1

Follow

1802

Followers

概要

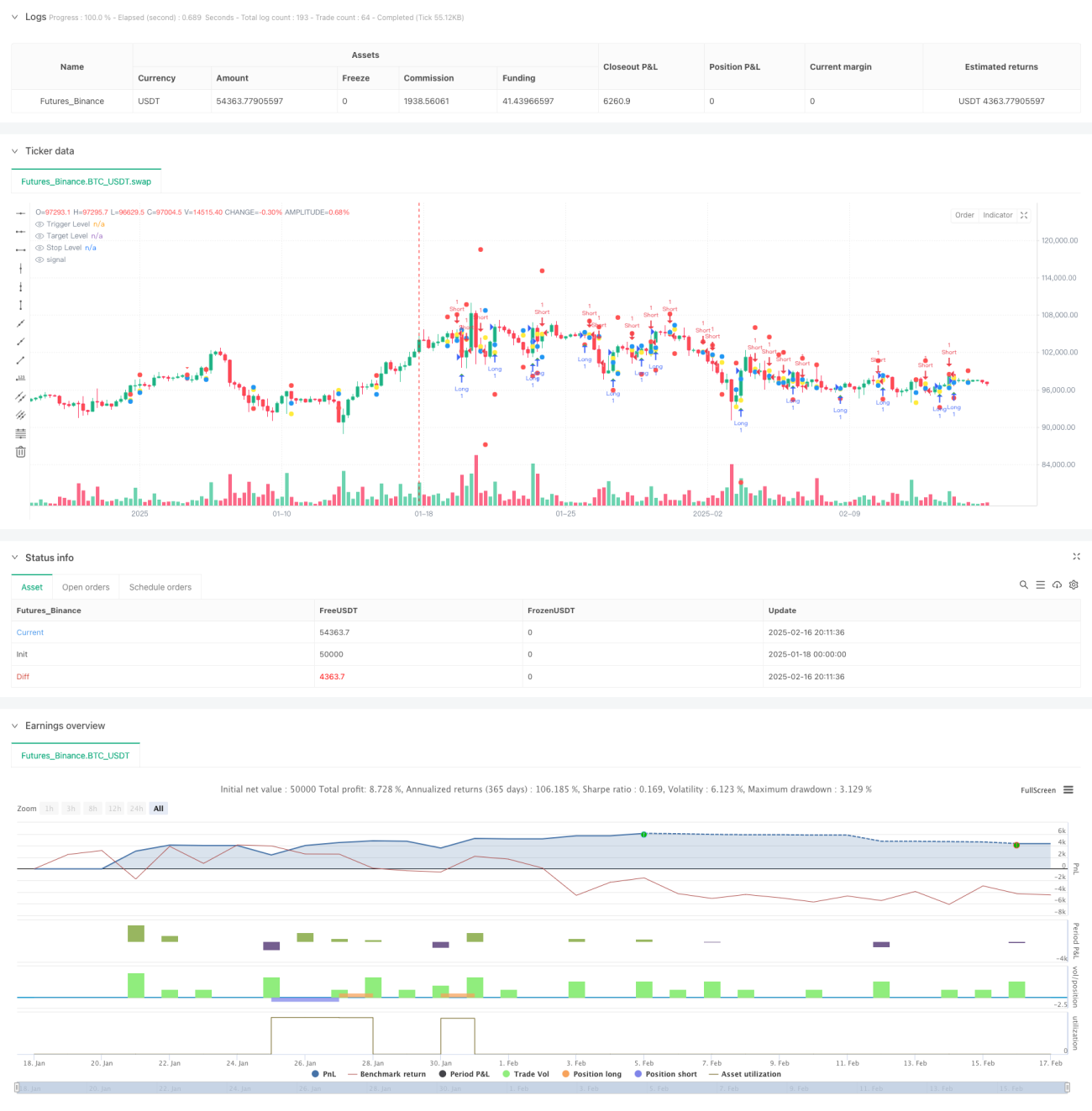

これはローソク足レンジ理論に基づくマルチタイムフレーム取引戦略です。主に、より高い時間足のローソク足の形状と価格レンジを分析することで、潜在的な取引機会を特定します。戦略は出来高フィルターと動的ストップロスメカニズムを統合しており、過去の高値安値のブレイクアウトを通じてトレンドの機会を捉えます。

戦略の原理

戦略の核心は、より高い時間足(デフォルト4時間)で価格が過去のレンジをブレイクする状況を監視することです。具体的には:

- 戦略は過去2本の高時間足ローソク足の高値安値データを継続的に追跡・保存します。

- 前のローソク足の終値が前高値より低く、現在のローソク足が新高値を付けた場合、売りシグナルが発生します。

- 前のローソク足の終値が前安値より高く、現在のローソク足が新安値を付けた場合、買いシグナルが発生します。

- エントリー価格はトリガーとなるローソク足の高値または安値の位置に設定されます。

- 利益確定目標は過去の対応する高値または安値の位置に設定されます。

- ストップロスの距離はレンジのサイズに応じて動的に調整されます。

戦略の利点

- マルチタイムフレーム分析により、より信頼性の高いシグナルを提供します。

- 動的ストップロス設定により、市場のボラティリティに応じて自己調整します。

- オプションの出来高フィルターメカニズムにより、取引確認度が向上します。

- 明確な視覚化インターフェースにより、トリガー価格、目標価格、ストップロス価格のマークが含まれます。

- 戦略ロジックはシンプルで明確であり、理解と実行が容易です。

- 様々な取引銘柄や市場環境に適用可能です。

戦略のリスク

- レンジ相場では頻繁な偽のブレイクアウトシグナルが発生する可能性があります。

- 大きなストップロス倍数により、一度の損失が大きくなる可能性があります。

- 過去の価格データに依存するため、急速に変化する市場環境では反応が遅れる可能性があります。

- ファンダメンタルズ要因を考慮していません。

- 流動性の低い市場では効果的に執行することが難しい場合があります。

戦略の最適化の方向性

- 移動平均線やADXインジケーターなどのトレンドフィルターを導入する。

- より多くの市場環境判断条件を追加する。

- ストップロス戦略を最適化し、トレーリングストップを導入することを検討する。

- ポジションサイズ管理モジュールを追加する。

- より多くの時間足の協調分析を追加することを検討する。

- ボラティリティ指標を導入してレンジ判断を最適化する。

まとめ

これは構造が完全で、ロジックが明確なマルチタイムフレーム取引戦略です。より高い時間足の価格行動を分析することで潜在的なトレンド機会を探し、同時にリスク管理とフィルターメカニズムを統合しています。戦略の核心的な利点はその適応性と拡張性にあり、簡単なパラメータ調整で様々な市場環境に適応できます。固有のリスクはいくつか存在しますが、提案された最適化の方向性を通じて戦略の安定性と信頼性をさらに向上させることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1