2

Follow

502

Followers

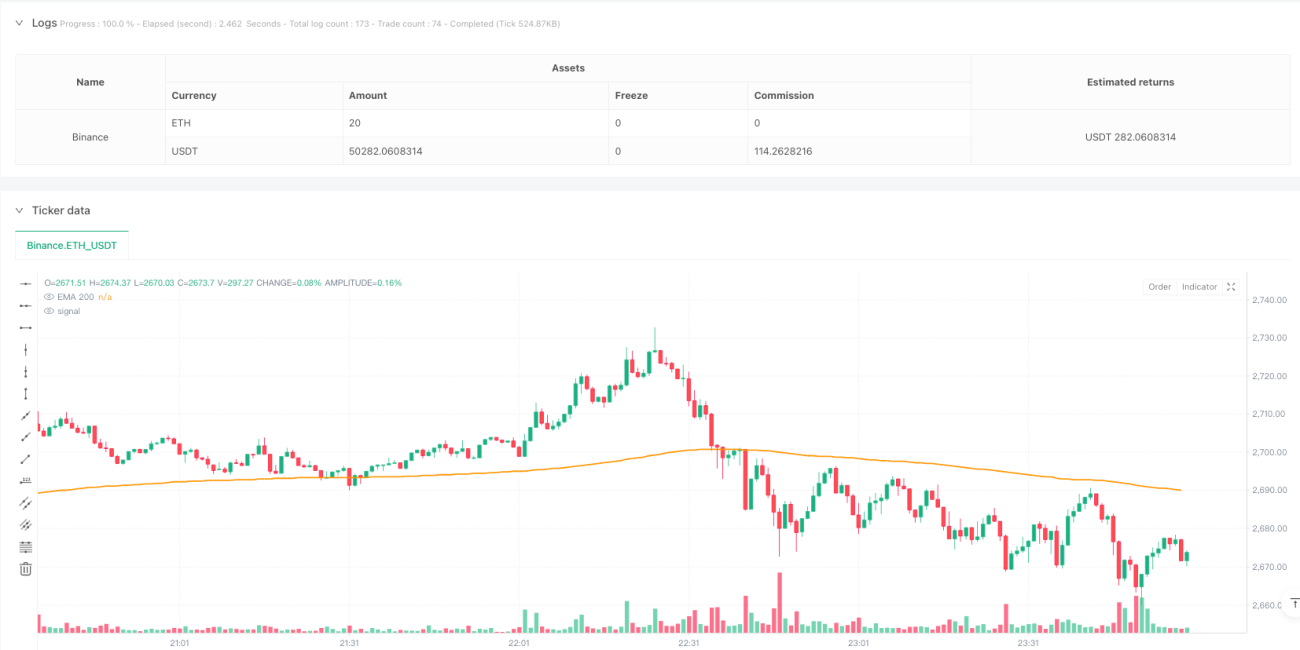

概要

本戦略は、MACDモメンタム指標とEMA移動平均線を組み合わせた双方向取引システムです。主にMACD指標のクロスシグナルと、価格のEMA(200)に対する位置に基づいてエントリータイミングを判断します。戦略は2:1のリスク・リワード比を採用し、5分足で動作可能であり、柔軟なパラメーター調整に対応しています。

戦略の原理

戦略のコアロジックは、以下の主要条件に基づいています。

- 買いエントリー条件:

- 価格がEMA(200)より上にある

- MACDラインがシグナルラインを下から上にクロスする

- MACD値がゼロラインより下にある

- 売りエントリー条件:

- 価格がEMA(200)より下にある

- MACDラインがシグナルラインを上から下にクロスする

- MACD値がゼロラインより上にある

- リスク管理はあらかじめ設定されたストップロスと利食い比率(デフォルト1:2)を用いる

戦略の優位性

- ロジックが明確かつシンプルで、理解・実装が容易

- トレンド指標とモメンタム指標を組み合わせ、より信頼性の高い取引シグナルを提供

- 柔軟なパラメーター設定が可能で、異なる市場環境に応じて最適化できる

- 双方向取引に対応し、市場機会を十分に捉えられる

- リスク管理メカニズムを内蔵し、資金の保護に役立つ

戦略のリスク

- レンジ相場では頻繁な偽シグナルが発生する可能性がある

- 固定されたストップロス・利食い比率はすべての市場環境に適しているとは限らない

- 市場の変動性の変化に敏感

- 頻繁な取引により高い手数料が発生する可能性がある

- 急激な相場変動時には一部の機会を逃す恐れがある

戦略の最適化方向

- ボラティリティ指標を導入し、ストップロスと利食い水準を動的に調整する

- 出来高確認シグナルを追加し、エントリーの質を高める

- 市場環境フィルターを追加し、不利な条件での取引を回避する

- 動的なパラメーター最適化システムを実装する

- 時間フィルターを追加し、低流動性時間帯の取引を避ける

まとめ

これは合理的に設計された戦略システムであり、テクニカル指標を組み合わせることで比較的信頼性の高い取引シグナルを提供します。潜在的なリスクは存在するものの、適切な最適化とリスク管理により、実戦での応用可能性は高いです。実運用前に十分なバックテストを行い、具体的な市場状況に応じてパラメーターを調整することを推奨します。

Source

Pine

Strategy parameters

Comment

All comments (0)

No data

- 1