1

Follow

1802

Followers

概要

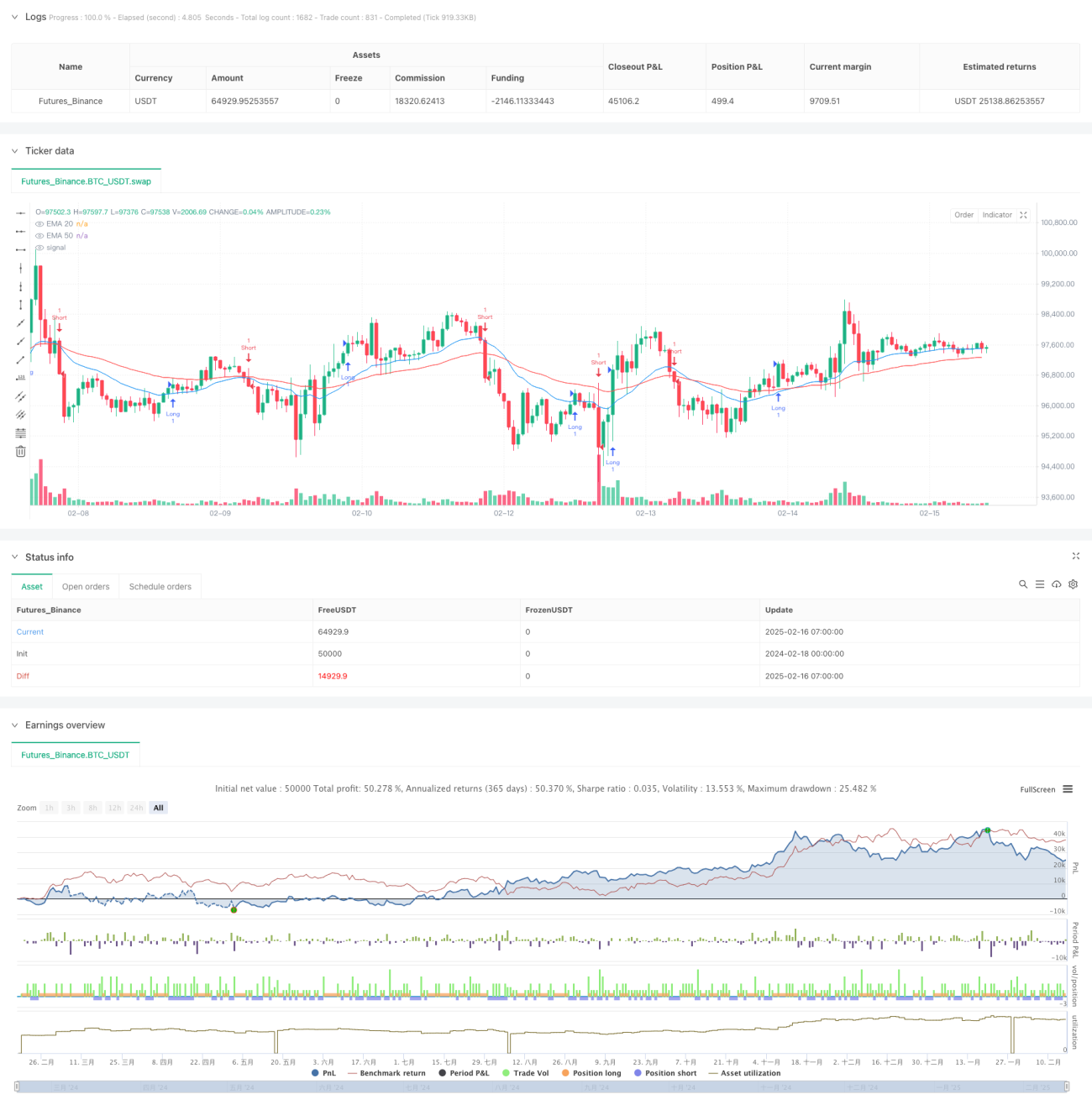

本戦略は、複数のテクニカル分析指標を組み合わせたハイブリッド取引システムです。主に移動平均線システム(EMA)で市場トレンドを判断し、サポート・レジスタンス(SR)レベルをエントリーシグナルとして活用し、ATR(平均真實レンジ)でリスク管理を行います。動的なストップロス設定を採用しており、市場のボラティリティに応じてストップロスの位置を適応的に調整できます。

戦略の原理

戦略は以下の主要コンポーネントに基づいて動作します。

- トレンド判定システム - 20期間と50期間の指数平滑移動平均線(EMA)の位置関係と差を用いてトレンドの強さを判断

- ブレイクアウトシグナルシステム - 9期間の最高値と最安値でサポート・レジスタンスレベルを構築

- リスク管理システム - 14期間のATRを採用し、ストップロスの距離を動的に調整

- エントリー条件は2つ:

- 価格がサポート・レジスタンスレベルを突破

- トレンド内にあり、価格が正しい移動平均線の方向にある

- エグジットはATRベースの動的ストップロスに基づき、ストップロス距離はATRの10倍

戦略の利点

- 多次元での確認 - トレンドフォローとブレイクアウト取引を組み合わせ、シグナル信頼性を向上

- 適応性の高さ - ATRでストップロスを動的に調整し、異なる市場環境に対応

- リスク管理の充実 - 明確なストップロスメカニズムがあり、市場変動に応じて調整

- システム化の高さ - 取引ルールが明確で、主観的判断の影響を受けない

- 拡張性の良さ - コアフレームワークが安定しており、新しい取引ルールを追加しやすい

戦略のリスク

- レンジ相場リスク - 横ばい市場では頻繁に偽シグナルが発生する可能性

- スリッページリスク - ブレイクアウト取引は高ボラティリティ時に大きなスリッページが発生する可能性

- ストップロス幅リスク - ATR倍率が大きすぎると大きなドローダウンにつながる可能性

- シグナル遅延リスク - 移動平均線システムには一定のラグが存在

- パラメータ感度 - 複数のパラメータ設定には十分なテストと最適化が必要

戦略の最適化方向

-

シグナルフィルター最適化

- 出来高確認メカニズムの追加

- ボラティリティフィルターの導入

- 他のテクニカル指標との検証強化

-

ポジション管理最適化

- 動的ポジション管理の実現

- ボラティリティに基づくポジションサイズ調整

- 分割建てメカニズムの追加

-

ストップロス最適化

- トレーリングストップの導入

- ATR倍率設定の最適化

- 利益保護メカニズムの追加

まとめ

本戦略は、複数の成熟したテクニカル分析方法を組み合わせることで、完全な取引システムを構築しています。中核となる強みは、システムの適応性とリスク管理能力にあります。継続的な改善と最適化により、本戦略は様々な市場環境で安定したパフォーマンスを発揮することが期待されます。実際の取引に使用する前に、十分な過去データテストとパラメータ最適化を実施することを推奨します。

Source

Pine

Strategy parameters

Comment

All comments (0)

No data

- 1