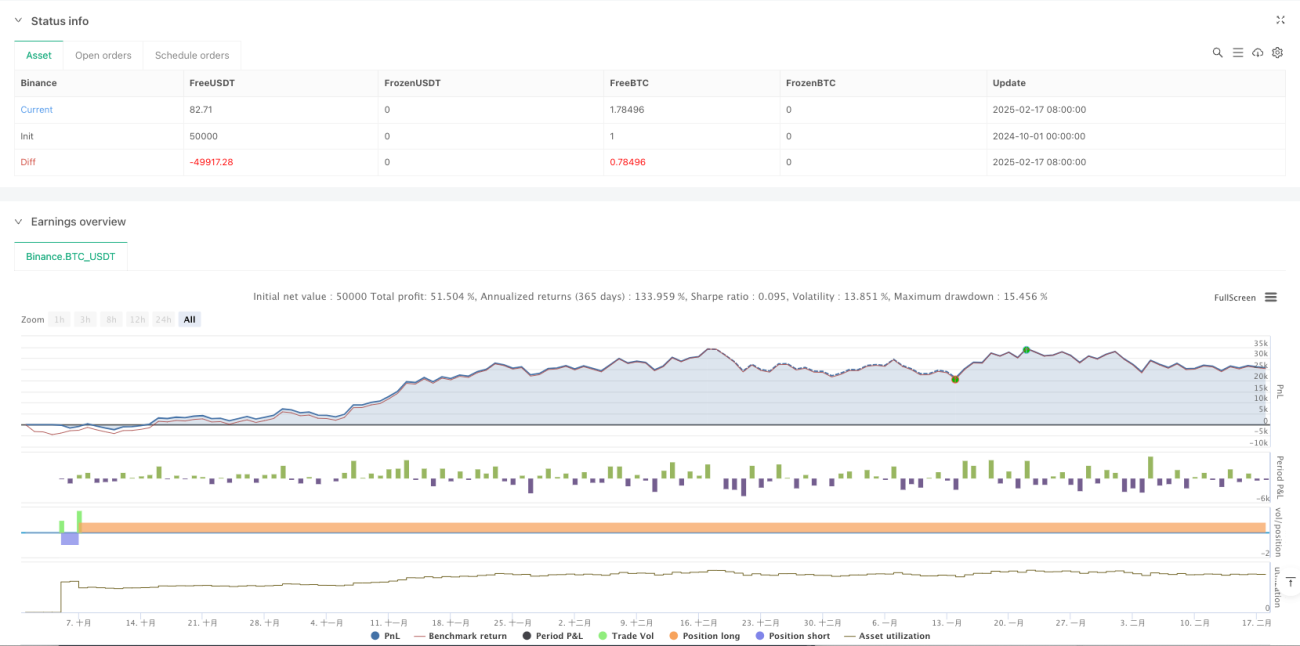

概要

本戦略は、68期間指数移動平均線(EMA)を基盤としたトレンド追跡型取引システムであり、動的なストップロス機構を組み合わせています。この戦略では、価格とEMAのクロスを通じて市場トレンドを識別し、初期ストップロスとトレーリングストップロスを活用してリスクを管理し、トレンド相場での安定した取引を実現します。

戦略の原理

戦略は、68期間EMAを中核指標として市場トレンドを判断します。価格がEMAを上抜けた場合、システムは買いポジションを建て、価格がEMAを下抜けた場合、売りポジションを建てます。リスクを効果的に管理するため、戦略は2層のストップロス保護メカニズム(初期ストップロスとトレーリングストップロス)を設定します。初期ストップロスはエントリー価格から20ポイント離れて設定され、価格が有利な方向に初期ストップロス距離を超えて移動すると、ストップロス価格は10ポイント調整され、一部の利益を確定します。

戦略の利点

- 強力なトレンド追跡能力: 68期間EMAは市場ノイズを効果的にフィルタリングし、中長期トレンドを捉えます。

- 完全なリスク管理: 二重のストップロス機構により、元本を保護しつつ利益を確定できます。

- 高いパラメータ調整可能性: EMA期間やストップロスポイント数などのパラメータは、市場特性に応じて柔軟に調整可能です。

- 明確な戦略ロジック: エントリー・エグジット条件が明確で、実取引での運用と監視が容易です。

- 高い自動化レベル: 戦略はプログラム取引として完全に自動化でき、人為的介入を低減します。

戦略のリスク

-

レンジ相場リスク: ボックス相場では頻繁にストップロスが発動される可能性があります。

対策案: ADXなどのトレンド確認指標を追加する。 -

ギャップリスク: 大きなギャップが発生した場合、実際のストップロス価格が想定から乖離する可能性があります。

対策案: オプションによるヘッジやポジションサイズの調整を検討する。 -

パラメータ最適化リスク: 過度なパラメータ最適化は戦略の有効性を損なう可能性があります。

対策案: サンプル外テストを実施し、パラメータの安定性を確認する。

戦略の改善方向

-

トレンド確認メカニズム: トレンド強度指標(ADX、MACDなど)を導入し、トレンド判断の精度を向上させる。

-

動的パラメータ調整: 市場ボラティリティに応じてEMA期間やストップロスパラメータを自動調整する。

-

ポジション管理の最適化: ボラティリティベースの動的ポジション管理システムを導入する。

-

マルチ期間連携: より長期のトレンド判断と組み合わせ、取引方向の精度を高める。

まとめ

本戦略は、EMAトレンド追跡と動的ストップロス管理を組み合わせることで、完全な取引システムを構築しています。戦略のコアとなる利点は、明確な取引ロジックと完全なリスク管理メカニズムにあります。提案された改善方向を適用することで、戦略の安定性と収益性のさらなる向上が期待できます。本戦略は、安定した収益を追求する中長期投資家に適しています。

- 1