2

Follow

502

Followers

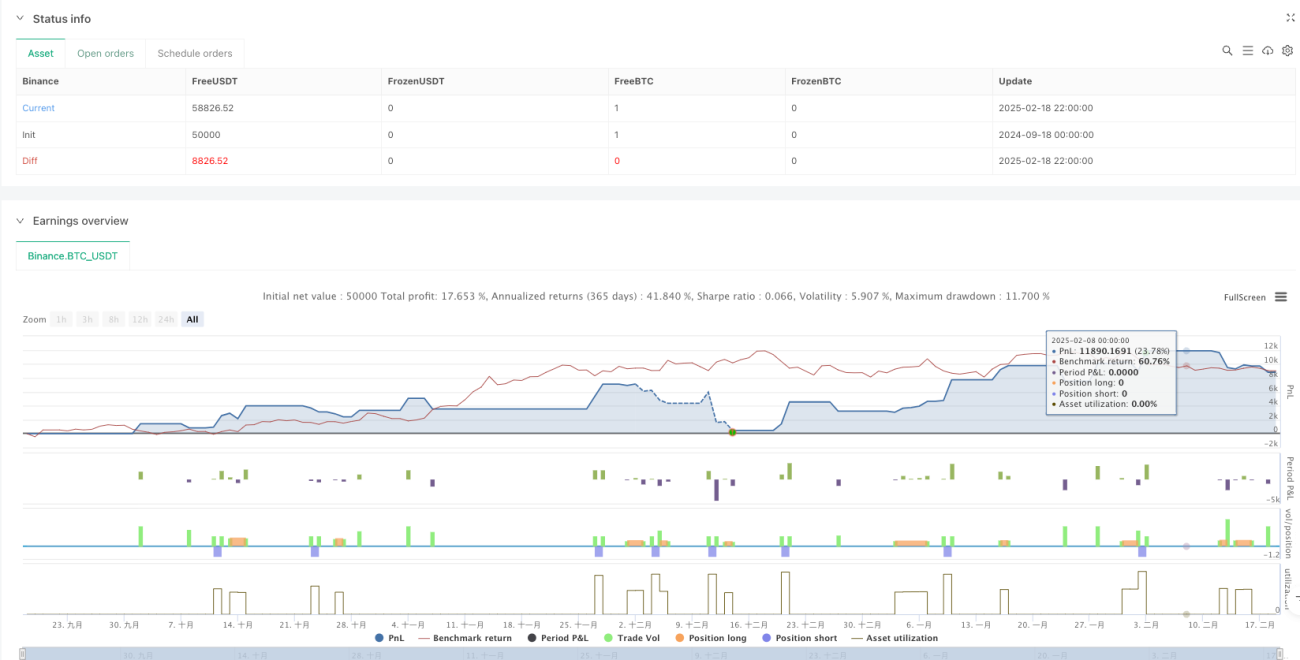

概要

本戦略は、二重移動平均線のクロスシグナルと動的リスク管理を組み合わせた取引システムです。短期および長期の移動平均線のクロスによって取引シグナルを生成し、同時にATR指標を利用してストップや利益確定ポイントを動的に調整し、時間フィルターとクーリングオフ期間を導入して取引の質を最適化します。また、リスクリワード比や1取引あたりのリスク割合の管理メカニズムも含まれています。

戦略の原理

戦略は主に以下の主要な構成要素に基づいています:

- シグナル生成システムでは、短期(10期間)と長期(100期間)の単純移動平均線のクロスを使用して取引をトリガーします。短期平均線が長期平均線を上抜けた場合に買いシグナル、逆の場合は売りシグナルが発生します。

- リスク管理システムでは、14期間のATRに1.5倍の係数を乗じて動的ストップ距離を設定し、利益目標はストップ距離の2倍(調整可能なリスクリワード比)とします。

- 時間フィルターにより、ユーザーは取引の具体的な時間帯を設定でき、指定された時間範囲内でのみ取引を実行します。

- 取引クーリングオフ期間メカニズムでは、10期間の待機時間を設定し、過剰な取引を防止します。

- 1取引あたりのリスクは口座の1%(調整可能)に制御されます。

戦略の利点

- 動的リスク管理:ATR指標を使用して市場のボラティリティに適応し、異なる市場環境で自動的にストップや利益確定距離を調整します。

- 完全なリスク管理:リスクリワード比や1取引あたりのリスク割合を設定することで、体系的な資金管理を実現します。

- 柔軟な時間管理:異なる市場の取引時間帯の特性に応じて取引時間を調整できます。

- 過剰取引の防止:クーリングオフ期間メカニズムにより、激しい変動期に多くの取引シグナルが発生するのを効果的に回避します。

- 視覚化効果:チャート上に取引シグナルと移動平均線が明確に表示され、分析と最適化が容易です。

戦略のリスク

- トレンド反転リスク:レンジ相場では偽のブレイクアウトシグナルが発生し、連続的なストップロスにつながる可能性があります。

- パラメータ感応性:移動平均線の期間やATR倍率などのパラメータの選択が、戦略のパフォーマンスに大きな影響を与えます。

- 時間フィルターの設定が不適切な場合、重要な取引機会を逃す可能性があります。

- 固定されたリスクリワード比は、市場環境によっては柔軟性に欠ける場合があります。

戦略の最適化方向

- トレンド強度フィルターの導入:ADXなどの指標を追加してトレンド強度を判断し、強いトレンド期間のみ取引するようにします。

- 動的リスクリワード比の調整:市場のボラティリティやトレンド強度に応じてリスクリワード比を自動調整します。

- 出来高分析の追加:出来高をシグナル確認の補完指標として利用します。

- クーリングオフ期間の最適化:クーリングオフ期間の長さを市場のボラティリティに応じて動的に調整します。

- 市場環境分類の導入:異なる市場環境で異なるパラメータセットを使用します。

まとめ

本戦略は、古典的なテクニカル分析手法と現代的なリスク管理概念を組み合わせることで、完全な取引システムを構築しています。その中核的な利点は動的リスク管理と多重フィルターメカニズムにありますが、実際の適用においては、特定の市場特性に応じてパラメータを最適化する必要があります。戦略を成功させるには、トレーダーが各構成要素の役割を深く理解し、市場の変化に応じてパラメータを適宜調整することが求められます。提案された最適化方向を通じて、戦略はさまざまな市場環境でより安定したパフォーマンスを達成できる可能性があります。

Source

Pine

/*backtest

start: 2024-09-18 00:00:00

end: 2025-02-19 00:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Profitable Moving Average Crossover Strategy", shorttitle="Profitable MA Crossover", overlay=true)

// Input parameters for the moving averagesStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1