1

Follow

1802

Followers

概要

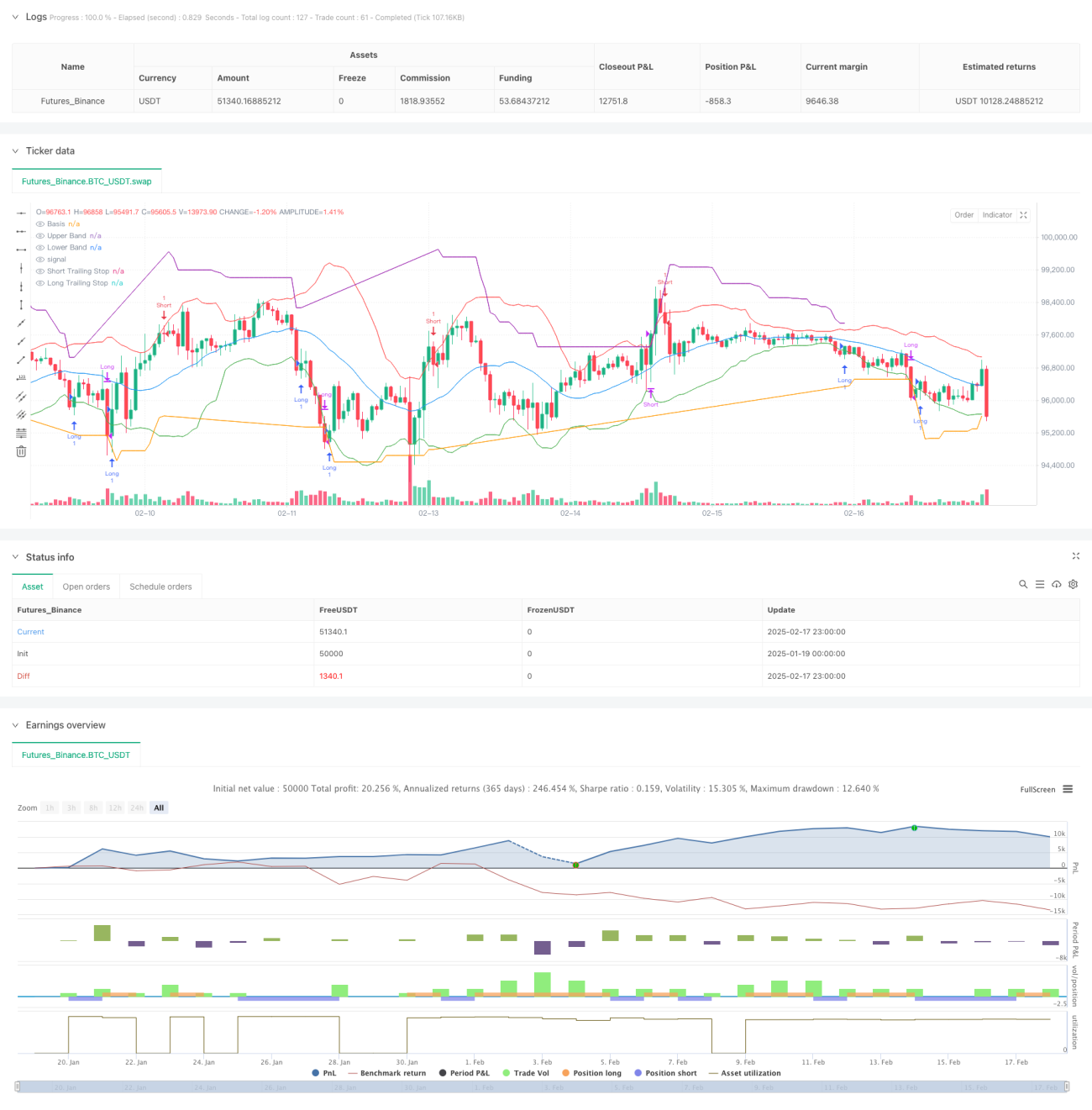

本戦略は、ボリンジャーバンド(Bollinger Bands)とATRトレーリングストップを組み合わせた適応型取引システムです。戦略は、ボリンジャーバンドの上限・下限のブレイクアウトをエントリーシグナルとし、ATRベースの動的トレーリングストップでリスク管理とエグジットタイミングを決定します。この戦略は、明確なトレンド相場でトレンド機会を捉えつつ、レンジ相場では防御機能を提供します。

戦略の原理

戦略の核となるロジックは、2つの主要部分から構成されます。

- エントリーシグナルシステム:ボリンジャーバンド(BB)を主指標とし、価格が下限をブレイクした場合はロングシグナル、上限をブレイクした場合はショートシグナルを発生させます。ボリンジャーバンドのパラメータは、中央線として20期間移動平均線、標準偏差倍率2.0に設定します。

- ストップロス管理システム:14期間ATRをボラティリティ指標として使用し、倍率は3.0とします。ロングポジション保有中は、価格上昇に伴ってストップラインが上方に移動し、ショートポジションの場合は逆方向に移動します。この動的ストップ機構により、利益を自然に伸ばしつつ、ドローダウンを効果的に抑制します。

戦略の優位性

- 適応性の高さ:ボリンジャーバンドとATRは市場の実際の変動に基づいて計算される指標であり、さまざまな市場環境に自動適応できます。

- リスク管理の充実:ATRによる動的ストップロスにより、迅速な損切りが可能であると同時に、強いトレンドから早期に離脱しません。

- シグナルの明確さ:エントリーとエグジットのシグナルは明確な価格ブレイクアウトに基づいており、主観的な判断が不要です。

- 可視性の高さ:チャート上にすべてのシグナルポイントを明確に表示するため、分析や最適化が容易です。

戦略のリスク

- レンジ相場のリスク:明確なトレンドがない市場では、ダマシのブレイクアウトシグナルが頻発し、連続的な損切りにつながる可能性があります。

- スリッページリスク:市場の変動が激しい場合、実際の約定価格が理論上のシグナル価格と大きく乖離する可能性があります。

- パラメータ感応度:戦略の効果はボリンジャーバンドとATRのパラメータ設定に敏感であり、市場環境に応じた最適化が必要です。

戦略の最適化方向

- トレンドフィルターの追加:追加のトレンド判断指標を導入し、明確なトレンドがある場合のみポジションを取ることで、レンジ相場での偽シグナルを削減します。

- ストップパラメータの最適化:市場状況に応じてATR倍率を動的に調整し、ボラティリティが高い場合は緩やかなストップを使用します。

- ポジション管理の導入:ATRに基づく動的なポジションサイジングシステムを設計し、ボラティリティに応じて取引規模を自動調整します。

- 時間フィルターの追加:重要な経済指標発表など高ボラティリティ時間帯の取引を避けます。

まとめ

本戦略は、ボリンジャーバンドとATRトレーリングストップを組み合わせることで、トレンド捕捉とリスク管理を両立した取引システムを構築しています。適応性の高い特性により、さまざまな市場環境で安定性を維持し、明確なシグナルシステムにより客観的な取引根拠を提供します。提案された最適化方向を通じて、戦略にはさらなる改善の余地があります。実際の運用では、投資家は自身のリスク選好や取引銘柄の特性に応じて、パラメータを調整することを推奨します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1