二重移動平均線トレンドクロス定量取引戦略の研究と最適化

2

Follow

502

Followers

概要

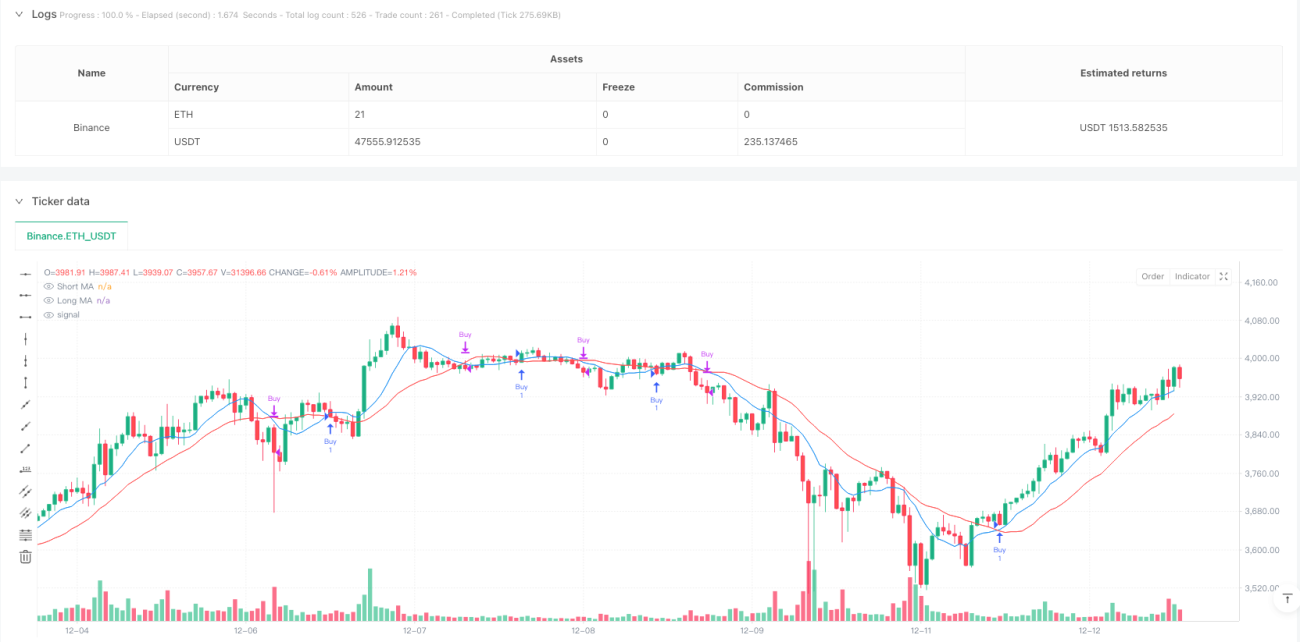

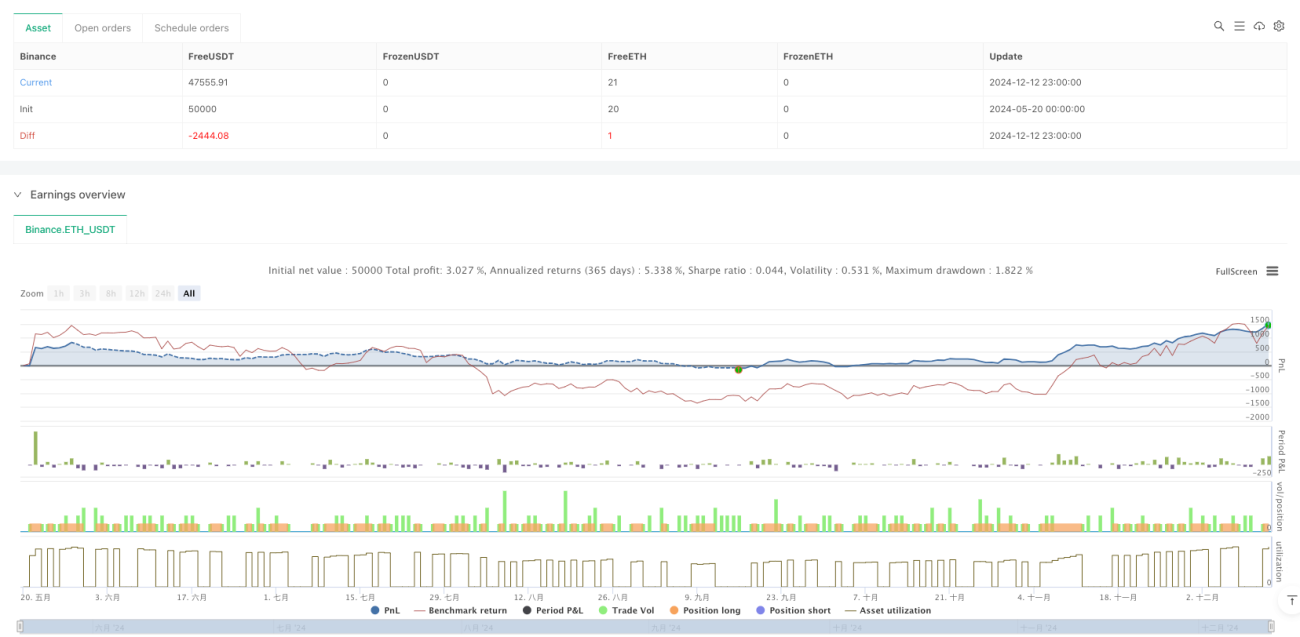

本戦略は、二重移動平均線のクロスを利用したトレンド追従型取引システムです。短期(9日)と長期(21日)の移動平均線の相対的な位置関係を比較することで、市場トレンドの転換タイミングを捉えます。古典的なテクニカル分析理論と現代の定量取引手法を組み合わせ、完全自動化された取引判断プロセスを実現しています。

戦略の原理

戦略のコアロジックは、異なる期間の移動平均線のクロスシグナルに基づきます。短期線(9日)が長期線(21日)を上抜けた場合、システムは市場のモメンタムが上向きに転じたと判断し、ロングシグナルを発します。短期線が長期線を下抜けた場合は、モメンタムが下向きに転じたと判断し、ポジションをクローズします。また、戦略には取引統計機能が含まれており、総取引回数、勝ちトレード数、負けトレード数をリアルタイムで追跡し、トレーダーによる戦略パフォーマンスの評価を支援します。

戦略の優位性

- ロジックがシンプルで明確であり、理解・保守が容易

- 価格データのみに基づいており、複雑な指標を必要としない

- トレンド追従機能を内蔵しており、中長期の相場を効果的に捉えられる

