2

Follow

502

Followers

概要

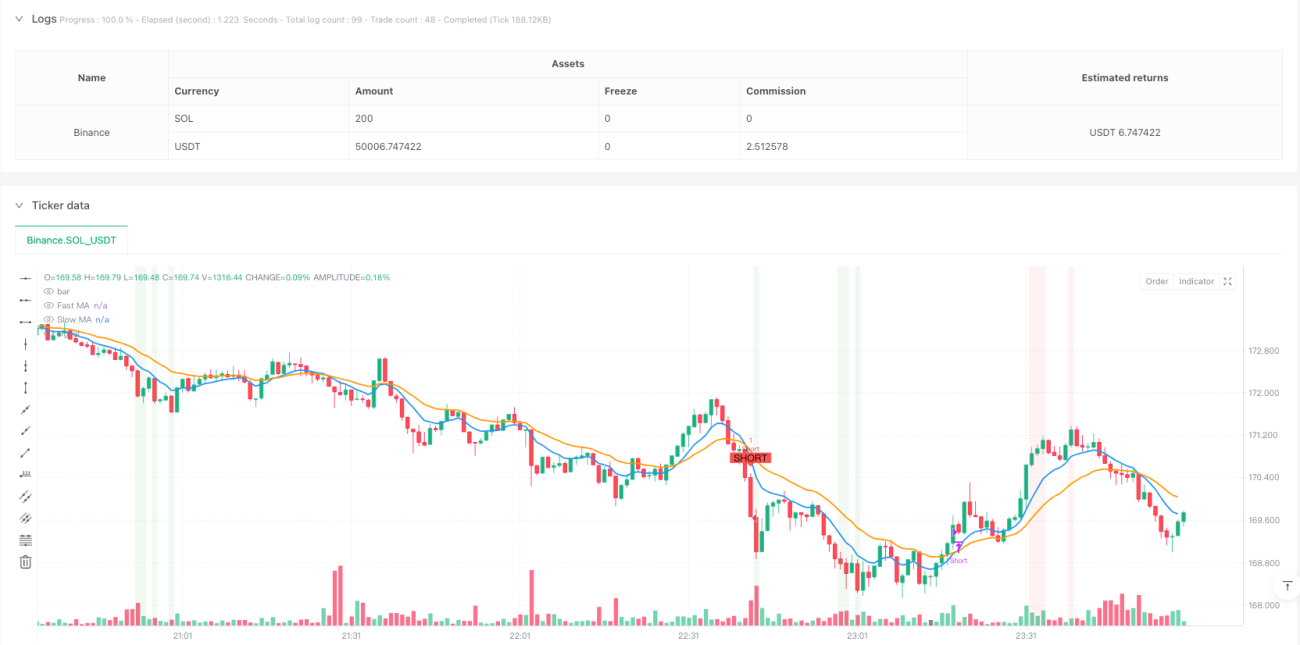

本戦略は、トレンド追跡とモメンタム取引に基づくインテリジェントな取引システムであり、主に短期および高速取引シーン向けに設計されています。戦略の中核は、指数移動平均線(EMA)クロス、相対力指数(RSI)、平均真實レンジ(ATR)を組み合わせた判定システムであり、パーセンテージベースのスマートストップロス機構を備えています。本戦略は特に1分足や5分足などの短い時間枠のチャート取引に適しており、パラメータを動的に調整することで様々な市場環境に対応します。

戦略の原理

戦略は3つのコアテクニカル指標を用いて取引シグナルシステムを構築しています:

- 短期・長期指数移動平均線(EMA)クロスシステム – 9期間と21期間のEMAを組み合わせ、ゴールデンクロスとデッドクロスでトレンド方向を判断します。

- RSIの買われすぎ・売られすぎフィルター – 14期間のRSIを使用し、70と30を買われすぎ・売られすぎの閾値として設定し、極端な状況でのエントリーを回避します。

- ATRボラティリティ確認メカニズム – ATRを用いて市場の変動性を測定し、十分な強度のブレイクアウト時のみ取引を実行します。

取引ロジックは明確に設計されています。ロングエントリーは短期線が長期線を上抜け、RSIが70未満、かつ価格がATRの倍数を上回って確認された場合に行います。ショートエントリーは短期線が長期線を下抜け、RSIが30超、かつ価格がATRの倍数を下回って確認された場合に行います。システムには1%の動的ストップロスが設定され、リスクを効果的に管理します。

