ATR動的トレンドフォローと再エントリー取引戦略

1

Follow

1802

Followers

概要

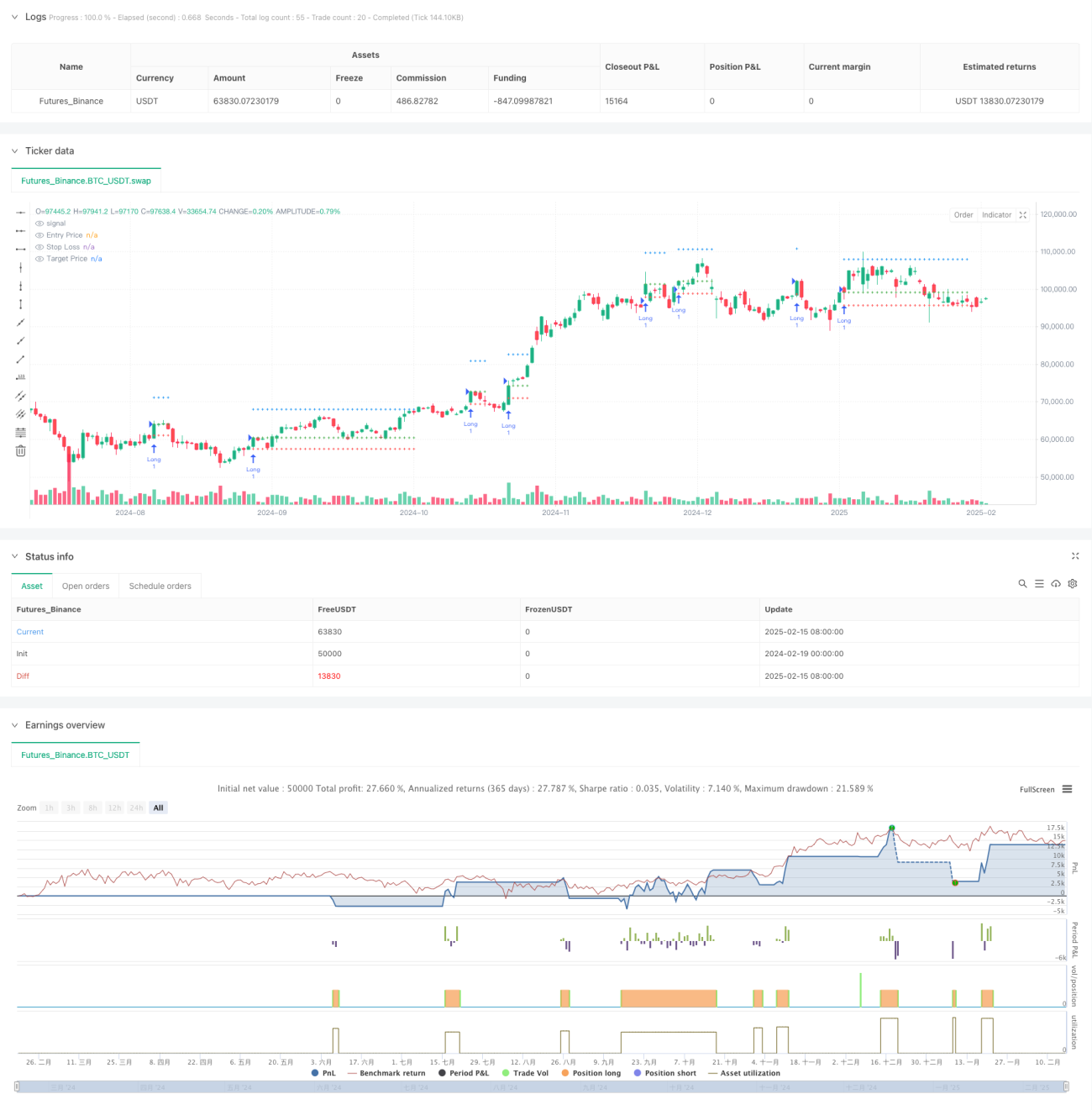

これはATRを動的に調整するトレンドフォロー戦略であり、移動平均線とATRを組み合わせてエントリーとエグジットのポイントを決定します。この戦略の核となる特徴は、ATRを用いて移動平均線の上下バンドを動的に調整し、価格が上バンドを突破した際に買いエントリーを行い、ATRの倍数に基づいたストップロスと利確ポイントを設定することです。さらに、価格がエントリーポイントまで戻った場合に再エントリーを可能にする革新的なメカニズムも含まれています。

戦略の原理

戦略は以下の重要な要素に基づいて動作します:

- ATRで調整された移動平均線をトレンド判断の基準として使用し、動的な上下バンドを形成します。

- 価格が上バンドを突破した際に買いシグナルが発生し、エントリー価格は現在の終値とします。

- ストップロスはエントリー価格の下方2倍のATR距離に設定されます。

- 利確ポイントはエントリー価格の上方(5 + カスタム倍数)× ATR距離に設定されます。

- ストップロスまたは利確がトリガーされた後、価格が元のエントリー価格まで戻った場合、戦略は自動的に再エントリーします。

- 最大30本のローソク足の表示制限を使用してチャート表示を最適化します。

戦略の利点

- 動的な適応性:ATRで調整された移動平均線は、市場のボラティリティの変化に自己適応できます。

- 科学的なリスク管理:ストップロスと利確ポイントはATRに基づいて動的に設定され、市場のボラティリティ特性に適合します。

- 革新的な再エントリーメカニズム:価格が有利な位置に戻った際に再エントリーを可能にし、利益獲得の機会を高めます。

- 優れた可視化効果:戦略は明確なエントリー、ストップロス、利確ラインを表示し、取引の監視を容易にします。

- 柔軟なパラメータ調整:入力パラメータにより、トレンド判断の周期や利確倍率を調整できます。

戦略のリスク

- トレンド反転リスク:レンジ相場ではストップロスが頻繁にトリガーされる可能性があります。

- 再エントリーリスク:価格がエントリーポイントまで戻って再建倉する場合、連続したストップロスに直面する可能性があります。

- スリッページリスク:ボラティリティの高い期間では、実際の約定価格がシグナル価格と乖離する可能性があります。

- パラメータ感応性:異なる市場条件下では最適なパラメータが大きく変化する可能性があります。

- 計算負荷:複数のテクニカル指標をリアルタイムで計算する必要があり、システム負荷が増加する可能性があります。

戦略の最適化方向

- 市場環境フィルターの導入:ボラティリティフィルターを追加し、高ボラティリティ期間中は戦略パラメータを調整するか取引を停止します。

- 再エントリーロジックの最適化:再エントリー時にトレンド確認指標など、より厳しい条件を考慮することができます。

- 利確メカニズムの改善:トレーリングストップロス機能を実装し、トレンド継続時に利益をより多く保護します。

- 時間フィルターの追加:取引時間帯の制限を追加し、低流動性期間を回避します。

- 計算効率の最適化:不要な計算や描画を削減することで、戦略の実行効率を向上させます。

まとめ

これは設計が合理的でロジックが明確なトレンドフォロー戦略であり、ATRによる動的調整により良好な市場適応性を提供します。戦略の再エントリーメカニズムは革新的なポイントであり、良好な市場条件下で追加の利益獲得機会を提供します。注意すべきリスクポイントはいくつかありますが、提案された最適化方向により戦略の安定性と収益性をさらに向上させることができます。体系的な取引方法を求める投資家にとって、検討に値する基本的な戦略フレームワークです。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1