2

Follow

502

Followers

概要

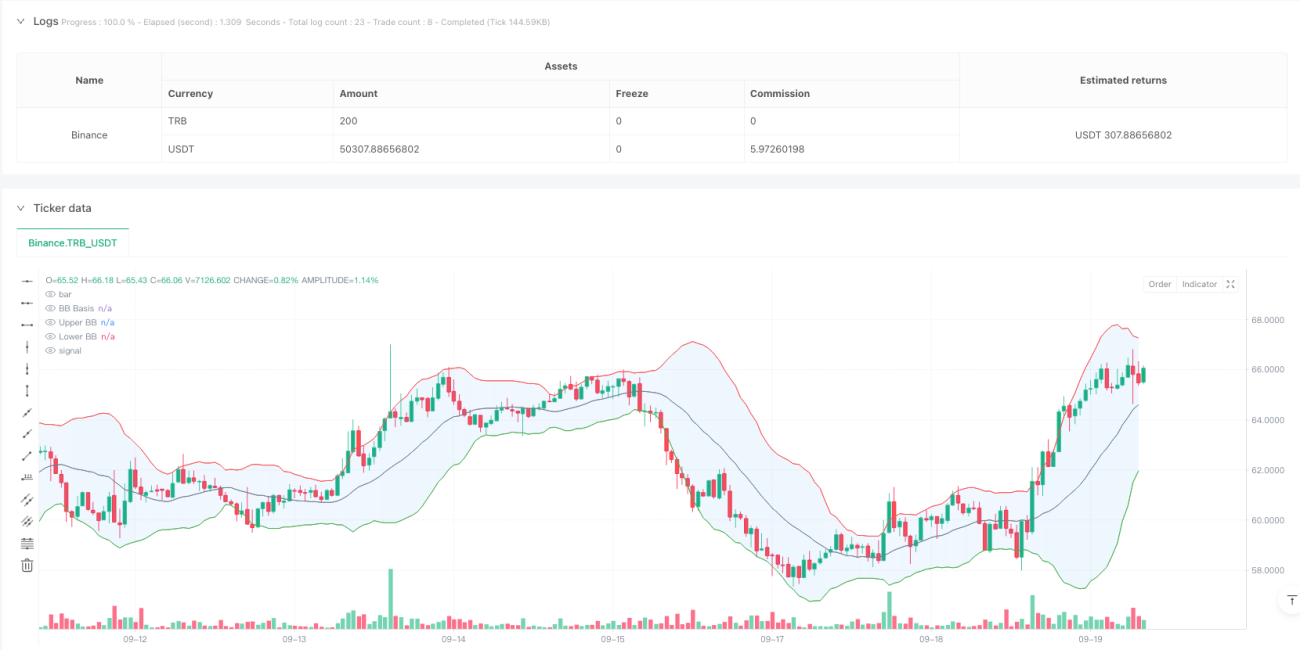

これは、ボリンジャーバンド、MACD(移動平均収束拡散法)、および出来高分析を組み合わせた高頻度取引戦略システムです。本戦略は、価格がボリンジャーバンドの上限・下限を突破し戻る動きを識別し、MACDモメンタム指標と出来高確認を組み合わせて市場の反転機会を捉えます。システムは1日あたりの最大取引回数を制限し、完全なリスク管理メカニズムを備えています。

戦略の原理

戦略は主に以下の3つのコア指標の組み合わせに基づいています。

- ボリンジャーバンド:20期間の単純移動平均線(SMA)を中央バンドとし、標準偏差倍率2.0で上限・下限を計算します。価格がボリンジャーバンドを突破した後、戻る際に潜在的な取引シグナルを発します。

- MACD指標:標準パラメータ設定(12,26,9)を使用し、価格トレンドのモメンタムを確認します。MACDラインがシグナルラインを上回っている場合は買いシグナル、下回っている場合は売りシグナルを確定します。

- 出来高分析:20期間移動平均を使用して出来高を確認し、シグナル発生時の出来高が少なくとも平均水準に達していることを要求し、市場参加度を確保します。

戦略の利点

- 複数シグナル確認:ボリンジャーバンド、MACD、出来高の3重確認により、取引シグナルの信頼性が大幅に向上します。

- 可視化設計:システムはボリンジャーバンドの塗りつぶし、シグナルマーク、背景色の変化など豊富なチャート表示を提供し、トレーダーが取引機会を迅速に識別できるようにします。