- 完全な取引統計システムを備え、戦略評価に便利

- 完全自動化により、人為的介入による感情的な影響を軽減

戦略のリスク

- レンジ相場では偽のシグナルが頻発する可能性がある

- エントリーとエグジットのタイミングにやや遅れが生じる

- ストップロス機構を設定していないため、急激な変動時に大きな損失を被る可能性がある

- 移動平均線のみに依存し、多面的な市場分析が不足

- パラメータが固定されており、異なる市場環境への適応が難しい

戦略の最適化方向性

- 適応型移動平均線期間を導入し、市場環境への適応性を向上させる

- ボラティリティフィルターを追加し、レンジ相場での偽シグナルを減らす

- 動的ストップロス機構を設計し、下方リスクを管理する

- RSIやMACDなど他のテクニカル指標と組み合わせ、シグナルの信頼性を高める

- 市場環境認識モジュールを開発し、インテリジェントなパラメータ調整を実現する

まとめ

これは古典的かつ実用的なトレンド追従戦略であり、二重移動平均線のクロスを利用して市場のモメンタム変化を捉えます。一定の遅延や偽シグナルのリスクはありますが、そのシンプルで堅実な特性により、定量取引分野における重要なツールとなっています。提案された最適化方向性により、戦略の安定性と収益性はさらに向上することが期待されます。

Source

Pine

Related strategies

Comment

All comments (0)

No data

- 1