2

Follow

502

Followers

概要

本戦略は、市場トレンド、モメンタム、ボラティリティの3次元分析を組み合わせたマルチインジケーター統合型トレンド追従取引システムです。中核ロジックは、一目均衡表(Ichimoku Cloud)で市場トレンドを判断し、MACDヒストグラムでモメンタムを確認、ボリンジャーバンド幅(Bollinger Band Width)で市場のボラティリティ状態をフィルタリングし、さらに週足レベルのトレンド確認メカニズムを導入し、最後にATRベースの動的ストップロスでリスクを管理します。

戦略の原理

本戦略は多層シグナルフィルタリングメカニズムを採用しています。まず、一目均衡表の先行スパンAとBを用いて価格が雲の上か下かを判断し、市場の大トレンドを決定します。次に、MACDヒストグラムでモメンタムの強さを判断し、ロング時はヒストグラムが-0.05より大きく、ショート時は0未満であることを要求します。第三に、週足時間軸の50期間移動平均線を導入し、より大きなトレンド方向を確認します。第四に、ボリンジャーバンド幅指標で低ボラティリティ相場をフィルタリングし、幅が0.02より大きい場合のみポジションを取ります。ストップロス設定は、市場のボラティリティ状態に応じて適応的に変化します。低ボラティリティ時には前期の高値・安値を使用し、高ボラティリティ時にはATR倍率を使用します。

