ダイナミックトレーリングストップロスを用いた三分の一ローソク足の定量取引戦略

1

Follow

1802

Followers

概要

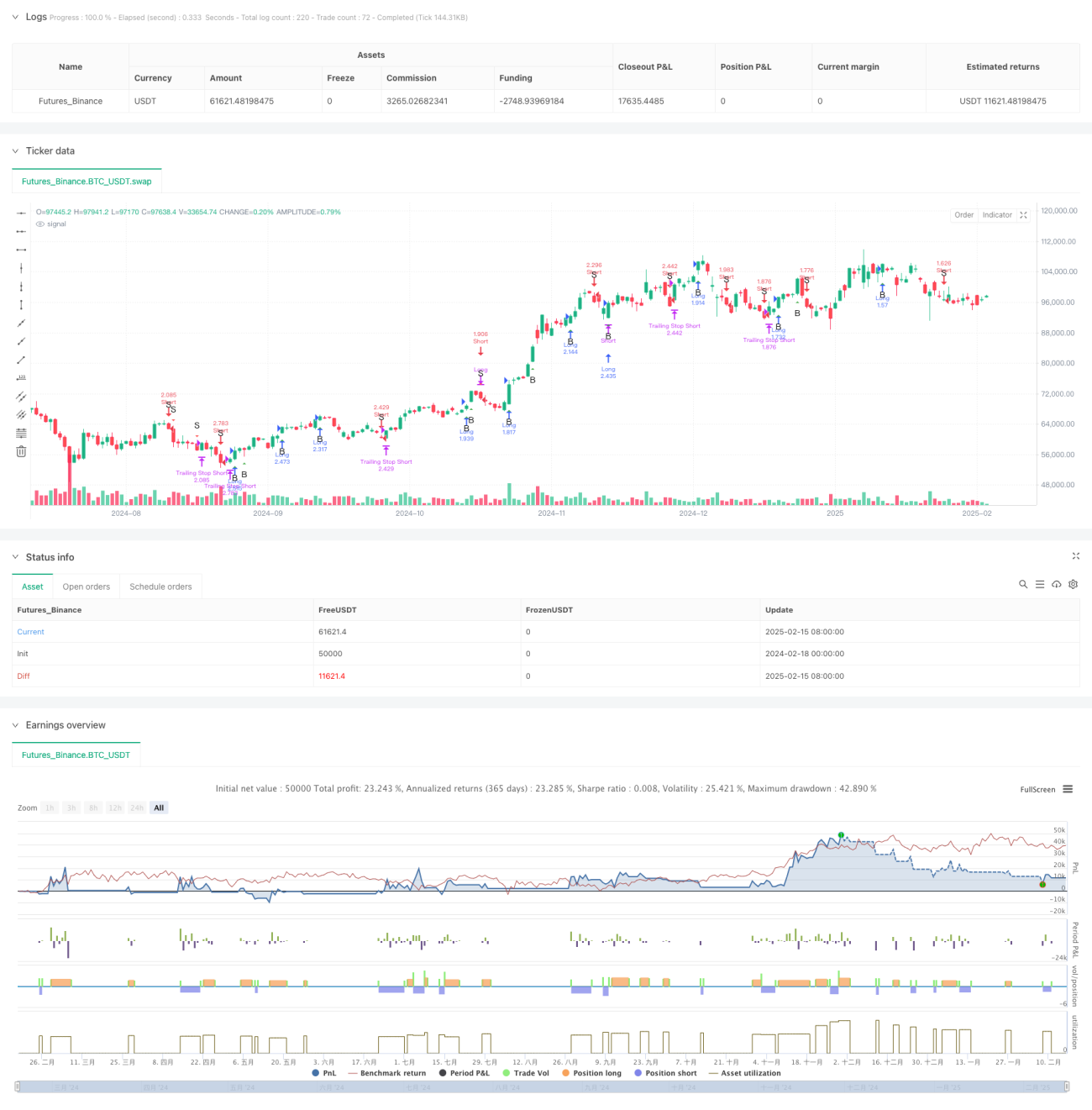

これは、ビル・ウィリアムズ(Bill Williams)の3分の1ローソク足分析手法と動的トレーリングストップ機能を組み合わせた定量取引戦略です。本戦略は、現在のローソク足と前のローソク足の構造的特徴を分析することで明確な買いシグナル・売りシグナルを生成し、設定可能なトレーリングストップ機構を利用してポジションを保護することで、正確なエントリー/エグジットとリスク管理を実現します。

戦略の原理

戦略のコアロジックは以下の主要部分に基づいています:

- ローソク足の三等分計算:各ローソク足のレンジ(高値-安値)を3等分し、上部ゾーンと下部ゾーンの境界値を取得します。

- ローソク足の形状分類:始値と終値が三等分ゾーンのどの位置にあるかに基づいて、ローソク足を複数のタイプに分類します。例えば、始値が下部ゾーンにあり終値が上部ゾーンにある場合、強い上昇形状と見なされます。

- シグナル生成ルール:現在のローソク足と前のローソク足の形状を組み合わせて分析し、有効な取引シグナルを判定します。例えば、連続する2本のローソク足がともに強い特徴を示す場合、買いシグナルがトリガーされます。

- 動的トレーリングストップ:指定された期間内で、前N本のローソク足の最安値(買いポジションの場合)または最高値(売りポジションの場合)を移動ストップポイントとして使用します。

戦略の利点

- ロジックの明確性:直感的なローソク足構造分析手法を用いており、取引ルールが明確で理解しやすい。

- リスク管理の充実:動的トレーリングストップ機構により、十分な利益空間を確保しつつ、ドローダウンリスクを効果的に抑制できる。

- 適応性の高さ:市場環境に応じてトレーリングストップパラメータを調整でき、優れた適応性を持つ。

- 自動化の高さ:シグナル生成からポジション管理まで完全に自動化されており、人為的介入を低減する。

戦略のリスク

