1

Follow

1802

Followers

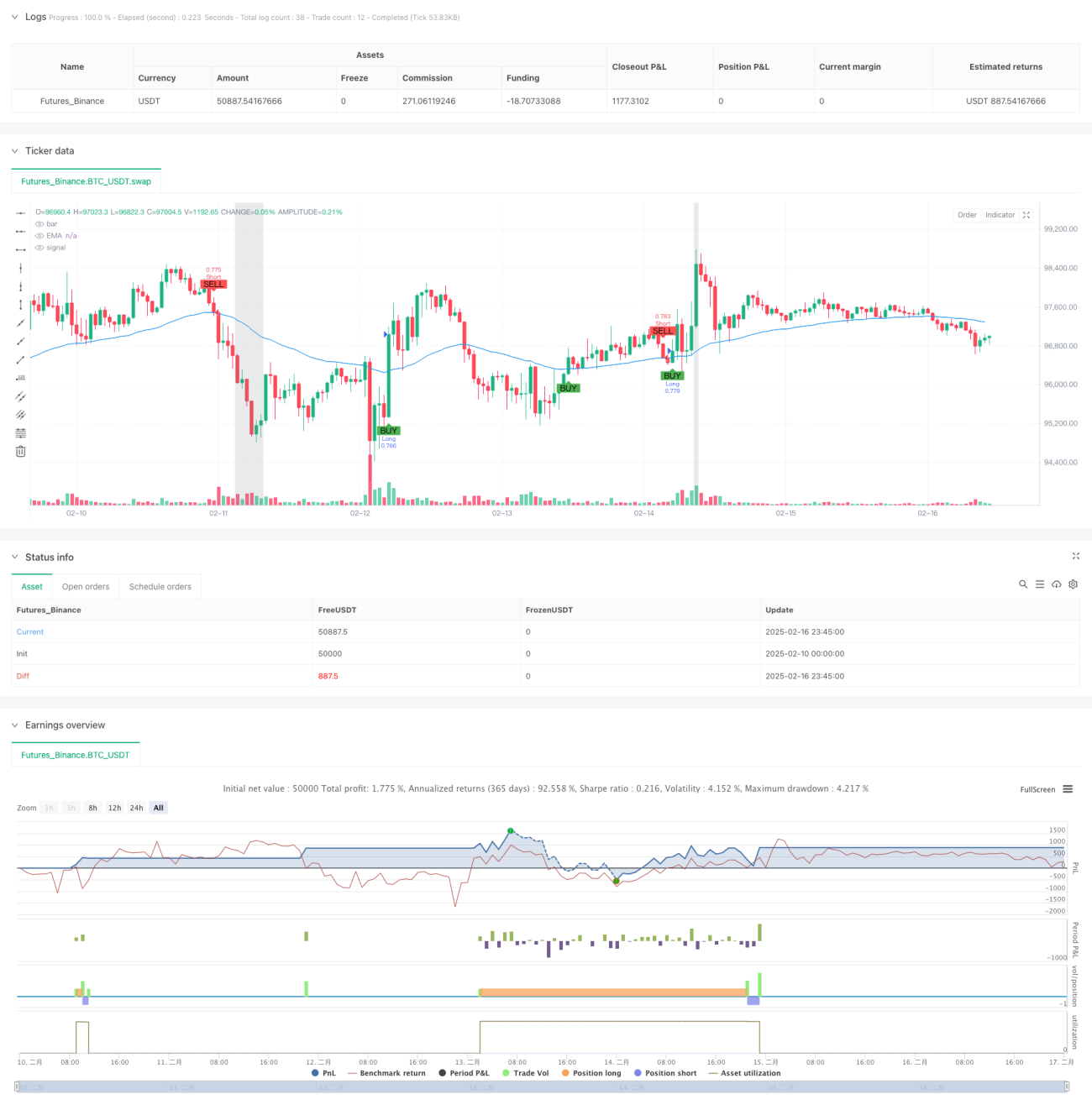

これは複数のテクニカル指標に基づいたトレンドフォロー戦略であり、ポジションを動的に調整することでスイングトレードを実現します。本戦略は主に指数平滑移動平均線(EMA)、相対力指数(RSI)、およびトレンド方向指数(ADX)を用いて市場トレンド分析と売買シグナル生成を行い、同時に平均真のレンジ(ATR)を使用して動的なストップロスと利益目標を設定します。

戦略概要

本戦略は、複数のテクニカル指標を組み合わせたトレンドフォロー型取引システムです。主にEMAで価格トレンドの方向性を判断し、RSIで市場の買われすぎ・売られすぎ状態を評価し、ADXでトレンドの強さを検証し、最後にATRを使用してポジションサイズとリスク管理パラメータを動的に調整します。戦略は、口座残高のパーセンテージベース、固定資金量、固定契約数など、複数のポジション計算方法をサポートします。

戦略原理

- エントリーシグナル:価格がEMAを上抜け、かつRSIが50を超え、さらにADXが設定した閾値を上回る場合、買いシグナルが発生します。価格がEMAを下抜け、かつRSIが50未満、さらにADXが設定した閾値を上回る場合、売りシグナルが発生します。

- ポジション管理:選択した方法に基づいて建て玉数量を計算します。リスク比率ベース、資金比率ベース、固定資金量、固定契約数の4つの方法をサポートします。

- リスク管理:ATRを使用してストップロスと利益目標を動的に計算し、同時にトレーリングストップで既得利益を保護します。

優位性分析

- 多次元でのトレンド確認:EMA、RSI、ADXの三重指標でトレンドを確認し、取引シグナルの信頼性を向上させます。

- 柔軟なポジション管理:複数のポジション計算方法をサポートし、さまざまなトレーダーのニーズに対応します。

- 動的なリスク管理:ATRに基づく動的なストップロスと利益目標設定により、市場のボラティリティの変化に適応します。

- トレーリングストップ機構:トレーリングストップにより既得利益を保護し、全体的な収益性を向上させます。

リスク分析

- ラグリスク:テクニカル指標にはすべて一定の遅延が生じ、エントリーのタイミングが遅れる可能性があります。

- レンジ相場リスク:横ばいのレンジ相場では、頻繁に誤ったシグナルが発生する可能性があります。

- パラメータ感応度:複数の指標パラメータの選択が戦略のパフォーマンスに大きく影響します。

- レバレッジリスク:高倍率レバレッジをサポートするため、大きな資金リスクを伴う可能性があります。

最適化の方向性

- 市場環境への適応:市場環境識別メカニズムを追加し、異なる市場条件に応じてパラメータを動的に調整します。

- シグナルフィルタリング:出来高などの補助指標を導入し、シグナルの質を向上させます。

- 利確の最適化:より柔軟な分割利確メカニズムを設計し、収益性を高めます。

- リスク管理の強化:最大ドローダウン制御などのリスク管理メカニズムを追加します。

まとめ

これは複数のテクニカル指標を総合的に活用したトレンドフォロー戦略であり、多次元でのトレンド確認と堅牢なリスク管理メカニズムにより、比較的安定した取引を実現します。戦略の強みは体系的トレンド確認メカニズムと柔軟なポジション管理にありますが、指標のラグや市場環境への適応性などの問題にも注意が必要です。継続的な最適化とリスク管理の改善により、本戦略はさまざまな市場環境で安定したパフォーマンスを発揮することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1