1

Follow

1802

Followers

概要

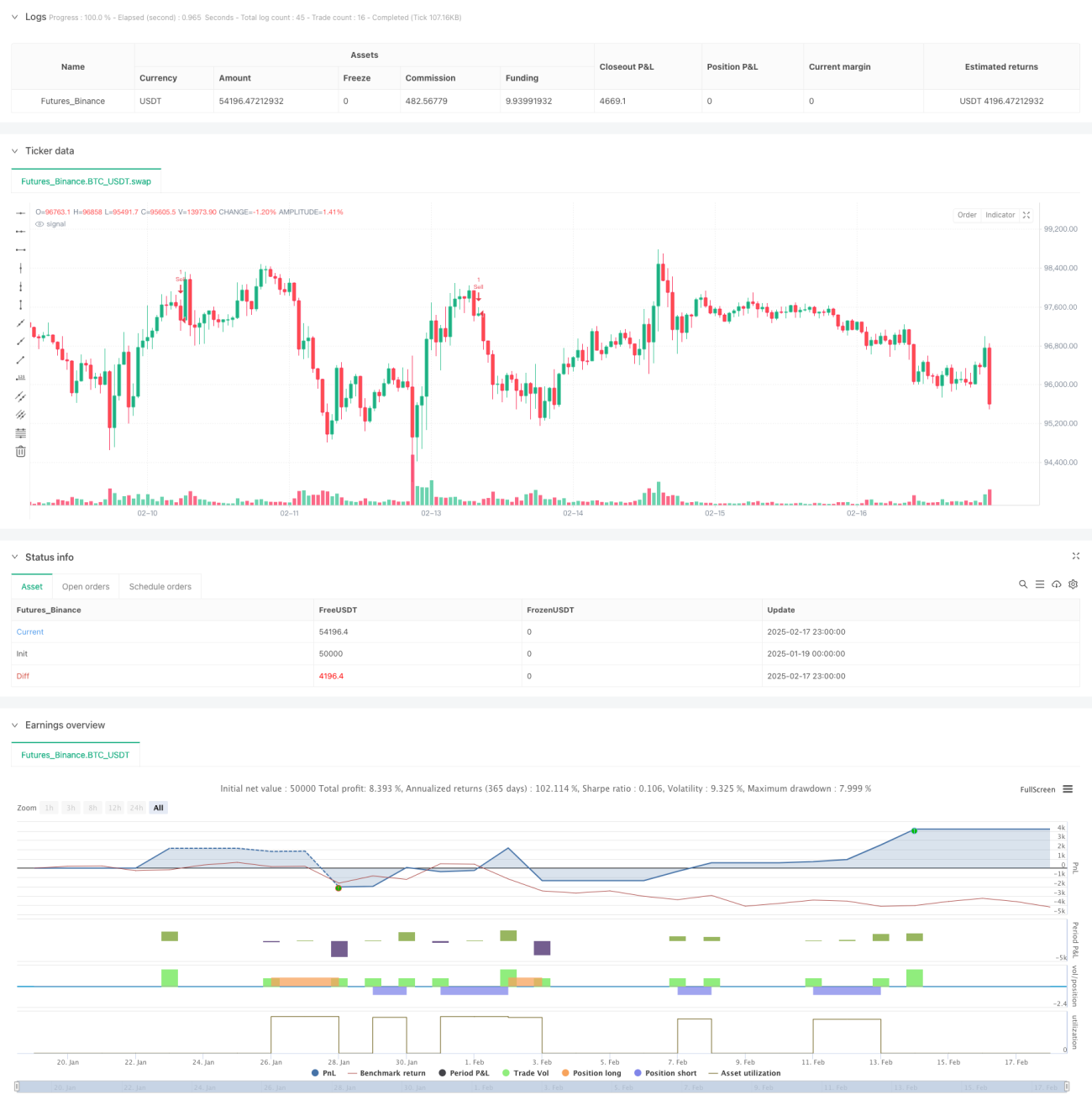

本戦略は、マルチタイムフレームのストキャスティクス指標に基づく取引システムであり、トレンド確認と価格パターン分析を組み合わせています。戦略は15分足、30分足、60分足の3つの時間足を使用し、ストキャスティクスのクロスシグナルと、高値圏での高値(Higher High)や安値圏での安値(Lower Low)のパターン確認を通じて取引機会を特定します。同時に、戦略は固定パーセンテージのストップロスと利益確定設定を採用し、リスクを管理し利益を確定します。

戦略の原理

戦略の中核ロジックは以下の重要な部分から構成されます:

- 3つの異なる時間足(15分足、30分足、60分足)のストキャスティクス指標を使用して市場の動向を分析します

- 主要時間足(15分足)において、K線がD線を上抜けし、かつ売られ過ぎ領域にある場合、より高い安値(Higher Low)パターンの確認で買いシグナルとします

- 同様に、K線がD線を下抜けし、かつ買われ過ぎ領域にある場合、より低い高値(Lower High)パターンの確認で売りシグナルとします

- ストップロス3.7%、利益確定目標1.8%を採用し、各取引のリスクとリターンを管理します

戦略の利点

- マルチタイムフレーム分析はより包括的な市場視点を提供し、偽のシグナルをより適切にフィルタリングできます

- 価格パターン分析の組み合わせにより、取引シグナルの信頼性が向上します

- 固定されたリスク管理パラメーターにより、取引結果がより安定し制御可能になります

- 戦略はボラティリティの高い市場環境に適しています

- 自動化されたエントリー・エグジットシグナルにより、主観的判断による感情的な影響が低減されます

戦略のリスク

- レンジ相場では頻繁な偽のシグナルが発生する可能性があります

- 固定されたストップロスと利益確定設定は、すべての市場環境に適しているとは限りません

- マルチタイムフレームのシグナルは遅延を生じる可能性があります

- 急激なトレンド相場では、利確設定が早期に利益を確定してしまう可能性があります

- 3.7%のストップロスに耐えるための十分な資金管理が必要です

戦略の最適化方向性

- 市場のボラティリティに応じてストップロスと利益確定目標を動的に調整することを検討できます

- 出来高指標を補助確認シグナルとして追加します

- トレンド強度指標を導入してレンジ相場でのパフォーマンスを改善します

- マルチタイムフレーム間のウェイト設定を最適化します

- 市場センチメント指標を追加してシグナルの精度を向上させることを検討します

まとめ

これは、マルチタイムフレーム分析とトレンド確認を組み合わせた完全な取引システムです。ストキャスティクス指標と価格パターンの組み合わせにより、市場の転換点をうまく捉えることができます。固定されたリスク管理パラメーターはシンプルですが、取引の一貫性を確保します。この戦略はボラティリティの高い市場に適していますが、トレーダーは具体的な市場環境に応じてパラメーターを最適化する必要があります。

Source

Pine

Strategy parameters

Comment

All comments (0)

No data

- 1