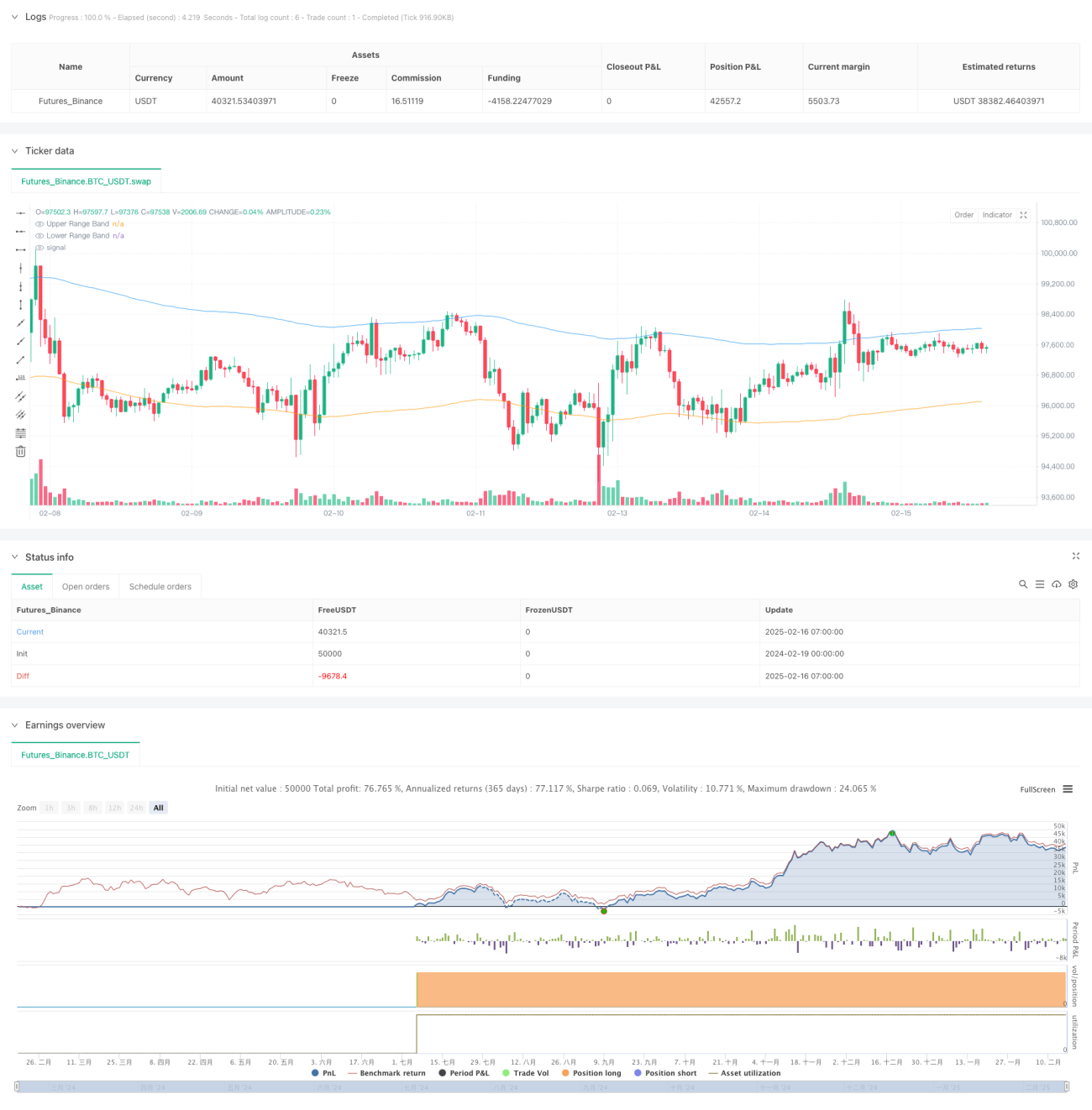

モメンタムと出来高に基づく複数指標のトレンド反転戦略

1

Follow

1802

Followers

概要

本戦略は、モメンタム指標(MACD、RSI)と出来高フィルターを組み合わせたトレンド反転取引システムです。レンジフィルター(Range Filter)による価格変動の監視を導入し、市場の天底を正確に捉えることを目的としています。従来のテクニカル指標に出来高確認メカニズムを加えることで、取引シグナルの信頼性を効果的に高めています。

戦略の原理

本戦略では、以下の複数の指標による検証を取引判断に用います:

- MACD指標:価格モメンタムの変化を捉え、短期線と長期線のクロスでトレンド転換点を確認

- RSI指標:市場の買われ過ぎ・売られ過ぎを監視し、RSIが極値に達した時点で反転の可能性を探る

- レンジフィルター:価格の平滑化レンジ帯を計算し、トレンドから大きく乖離した位置で取引が発生するようにする

- 出来高フィルター:取引シグナルが出来高の増加によって確認されることを要求し、シグナルの信頼性を高める

複数条件の連動発動メカニズムは以下の通り:

- ロング条件:MACDゴールデンクロス + RSIが売られ過ぎエリア + 価格が下限バンドを下回る + 出来高が平均を上回る

- ショート条件:MACDデッドクロス + RSIが買われ過ぎエリア + 価格が上限バンドを上回る + 出来高が平均を上回る

戦略の優位性

- 複数指標の相互検証によりシグナルの精度が向上し、偽シグナルの影響を効果的に低減

- レンジフィルターの導入により、価格が大きく乖離した位置での取引が保証され、潜在的なリターン空間が拡大

- 出来高確認メカニズムにより、低流動性環境での誤判断を回避し、取引の信頼性を向上

- 戦略パラメータは柔軟に調整可能で、異なる市場環境や取引銘柄の特性に対応

- 明確なシグナル生成ロジックにより、リアルタイム監視やバックテスト分析が容易

戦略のリスク

- 複数条件の厳格な要求により、一部の潜在的な取引機会を逃す可能性

- レンジ相場では頻繁な取引シグナルが発生し、取引コストが増加する可能性

- パラメータ選択には十分な市場経験と過去データの裏付けが必要

- 極端な市場環境では、テクニカル指標の有効性が影響を受ける可能性

リスク管理の提案:

- 十分なパラメータ最適化とバックテスト検証を推奨

- ストップロス・テイクプロフィットメカニズムの導入を検討

- 市場環境の変化に注目し、戦略パラメータを適宜調整

戦略の最適化方向性

- 適応型パラメータ機構の導入:市場のボラティリティに応じて指標パラメータを動的に調整

- 市場環境識別モジュールの追加:異なる市場状態で異なるシグナルフィルタリングルールを適用

- 出来高フィルターの最適化:出来高パターン分析の導入を検討

- 価格パターン認識機能の追加:より多くの反転確認シグナルを提供

- スマート資金管理モジュールの開発:ポジションサイズとリスク管理の最適化

まとめ

本戦略は、複数のテクニカル指標を連携させることで、比較的完成度の高いトレンド反転取引システムを構築しています。戦略の核となる優位性は、厳格なシグナルフィルタリング機構と柔軟なパラメータ調整の余地にあります。継続的な最適化と改善により、様々な市場環境で安定したパフォーマンスを発揮することが期待されます。実際の適用にあたっては、投資家が自身のリスク選好や市場経験に応じて、戦略パラメータを調整することを推奨します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1