マルチ指標トレンドモメンタムATR目標価格取引戦略

2

Follow

502

Followers

概要

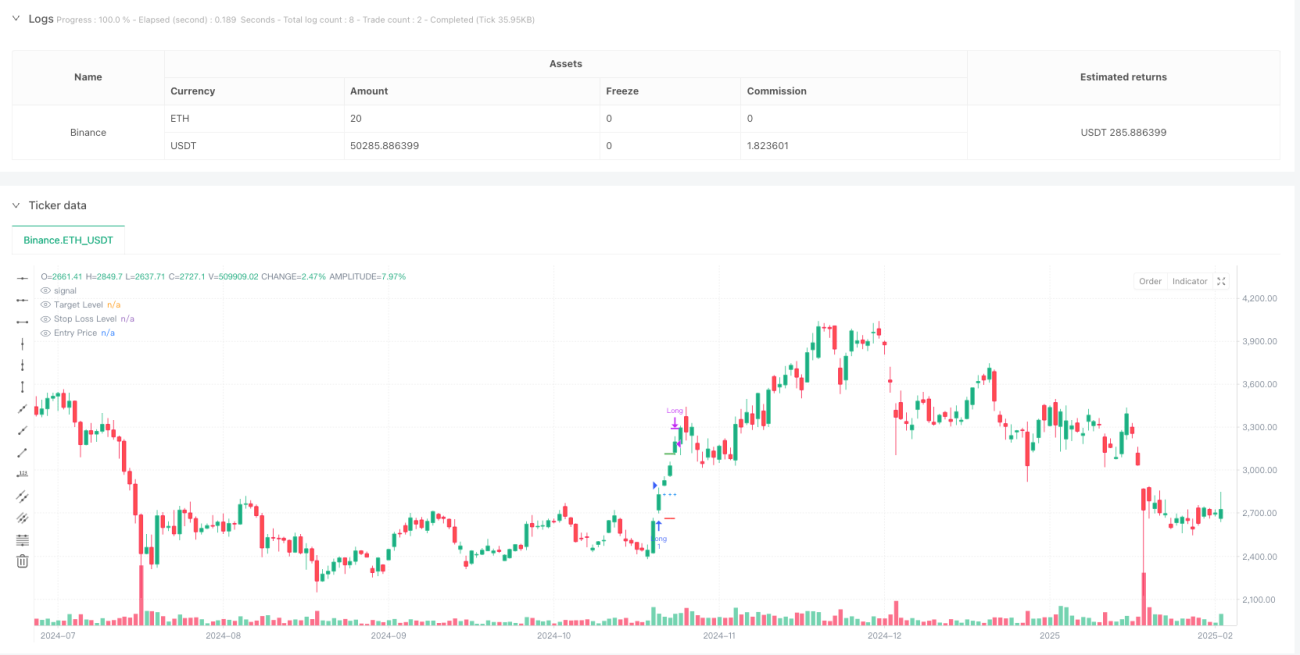

本戦略は、複数のテクニカル指標を組み合わせたトレンド追随型のモメンタム取引システムです。主に平均方向性指標(ADX)、相対力指数(RSI)、平均真のレンジ(ATR)を組み合わせて買いの機会を識別し、ATRを利用して動的な利益確定および損切りの価格を設定します。特に1分足のオプション取引に適しており、厳格なエントリー条件とリスク管理により取引成功率を高めます。

戦略の原理

戦略の核となるロジックは、以下の主要な要素で構成されています。

- トレンド確認:ADXが18より大きく、かつ+DIが-DIよりも大きいことで上昇トレンドを確認します。

- モメンタム検証:RSIが60を突破し、かつその20期間移動平均線よりも上にあることを要求し、価格のモメンタムを検証します。

- エントリーのタイミング:トレンド条件とモメンタム条件が同時に満たされた場合、システムは現在の終値でロングポジションを建てます。

- 目標管理:エントリー時のATR値に基づき、動的な利益確定目標(ATRの2.5倍)と損切りライン(ATRの1.5倍)を設定します。

戦略のメリット

- 多次元的な確認:トレンド指標とモメンタム指標を組み合わせることで、より信頼性の高い取引シグナルを提供します。

- 動的なリスク管理:ATRを使用してストップロス・利食いの位置を動的に調整し、市場のボラティリティ変化に適応します。

- 明確な取引ルール:エントリーとエグジットの条件が明確であり、主観的な判断による混乱を低減します。

- 適応性:戦略のパラメータは、異なる市場環境や取引商品に応じて最適化・調整が可能です。

戦略のリスク

- 偽のブレイクアウトリスク:RSIが60を突破しても偽のシグナルとなる可能性があり、他の指標で確認する必要があります。

- スリッページの影響:1分足の高速な市場では、大きなスリッページリスクに直面する可能性があります。

- 市場環境への依存:トレンドが明確な市場では良好に機能しますが、レンジ相場では頻繁に損切りが発生する可能性があります。

- パラメータ感応度:複数の指標パラメータ設定のバランスが必要であり、不適切なパラメータ組み合わせは戦略のパフォーマンスに影響を与える可能性があります。

戦略の最適化方向

- エントリー最適化:出来高確認メカニズムを追加し、シグナルの信頼性を高めることができます。

- ポジション管理:動的なポジション管理システムを導入し、市場のボラティリティに応じて保有サイズを調整します。

- エグジットメカニズム:トレーリングストップ機能を追加することで、利益をより適切に保護できます。

- 時間フィルター:取引時間帯のフィルターを追加し、ボラティリティが過大または流動性が不足する時間帯を回避します。

まとめ

本戦略は、複数のテクニカル指標を総合的に活用することで、完全な取引システムを構築しています。そのメリットは、トレンド分析とモメンタム分析を組み合わせ、動的なリスク管理方法を採用している点にあります。一定のリスクは存在するものの、適切なパラメータ最適化とリスク管理措置により、実際の取引において安定したパフォーマンスを発揮することが期待できます。実取引で使用する前に、十分なバックテストとパラメータ最適化を行い、取引する商品の特性に応じて適宜調整することをお勧めします。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1