2

Follow

502

Followers

概要

これは、複数の統計バンドとトレンド分析を組み合わせた取引戦略です。ボリンジャーバンド、分位数バンド、べき乗則バンドを組み合わせて、重要なサポート/レジスタンスゾーンを特定し、上分位数バンドの下標準偏差線をトリガーシグナルとして、エントリーとエグジットのタイミングを決定します。戦略は市場のボラティリティを十分に考慮し、複数の統計手法を重ねることでシグナルの信頼性を高めています。

戦略の原理

戦略の核となる原理は、複数の統計バンドの交差を利用して市場のトレンドを捉えることです。主な構成要素は以下の通りです。

- ボリンジャーバンドシステム - 価格の変動範囲を判断し、価格が上限バンドを突破すると黄色の警告を表示します。

- 分位数バンドシステム - 価格の上下分位数を計算し、価格の極値確率を評価します。

- べき乗則バンドシステム - 過去のリターンに基づいて有意水準を計算し、買われ過ぎ/売られ過ぎを測定します。

- トリガーシステム - 上分位数バンドの下標準偏差線を主要なトリガーシグナルとし、価格がこのライン以上に維持される場合に強気シグナルとみなします。

- 確認システム - 連続確認ローソク足数を設定することで、偽のシグナルをフィルタリングします。

戦略の利点

- シグナルの安定性が高い - 複数の統計バンドを重ねて使用することで、偽のシグナルを効果的に低減します。

- 適応性が良好 - 異なる時間枠や市場状況に適応できます。

- リスク管理が充実 - 複数の統計バンドでリスクゾーンを区分し、ストップロスメカニズムも備えています。

- パラメータの柔軟性 - 豊富なパラメータオプションを提供し、異なる市場特性に合わせて最適化できます。

- 視覚化が明確 - 各指標ラインの色分けが明確で、取引シグナルが直感的に把握できます。

戦略のリスク

- 遅延リスク - 統計指標はいずれも一定の遅延が生じるため、最適なエントリーポイントを逃す可能性があります。

- レンジ相場に不利 - 横ばいのレンジ相場では、過剰な取引シグナルが発生する可能性があります。

- パラメータ感度 - 異なるパラメータの組み合わせで結果が大きく異なるため、繰り返しの最適化が必要です。

- 計算負荷が大きい - 複数の統計指標のリアルタイム計算には、大きな計算リソースが必要です。

- 市場環境への依存 - 極端な市場環境では統計的な法則が機能しなくなる可能性があります。

戦略の最適化方向性

- 動的パラメータの導入 - 市場のボラティリティに応じて各パラメータを自動調整します。

- 市場環境判断の追加 - トレンド強度指標を追加し、レンジ相場のシグナルをフィルタリングします。

- 計算効率の最適化 - 一部の計算プロセスを簡略化し、リソース消費を削減します。

- リスク管理の強化 - より多くのストップロス条件とポジション管理戦略を追加します。

- 適応性の向上 - 自己適応型のパラメータ最適化システムを開発します。

まとめ

これは、複数の統計手法を融合した総合的なトレンドフォロー戦略です。ボリンジャーバンド、分位数バンド、べき乗則バンドの相乗効果により、市場トレンドを適切に捉え、リスク管理能力にも優れています。ある程度の遅延性やパラメータ最適化の難しさはあるものの、継続的な改良と最適化により、実用的な価値と発展の可能性を秘めた戦略です。

Source

Pine

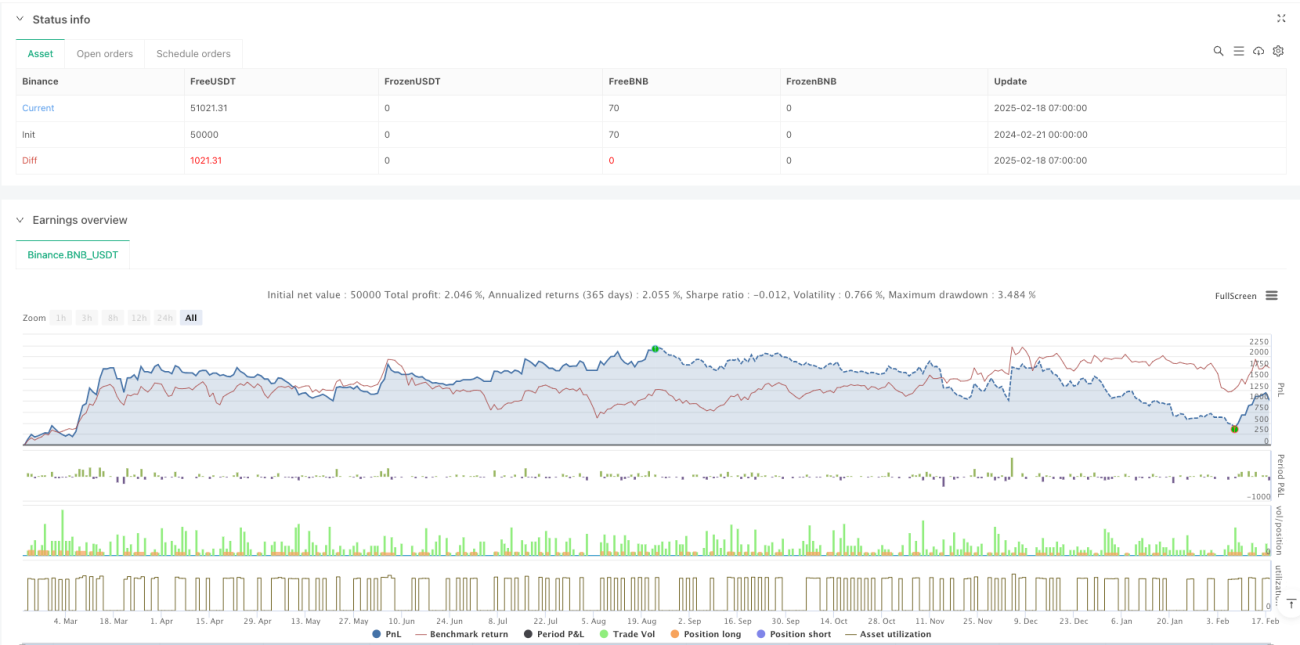

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BNB_USDT"}]

*/

//@version=6

strategy("Multi-Band Comparison Strategy with Separate Entry/Exit Confirmation", overlay=true,

default_qty_type=strategy.percent_of_equity, default_qty_value=10,

initial_capital=5000, currency=currency.USD)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1