戦略の利点

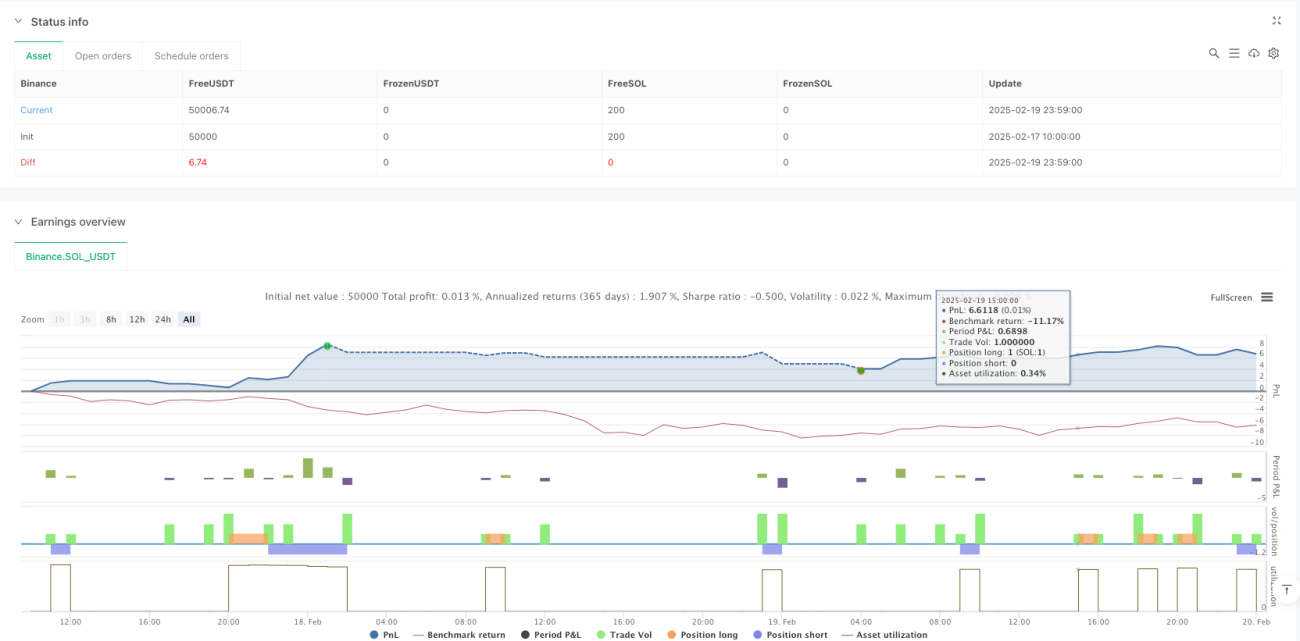

- 複数のテクニカル指標による相互検証により、シグナルの信頼性が向上。

- 動的パラメータ適応システムにより、異なる時間枠に適合。

- ATRベースのボラティリティフィルタリングにより、誤ったシグナルを低減。

- スマートストップロスシステムにより、各取引のリスクを厳格に管理。

- 明確なグラフィックマーカーや背景表示を含む完全な可視化システム。

戦略のリスク

- レンジ相場では頻繁な取引シグナルが発生し、取引コストが増加する可能性。

- 固定パーセンテージのストップロスはすべての市場環境に適しているとは限らない。

- 高ボラティリティ期間中にスリッページリスクが生じる可能性。

- パラメータ最適化には継続的な監視と調整が必要。

リスク低減のための推奨事項:

- 銘柄の特性に応じてストップロス率を調整する。

- トレンド強度確認メカニズムを追加する。

- 市場の変動状況をリアルタイムで監視する。

- 完全な資金管理システムを構築する。

戦略の最適化方向

- 適応型ストップロス機構を導入し、市場の変動に応じてストップロス率を動的に調整。

- トレンド強度フィルターを追加し、取引シグナルの質を向上。

- インテリジェント時間フィルターシステムを開発し、低流動性時間帯を回避。

- 出来高指標を統合し、シグナルの信頼性を強化。

- 動的パラメータ最適化システムを開発し、戦略の自己調整を実現。

まとめ

本戦略は、複数のテクニカル指標の相乗効果により、完全な取引システムを構築しています。柔軟性を維持しつつ、厳格なリスク管理により取引の安全性を確保しています。一定の限界はあるものの、継続的な最適化と改善により、本戦略は実用的な価値と発展の可能性を有しています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1