多層級RSIクロス回帰増倉戦略

2

Follow

502

Followers

概要

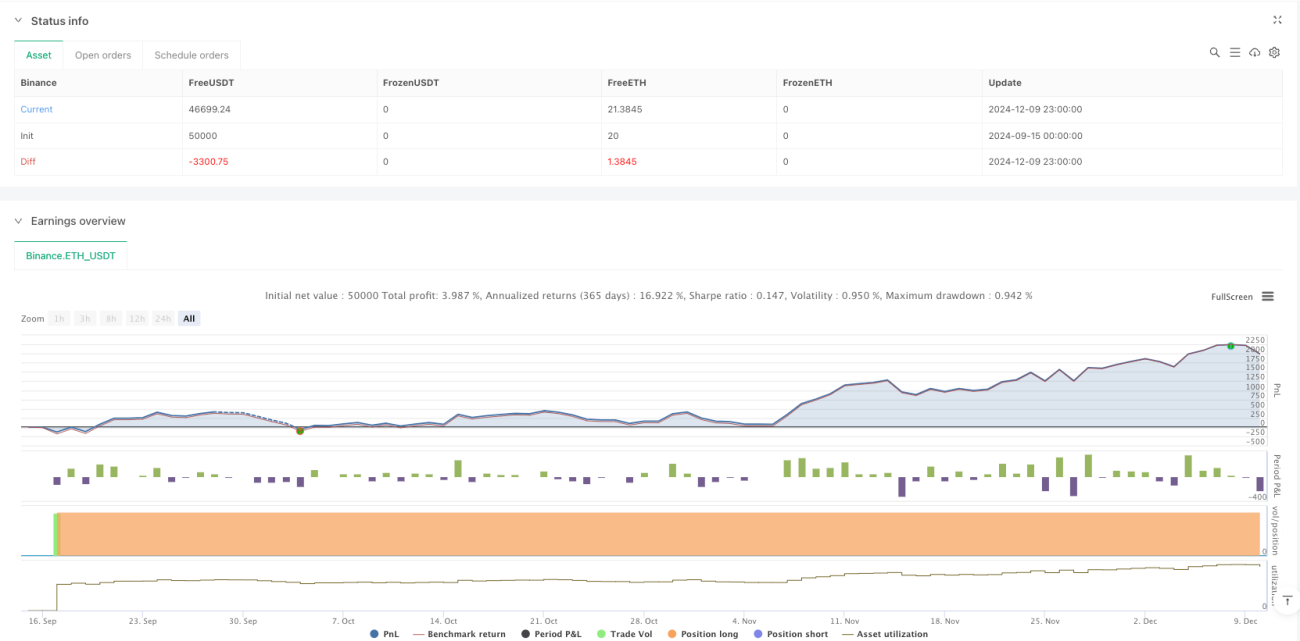

本戦略は、相対力指数(RSI)に基づく自動売買システムであり、主に市場の売られ過ぎ状態を識別することで、反発の可能性を捉えます。戦略は段階的なポジション構築方式を採用し、RSIが低水準でクロスした際に複数のポジションを徐々に構築し、利益目標を設定してリスク管理を行います。システムは柔軟な資金管理メカニズムを備えており、各取引では口座総額の6.6%を使用し、最大15回のピラミッディングによる追加ポジション取得を許可します。

戦略の原理

戦略の核となるロジックは、以下の主要な要素に基づいています。

- エントリーシグナル:14期間のRSI指標が28.5の売られ過ぎ水準を下回ったときに買いシグナルが発生します。

- ポジション管理:1回のポジション構築には口座残高の6.6%を使用し、最大15回までの段階的なポジション追加を許可します。

- 利益確定:価格が建玉平均単価の900%上昇に達した時点で、保有ポジションの50%を決済します。

- 可視化表示:チャート上に売買シグナル、RSI曲線、エントリー価格、目標価格を表示します。

この戦略は、RSI指標の売られ過ぎ領域における動きを観察して相場の方向性を判断し、売られ過ぎシグナルが発生した場合に段階的にポジションを構築することで、建玉コストを低減します。

戦略の利点

- システム化されたポジション構築:事前設定されたRSIパラメータにより取引機会を自動的に識別し、人的判断による主観的バイアスを回避します。

- リスク分散:段階的なポジション構築方式を採用し、異なる価格帯で複数のポジションを保有することでリスクを効果的に分散します。

- 柔軟な適応性:戦略パラメータは、異なる市場環境や個人のリスク許容度に応じて調整可能です。

- 利益保護:明確な利益目標を設定し、目標達成時に自動的にポジションを縮小して利益の一部を確定します。

- 資金効率:適切なポジションコントロールと追加ポジション機構により、資金の使用効率を向上させます。

戦略のリスク

- トレンドリスク:強い下落トレンドでは、ポジション構築シグナルが頻繁に発生し、資金損失につながる可能性があります。

- パラメータ感度:RSIパラメータやポジション構築比率の設定が不適切な場合、戦略のパフォーマンスに影響を与える可能性があります。

- 市場流動性:流動性の低い市場では、目標価格で取引を完了することが困難な場合があります。

- 資金管理:過度なポジション追加により、リスクエクスポージャーが過大になる可能性があります。

解決策:

- トレンドフィルターを追加し、明確な下落トレンドではポジション構築を停止します。

- バックテストを通じてパラメータ設定を最適化します。

- 最大ドローダウン制限を設定します。

- 追加ポジションの閾値を動的に調整します。

戦略の最適化方向

- 動的パラメータ:市場のボラティリティに応じてRSIパラメータとポジション構築条件を自動調整します。

- ストップロス機構:トレーリングストップロス機能を追加し、リスク管理を強化します。

- 市場フィルター:出来高やトレンドなどのフィルター条件を追加し、シグナルの品質を向上させます。

- エグジット最適化:より柔軟な利益確定メカニズムを設計します(例:段階的なポジション縮小)。

- リスク管理:最大ドローダウン制限とリスクエクスポージャーのコントロールを追加します。

まとめ

本戦略は、RSI指標を用いて売られ過ぎの機会を識別し、ピラミッディングによるポジション追加と固定比率による利益確定を組み合わせることで、完全な取引システムを構築しています。戦略の利点はシステム化された運用とリスク分散にありますが、市場トレンドやパラメータ設定が戦略のパフォーマンスに与える影響に注意する必要があります。動的パラメータ調整、ストップロス機構、市場フィルターなどの最適化対策を追加することで、戦略の安定性と収益性をさらに向上させることができます。

Source

Pine

/*backtest

start: 2024-09-15 00:00:00

end: 2024-12-10 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("RSI Cross Under Strategy", overlay=true, initial_capital=1500, default_qty_type=strategy.percent_of_equity, default_qty_value=6.6)

// Input parametersStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1