動的適応マルチタイムフレームトレンドフォロー&レンジ反転複合戦略

2

Follow

502

Followers

概要

本戦略は、トレンド追跡とレンジ取引を組み合わせた複合型トレーディングシステムです。一目均衡表を使用して市場状態を識別し、MACDのモメンタム確認とRSIの買われ過ぎ・売られ過ぎ指標を組み合わせ、さらにATRを用いた動的ストップロス管理を実施します。この戦略は、トレンド市場ではトレンド性の機会を捉え、ボラティリティ市場では反転の機会を探すことができ、高い適応性と柔軟性を持ちます。

戦略原理

戦略は多層的なシグナル確認メカニズムを採用しています:

- 一目均衡表を市場状態の主要判断基準として使用し、価格と雲の位置関係から市場がトレンド状態かレンジ状態かを判断します。

- トレンド市場において、価格が雲の上に位置し、かつRSI>55、MACDヒストグラムが正の場合に買いポジションを取ります。価格が雲の下に位置し、かつRSI<45、MACDヒストグラムが負の場合に売りポジションを取ります。

- レンジ市場において、RSI<30かつ確率的RSI<20の場合に買いの機会を探します。RSI>70かつ確率的RSI>80の場合に売りの機会を探します。

- ATRに基づく動的ストップロスを使用してリスクを管理し、ストップロスの距離はATR値の2倍とします。

戦略の利点

- 市場適応性が高い:異なる市場状態に応じて自動的に取引戦略を調整し、戦略の安定性を高めます。

- シグナルの信頼性が高い:複数の指標による検証メカニズムを採用し、誤シグナルの影響を低減します。

- リスク管理が充実:ATRによる動的ストップロスにより、利益を十分に伸ばすと同時にリスクを効果的に抑制します。

- 視覚効果が良い:背景色で市場状態を表示し、トレーダーが市場環境を直感的に理解しやすくなります。

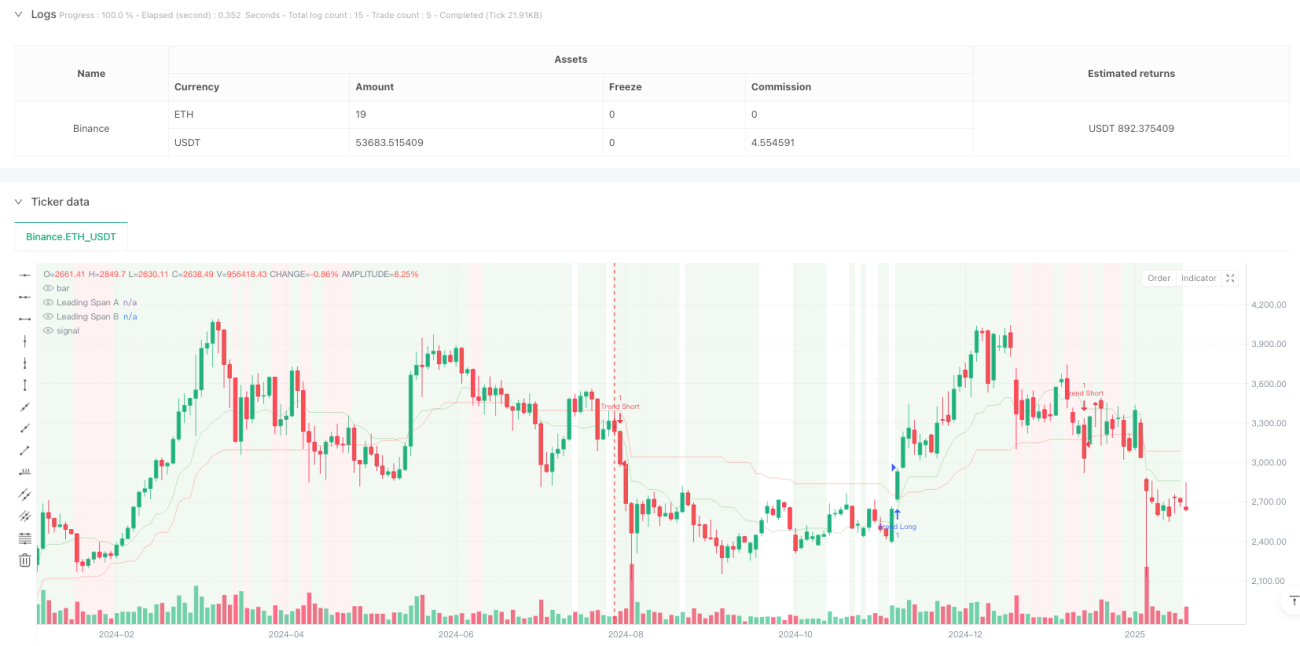

