2

Follow

502

Followers

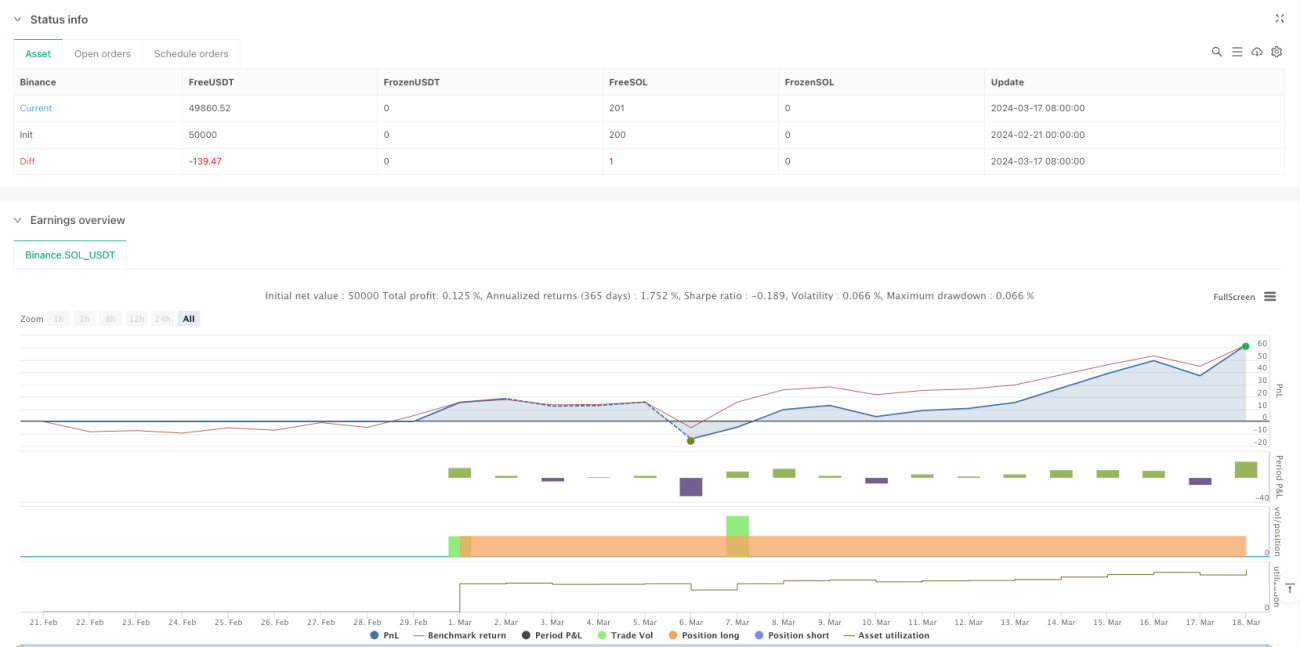

概要

この戦略は、ドンチャンチャネル(Donchian Channel)と200期間単純移動平均線(SMA)を組み合わせたトレンドフォロー型取引システムです。価格がドンチャンチャネルの上限・下限を突破する動きを観察し、SMAの動きと合わせて潜在的な買い・売りの機会を特定します。また、チャネル中央線に基づいた動的なストップロス機構を設計し、リスクを管理します。

戦略の原理

戦略の核となるロジックは、以下の主要要素に基づいています。

- 20期間を使用してドンチャンチャネルの上限、下限、中央線を計算

- 200期間SMAの動きを組み合わせて全体的なトレンド方向を判断

- エントリーシグナル

- 価格がドンチャンチャネルの上限を上抜け、かつSMA200より上にある場合、買いシグナルが発生

- 価格がドンチャンチャネルの下限を下抜け、かつSMA200より下にある場合、売りシグナルが発生

- ストップロスの設定

- 買いポジションのストップロスはチャネル中央線の下方45%の位置に設定

- 売りポジションのストップロスはチャネル中央線の上方45%の位置に設定

戦略のメリット

- トレンドフォロー効果が顕著:ドンチャンチャネルのブレイクとSMA200によるトレンド確認を組み合わせることで、中長期的なトレンドを効果的に捉えられる

- リスク管理が適切:チャネル中央線に基づいた動的ストップロス機構により、市場の変動に応じてストップロス位置を自動調整

- パラメータ設定がシンプル:チャネル期間と移動平均線期間の2つの主要パラメータのみ設定すればよく、過度な最適化リスクを低減

- ロジックが明確:エントリーとエグジットの条件が明確で、理解・実行が容易

- 適応性が高い:さまざまな取引銘柄や時間足に適用可能

戦略のリスク

- レンジ相場のリスク:横ばいのレンジ相場では、偽のブレイクアウトシグナルが頻発し、連続したストップロスが発生する可能性

- スリッページのリスク:急激な相場変動時には、実際の約定価格がシグナル価格と大きく乖離する可能性

- トレンド反転のリスク:大きなトレンド転換時に大きなドローダウンが発生する可能性

- パラメータ感応度:チャネル期間や移動平均線期間の選択が戦略パフォーマンスに大きく影響

リスク管理の推奨事項

- 他のテクニカル指標と組み合わせてクロス検証することを推奨

- トレンド強度フィルターを追加可能

- 動的なポジション管理手法を検討

- 定期的に戦略パラメータをチェック・最適化

戦略の最適化方向

-

シグナル最適化

- 出来高確認メカニズムの追加

- トレンド強度指標の導入

- 価格パターン分析の検討

-

ストップロス最適化

- 最適なストップロス割合の研究

- トレーリングストップロス機構の追加

- ボラティリティ適応型ストップロスの検討

-

ポジション管理の最適化

- ボラティリティに基づいた動的ポジションコントロールの実装

- 分割建て・分割決済メカニズムの導入

-

タイミングの最適化

- 市場環境認識メカニズムの追加

- 取引時間フィルターの最適化

まとめ

本戦略は、古典的なドンチャンチャネルと移動平均線指標を組み合わせることで、ロジックが明確でリスク管理が容易なトレンドフォローシステムを構築しています。シグナルが明確でリスク管理が適切というメリットがある一方、レンジ相場ではパフォーマンスが低下する可能性があります。出来高確認、ストップロス機構の最適化、動的ポジション管理の導入などにより、戦略にはさらなる改善の余地があります。実運用時にはリスク管理を徹底し、取引銘柄や市場環境に応じて最適化することをお勧めします。

Source

Pine

Related strategies

Comment

All comments (0)

No data

- 1