ダイナミックトレンドブレイクアウト指数移動平均クロスオーバー戦略

EMA

作成日:

2025-02-21 11:32:44

最終変更日:

2025-02-27 17:05:44

コピー:

5

クリック数:

394

2

フォロー

455

フォロワー

概要

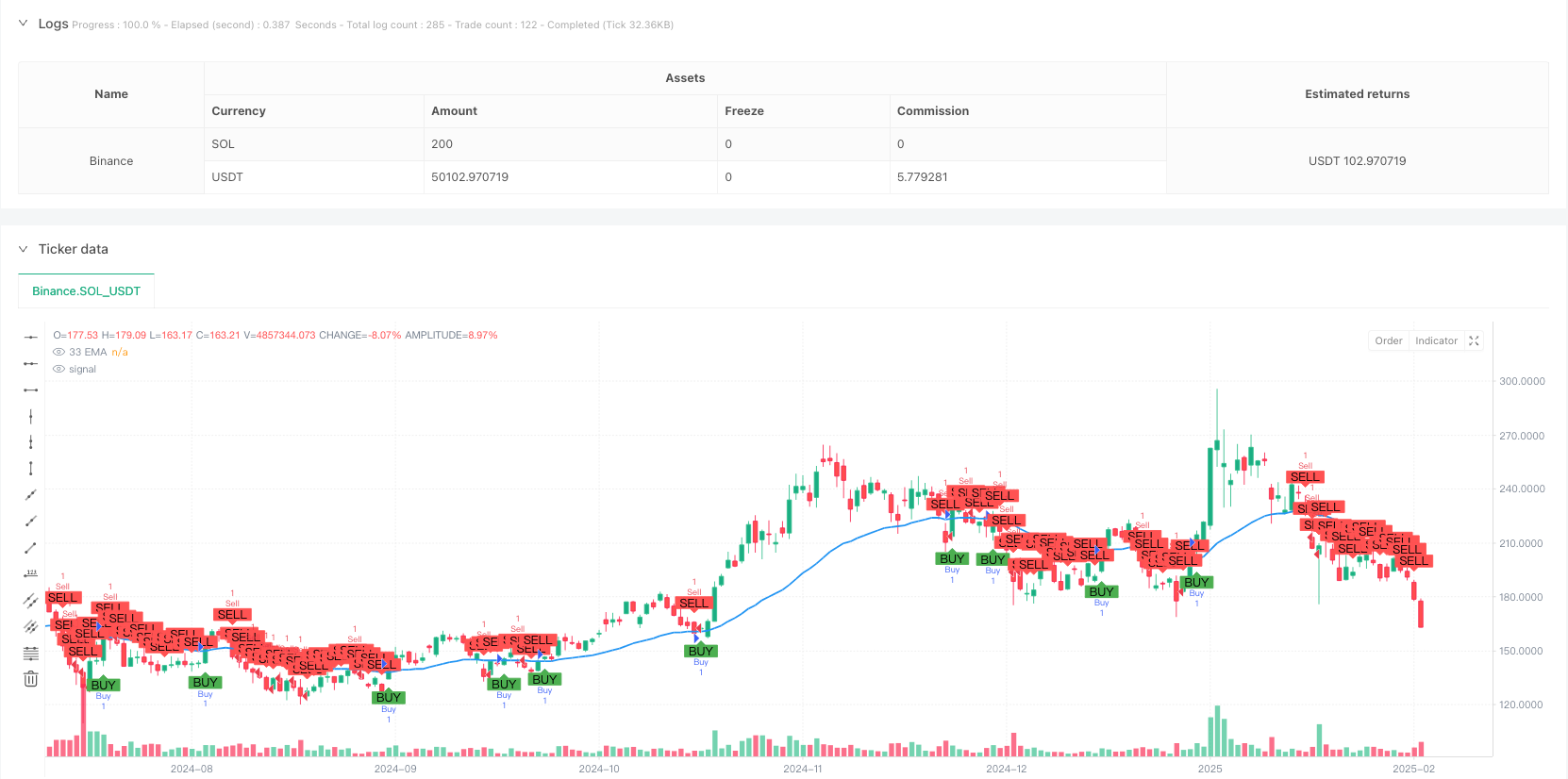

この戦略は,33周期指数移動平均 ((EMA)) に基づくトレンド追跡取引システムである.価格とEMAの交差関係によって市場トレンドの変化を認識し,波動的な高低点と組み合わせてストップ・ストップ・ロスのポジションを設定することで,トレンドの動態を追跡し,リスクを制御することができる.