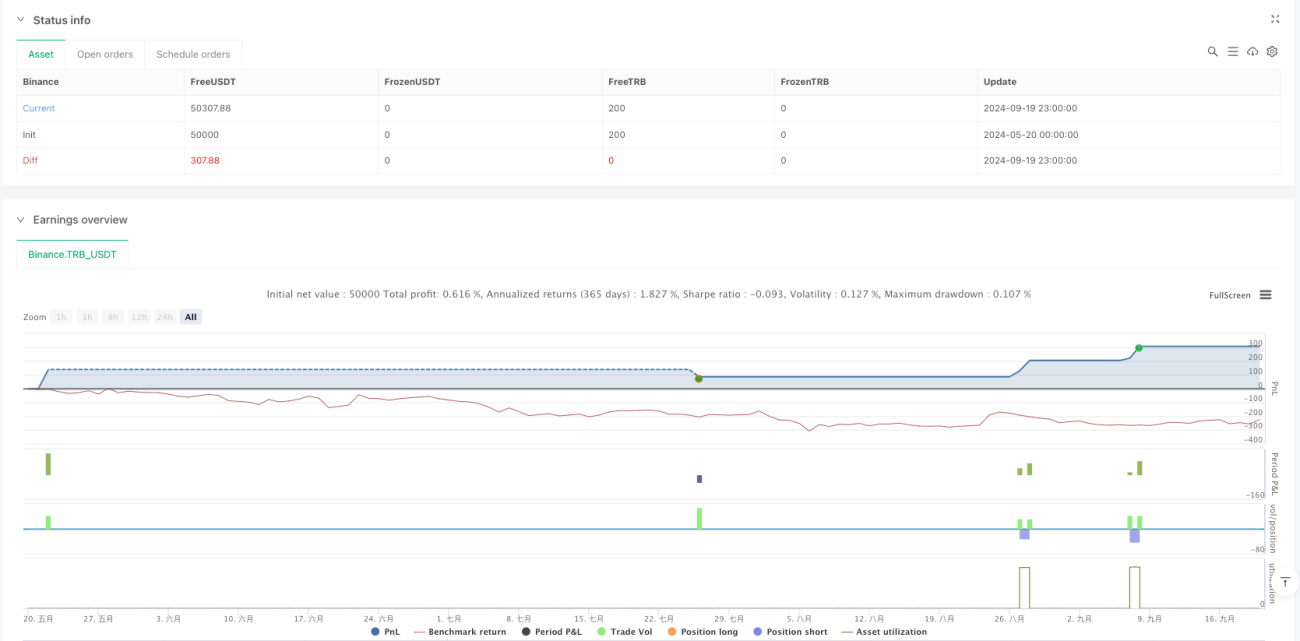

- リスク管理の充実:固定のストップロスと利益確定目標を実施し、1日あたりの最大取引回数を制限することで、リスクエクスポージャーを効果的に管理します。

- システム化された運用:明確なエントリーとエグジット条件を提供し、主観的判断による不確実性を低減します。

戦略のリスク

- 市場変動リスク:変動の激しい市場では、偽のブレイクアウトシグナルが発生し、取引損失を招く可能性があります。

- スリッページリスク:高頻度取引環境では、大きなスリッページコストに直面し、実際の収益に影響を与える可能性があります。

- 流動性リスク:出来高条件により、市場流動性が不十分な場合に取引機会が制限されることがあります。

- システムリスク:固定のパラメータ設定では、市場環境の急激な変化に適応できない可能性があります。

戦略の最適化方向性

- パラメータの動的最適化:適応型パラメータ調整メカニズムを導入し、ボリンジャーバンドとMACDのパラメータが市場条件に応じて自動調整されるようにします。

- 市場サイクルの識別:市場サイクル判断モジュールを追加し、異なる市場サイクルで異なる取引戦略を採用します。

- リスク管理の最適化:動的ストップロスメカニズムを導入し、市場のボラティリティに応じてストップロス位置を調整することを検討します。

- シグナルフィルターの強化:トレンド強度フィルターを追加し、レンジ相場で過剰な取引シグナルが発生するのを防ぎます。

まとめ

本戦略は、ボリンジャーバンドの反転シグナル、MACDトレンド確認、出来高検証を組み合わせることで、完全な取引システムを構築しています。可視化設計と厳格なリスク管理により、特にデイトレードに適しています。一定の市場リスクは存在しますが、継続的な最適化とパラメータ調整により、様々な市場環境で安定したパフォーマンスを発揮することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1