅延をさらに低減

- より多くのテクニカル指標を導入してクロスバリデーションを行い、シグナルの信頼性を向上

- スマートストップロスメカニズムを開発し、リスク管理能力を向上

まとめ

本戦略は、ガウスフィルタとStochRSI指標の組み合わせにより、市場トレンドを効果的に追跡します。システムは優れたノイズ除去能力とトレンド識別能力を持ちますが、一定の遅延とパラメータ最適化の難しさも存在します。継続的な最適化と改善により、本戦略は実際の取引において安定した収益を上げることが期待されます。

Source

Pine

/*backtest

start: 2024-02-19 00:00:00

end: 2025-02-16 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Demo GPT - Gaussian Channel Strategy v3.0", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=0, default_qty_type=strategy.percent_of_equity, default_qty_value=250)

// ============================================Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1