- レンジ相場リスク:横ばいのレンジ相場では、頻繁な偽のブレイクアウトシグナルが発生し、過剰取引につながる可能性がある。

- ギャップリスク:大幅なギャップが発生した場合、トレーリングストップが適時にトリガーされず、想定以上の損失が生じる可能性がある。

- パラメータ敏感性:トレーリングストップのパラメータ選択が戦略のパフォーマンスに大きな影響を与え、不適切な設定は早期エグジットや保護不足を引き起こす可能性がある。

戦略の最適化方向性

- 市場環境フィルターの追加:トレンド指標やボラティリティ指標を導入し、異なる市場環境で戦略パラメータを動的に調整する。

- ストップ機構の最適化:ATR指標を組み合わせてより柔軟なストップ距離を設定し、ストップの適応性を高めることを検討する。

- ポジション管理の導入:シグナルの強さや市場のボラティリティに応じてポジションサイズを動的に調整し、より精密なリスクコントロールを実現する。

- エグジットの最適化:利益目標やテクニカル指標を追加してエグジットタイミングを補助判断し、エグジットの最適化を図る。

まとめ

これは構造が完備され、ロジックが明確な定量取引戦略であり、古典的なテクニカル分析手法と現代的なリスク管理技術を組み合わせることで、高い実用性を備えています。戦略の設計は実取引のニーズ(シグナル生成、ポジション管理、リスク管理等の重要な要素)を十分に考慮しています。さらなる最適化と改善により、本戦略は実際の取引においてより良いパフォーマンスを発揮することが期待されます。

Source

Pine

/*backtest

start: 2024-02-18 00:00:00

end: 2025-02-16 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("TrinityBar with Trailing Stop", overlay=true, initial_capital=100000,

default_qty_type=strategy.percent_of_equity, default_qty_value=250)

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1