戦略原則

策略の核心的な論理は,価格と33サイクルEMAの交差関係を観察することによって,トレンドの方向を判断することです. 閉盘価格が上方突破してEMAを安定させると,多信号を触発します. 閉盘価格が下方突破してEMAを破ると,空き信号を触発します. 策略は,波動の参照として14サイクルの高低点を使用し,最高点を多単一のストップと最低点を多単一のストップと設定します.

戦略的優位性

- 信号明晰:EMA交差を取引信号として使用し,基準を客観的に明確に判断し,主観的な推測を避ける.

- ダイナミックマネジメント:波動的な高低点のダイナミック調整により,ストップ・ストップ・ローズの位置を,市場の波動的な特性に適応させる.

- リスク管理: 取引ごとに明確なストップ・ロスの位置があり,リスクが効果的に管理されます.

- トレンド追跡: EMAのトレンド特性により,中長期のトレンドをよりよく把握できます.

- パラメータ最適化:異なる市場特性に合わせて最適化するために,重要なパラメータを調整できます.

戦略リスク

- 振動市場の損失:横盤振動市場の場合,頻繁な交差は連続的な停止損失を引き起こす可能性があります.

- 遅滞リスク:EMAは遅滞しており,トレンドの初期に重要な価格ポイントを逃す可能性があります.

- 偽突破のリスク:短期的な価格変動により偽突破が起こり,誤ったシグナルが発生する可能性があります.

- 止損幅度:波動極限を止損点として使用し,いくつかの場合,止損幅度が大きい可能性があります.

戦略最適化の方向性

- トレンドフィルター導入:より長い周期平均線またはトレンド指標を追加して,震動市場からの取引信号をフィルタリングできます.

- 改善のタイミング:RSIなどの振動指標を組み合わせて,より優良な価格位置で参戦する.

- 止損設定の最適化:風制御をより柔軟にするために,ATRを使用して止損距離を動的に調整することを検討できます.

- 取引量確認:取引量分析を追加し,信号の信頼性を向上させる.

- 退出メカニズムを完善する:移動停止の導入など,より細かい退出条件を設計する.

要約する

これは,構造が整った,論理がはっきりしたトレンド追跡戦略である。EMAを交叉してトレンドを捕捉し,波動的な高低点でリスクを管理する,優れた実用性がある。いくつかの固有の限界があるが,推奨された最適化方向によって,戦略の安定性と収益性をさらに向上させることができる。戦略の整体設計理念は,量化取引の核心原則に合致し,研究と実践に値する取引システムである。

ストラテジーソースコード

/*backtest

start: 2024-02-22 00:00:00

end: 2025-02-19 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlenMabasa

//@version=6

strategy("33 EMA Crossover Strategy", overlay=true)

// Input for the EMA length

ema_length = input.int(33, title="EMA Length")

// Calculate the 33-day Exponential Moving Average

ema_33 = ta.ema(close, ema_length)

// Plot the 33 EMA

plot(ema_33, color=color.blue, title="33 EMA", linewidth=2)

// Buy condition: Price crosses and closes above the 33 EMA

buy_condition = ta.crossover(close, ema_33) and close > ema_33

// Sell condition: Price crosses or closes below the 33 EMA

sell_condition = ta.crossunder(close, ema_33) or close < ema_33

// Swing high and swing low calculations

swing_high_length = input.int(14, title="Swing High Lookback")

swing_low_length = input.int(14, title="Swing Low Lookback")

swing_high = ta.highest(high, swing_high_length) // Previous swing high

swing_low = ta.lowest(low, swing_low_length) // Previous swing low

// Profit target and stop loss for buys

buy_profit_target = swing_high

buy_stop_loss = swing_low

// Profit target and stop loss for sells

sell_profit_target = swing_low

sell_stop_loss = swing_high

// Plot buy and sell signals

plotshape(series=buy_condition, title="Buy Signal", location=location.belowbar, color=color.green, style=shape.labelup, text="BUY")

plotshape(series=sell_condition, title="Sell Signal", location=location.abovebar, color=color.red, style=shape.labeldown, text="SELL")

// Strategy logic for backtesting

if (buy_condition)

strategy.entry("Buy", strategy.long)

strategy.exit("Take Profit/Stop Loss", "Buy", limit=buy_profit_target, stop=buy_stop_loss)

if (sell_condition)

strategy.entry("Sell", strategy.short)

strategy.exit("Take Profit/Stop Loss", "Sell", limit=sell_profit_target, stop=sell_stop_loss)