戦略の利点

- 多次元シグナルフィルタリング:トレンド、モメンタム、ボラティリティの3次元インジケーターを組み合わせることで、偽のシグナルを効果的に低減します。

- 複数時間枠分析:週足トレンド確認を導入し、取引方向の精度を向上させます。

- 動的リスク管理:ATRとボリンジャーバンド幅に基づく適応的ストップロスメカニズムにより、利益を保護しつつトレンドの展開余地を残します。

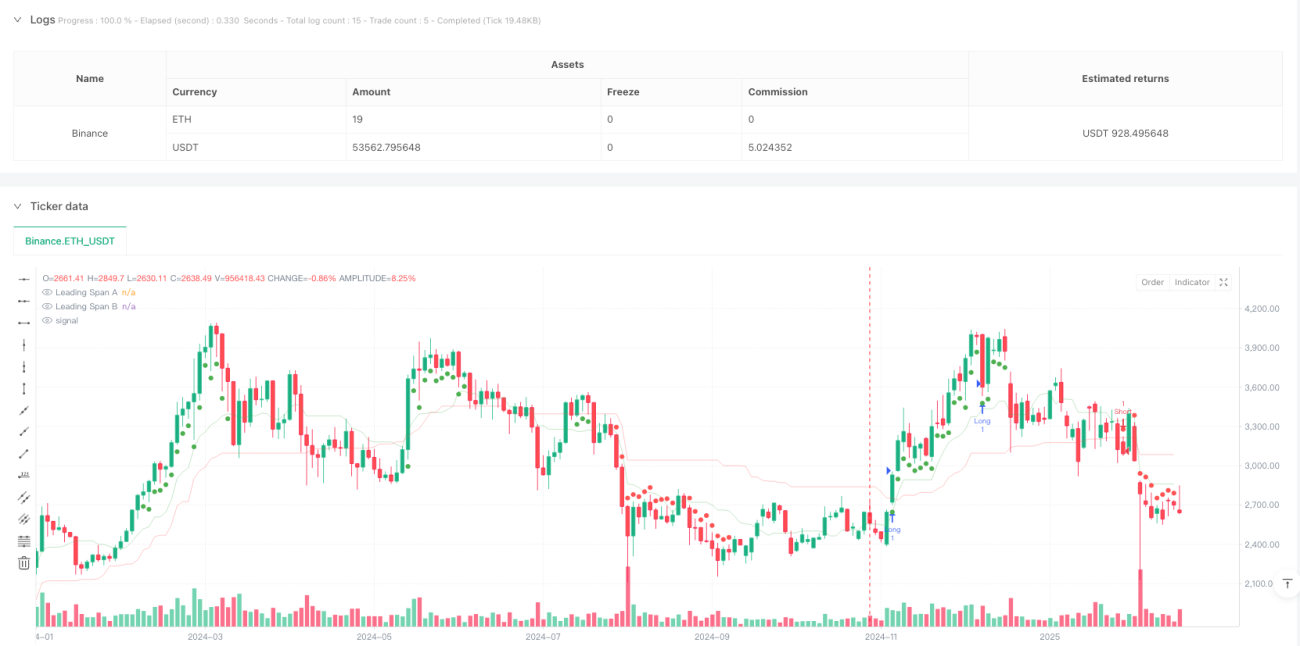

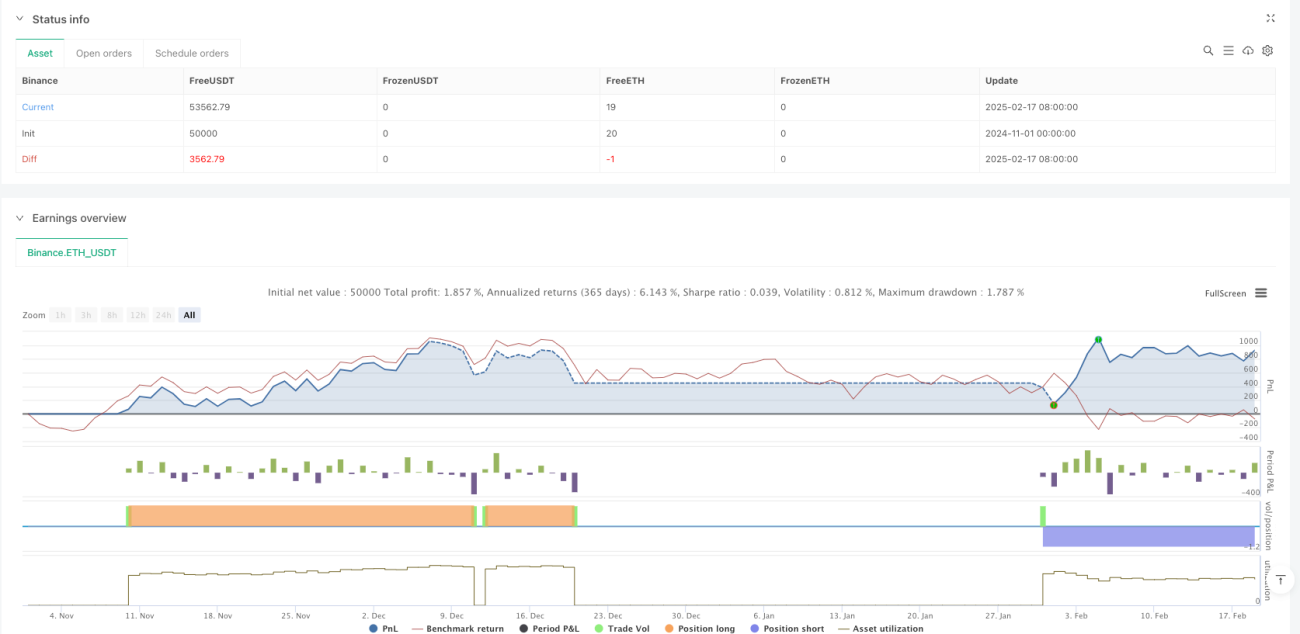

- バックテスト結果が優秀:純利益10.80%、利益損失比率2.593、勝率50.70%、最大ドローダウンはわずか1.47%。

戦略のリスク

- トレンド依存性:レンジ相場では、偽のシグナルが頻発する可能性があります。

- パラメータ感度:複数のインジケーターパラメータを市場環境に応じて最適化する必要があります。

- 遅延リスク:多重シグナルフィルタリングにより、エントリータイミングが遅れ、一部の相場を逃す可能性があります。

- バックテストの限界:過去のパフォーマンスは将来の結果を保証するものではなく、実運用ではスリッページや手数料も考慮する必要があります。

戦略の最適化方向

- シグナルシステムの最適化:RSIなどの他のモメンタム指標を導入し、シグナルの信頼性を向上させることができます。

- ポジション管理の最適化:ボラティリティに基づいてポジションサイズを動的に調整できます。

- 利確メカニズムの最適化:トレーリングストップやテクニカル指標に基づく利確条件を追加できます。

- 市場適応性の最適化:市場状態に応じてパラメータを動的に調整します。

まとめ

本戦略は、多次元インジケーター統合と複数時間枠分析により、完全なトレンド追従システムを構築し、動的リスク管理メカニズムを備えています。バックテストのパフォーマンスは優秀ですが、市場環境の変化によるリスクに留意する必要があり、実運用では慎重な検証と継続的な最適化を推奨します。

Source

Pine

/*backtest

start: 2024-11-01 00:00:00

end: 2025-02-19 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © FIWB

//@version=6

strategy("Momentum Edge Strategy - 1D BTC Optimized", overlay=true)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1