# マルチレベルEMAとRSI動的勢い強度に基づくビットコインクロスサイクルトレンド取引戦略

2

Follow

502

Followers

概要

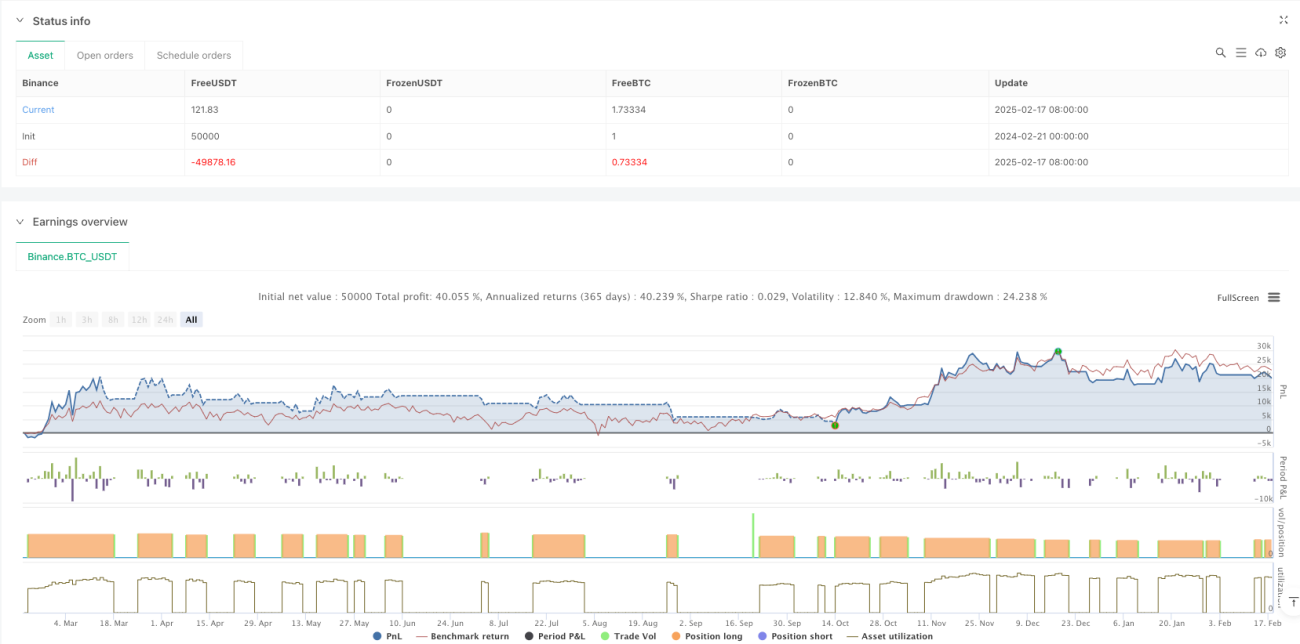

本戦略は、複数時間枠分析に基づくトレンド追跡取引システムであり、週足と日足レベルのEMA移動平均線およびRSIインジケーターを組み合わせて市場のトレンドとモメンタムを識別します。複数の時間枠におけるトレンドの一致性を利用して取引機会を判断し、ATRベースの動的ストップロスでリスクを管理します。資金管理方式として、1回の取引で口座資金の100%を使用し、0.1%の取引手数料を考慮しています。

戦略の原理

戦略の核心理論は以下の主要要素に基づいています。

- 週足レベルのEMAを主要なトレンドフィルターとして使用し、日足終値と週足EMAの関係から市場状態を判断します。

- ATRインジケーターによりトレンド判定のしきい値を動的に調整し、戦略の適応性を高めます。

- RSIモメンタムインジケーターを追加の取引フィルター条件として統合します。

- 7日間の最安値とATRに基づくトレーリングストップロスシステムを使用します。

- 過度の上昇を示す警告シグナルが発生した場合、リスク回避のために新規ポジションを停止します。

戦略の利点

- 複数時間枠分析により、より包括的な市場視点が得られ、偽のブレイクアウトを効果的にフィルターできます。

- 動的ストップロス機構は市場のボラティリティに応じて適応的に調整され、柔軟なリスク管理を提供します。

- RSIモメンタムフィルターはトレンドの強さを確認し、エントリーの質を向上させます。

- 過度の上昇に対する警告メカニズムを備えており、ドローダウンリスクの回避に役立ちます。

- 戦略のパラメータ調整が容易であり、さまざまな市場環境に応じて最適化できます。

戦略のリスク

- レンジ相場では頻繁にエントリー・エグジットを繰り返し、取引コストが増加する可能性があります。

- 100%の資金を用いた取引は大きなドローダウンリスクを伴います。

- テクニカル指標に依存するため、市場の突発的なイベントに対して迅速に対応できない可能性があります。

- 複数時間枠分析では、異なるレベルで矛盾したシグナルが発生することがあります。

- トレーリングストップロスは激しい変動時に早期にトリガーされる可能性があります。

戦略の最適化方向性

- ボラティリティフィルターを導入し、低ボラティリティ期間中の取引頻度を減らします。

- ポジション管理システムを追加し、市場状態に応じて保有比率を動的に調整します。

- ファンダメンタル指標を統合し、追加の市場環境判断を提供します。

- トレーリングストップロスパラメータを最適化し、異なる市場局面に適応できるようにします。

- 出来高分析を追加し、トレンド判定の精度を高めます。

まとめ

本戦略は、構造が整い、ロジックが明確なトレンド追跡戦略です。複数時間枠分析と動的指標フィルタリングにより、主要なトレンドをうまく捉えることができます。固有のリスクは存在するものの、パラメータ最適化や補助指標の追加により、改善の余地は十分にあります。実取引に使用する前に十分なバックテストを実施し、具体的な市場環境に応じてパラメータ設定を調整することを推奨します。

Source

Pine

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

// @version=6

strategy("Bitcoin Regime Filter Strategy", // Strategy name

overlay=true, // The strategy will be drawn directly on the price chart

initial_capital=10000, // Initial capital of 10000 USDStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1