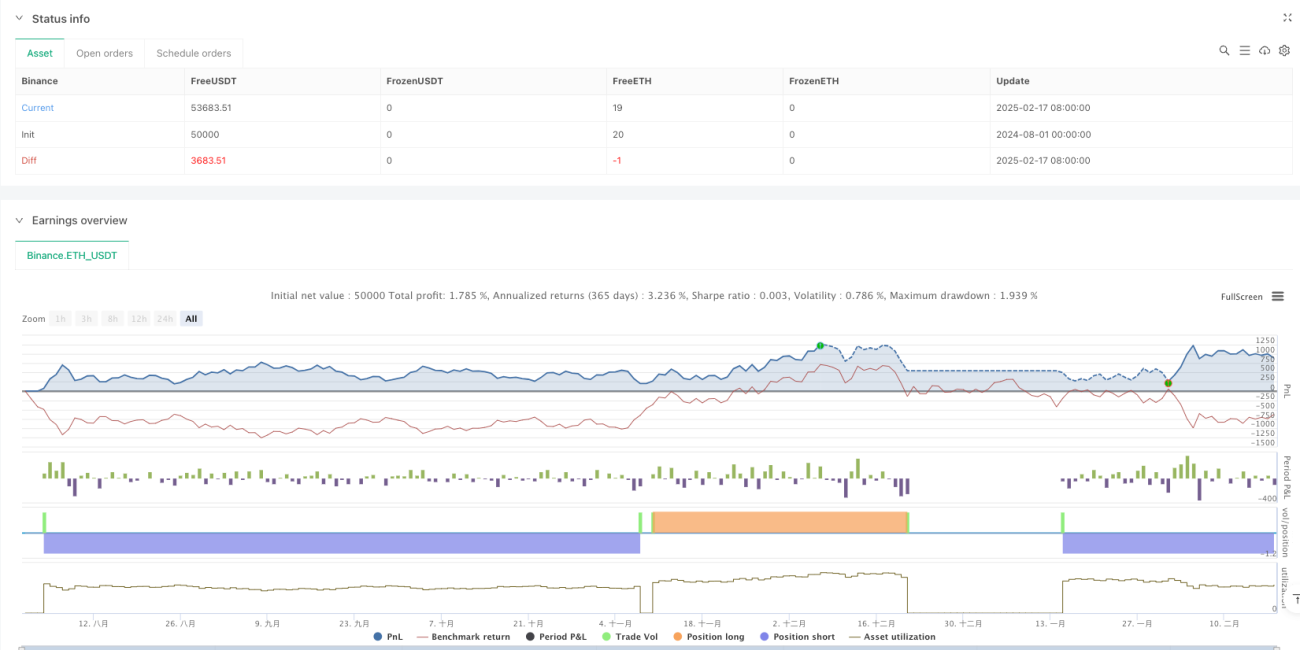

- 高時間足でのパフォーマンスが優れている:日足ではプロフィットファクターが2.159、純利益率が10.71%に達しています。

戦略のリスク

- 勝率が低い:各時間足の勝率が40%未満であり、強い心理的耐性が必要です。

- 低時間足での過剰取引:4時間足で430件の取引を実行しており、効率が低いです。

- シグナルの遅延:複数の指標による検証を使用するため、一部の市場機会を逃す可能性があります。

- パラメータ最適化が難しい:複数の指標を組み合わせることで、戦略最適化の複雑さが増します。

戦略の最適化方向

- シグナルフィルターの最適化:各指標の閾値を調整して勝率を向上させることができます。

- 時間足の適合:主に日足以上の時間足での使用を推奨し、市場特性に応じてパラメータを調整できます。

- ストップロスの最適化:市場状態に応じてATR倍率を動的に調整することを検討できます。

- エントリータイミングの最適化:出来高確認や価格パターン確認を追加してエントリー精度を向上させることができます。

- ポジション管理の最適化:シグナルの強さに基づいて動的なポジション管理システムを設計できます。

まとめ

本戦略は、設計が合理的でロジックが明確な総合取引システムです。複数の指標を組み合わせることで、市場状態のインテリジェントな識別と取引機会の正確な捕捉を実現しています。低時間足ではいくつかの問題がありますが、日足などの高時間足では優れたパフォーマンスを示しています。トレーダーは実運用時には日足レベルのシグナルに重点を置き、自身のリスク許容度に応じてパラメータを適切に調整することをお勧めします。継続的な最適化と調整を通じて、本戦略はトレーダーに安定した利益機会を提供することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1