スマート多次元自己適応型トレンド取引システム

2

Follow

502

Followers

概要

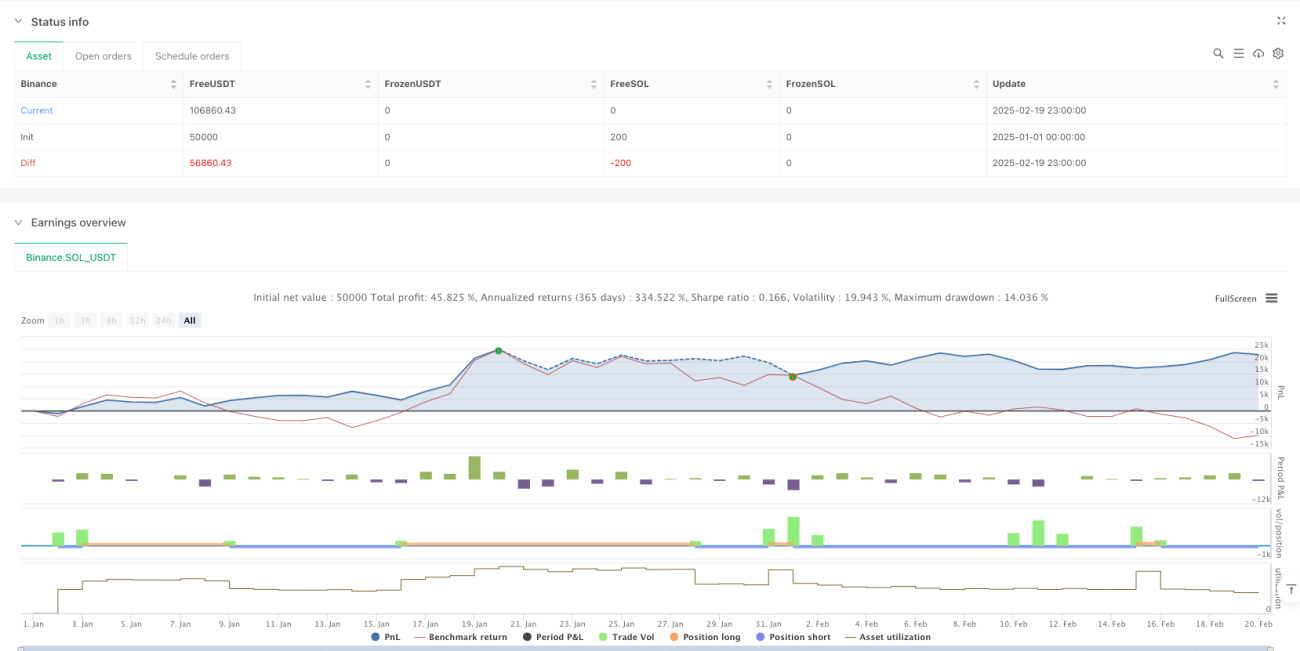

本戦略は、複数のテクニカル指標を融合したスマートな取引システムであり、フェアバリューギャップ(FVG)、トレンドシグナル、価格アクションの総合分析を通じて市場の機会を識別します。システムは二重戦略メカニズムを採用し、トレンドフォローとスイングトレードの特性を組み合わせ、動的なポジション管理と多次元のエグジットメカニズムによって取引パフォーマンスを最適化します。特にリスク管理に重点を置き、ボラティリティフィルターと出来高確認によりシグナルの品質を高めています。

戦略の原理

戦略の核心ロジックは以下の次元に基づいています:

- FVGギャップ識別 - 価格の窓空き(ギャップ)の大きさを計算して潜在的な取引機会を探す

- トレンド確認システム - 200日移動平均線、SuperTrend指標、MACDを組み合わせて市場のトレンドを確認

- スマートマネー確認 - RSIの買われすぎ/売られすぎ、出来高異常、価格行動パターンを取引トリガー条件として使用

- 動的ポジション管理 - ATRベースのボラティリティでポジションサイズを調整し、リスクエクスポージャーの一貫性を確保

- 多層的エグジットメカニズム - トレーリングストップと目標利確を組み合わせて取引の退出を管理

戦略の優位性

- 自己適応性が高い - 市場のボラティリティに応じてパラメータとポジションを自動調整

- リスク管理が充実 - 多重フィルターと厳格なポジション管理でリスクを抑制

- シグナル品質が信頼できる - 多次元指標の確認により取引シグナルの精度を向上

- 柔軟な取引方法 - トレンド相場とレンジ相場の両方の機会を捉えられる

- 資金管理が科学的 - パーセンテージリスク管理を採用し、資金の合理的な利用を確保

戦略のリスク

- パラメータ感応度 - 複数のパラメータ設定が戦略パフォーマンスに影響を与える可能性があり、継続的な最適化が必要

- 市場環境への依存 - 特定の市場環境では偽のブレイクアウトシグナルが発生する可能性

- スリッページの影響 - 流動性の低い市場では大きなスリッページに直面する可能性

- 計算の複雑性 - 複数の指標の計算によりシグナルに遅延が生じる可能性

- 資金要件が高い - 戦略を完全に実施するには比較的大きな初期資金が必要

戦略の最適化方向性

- 指標の重み最適化 - 機械学習手法を導入し、各指標の重みを動的に調整

- 市場適応性の強化 - 市場ボラティリティ適応メカニズムを追加

- シグナルフィルター改善 - より多くの市場ミクロ構造指標を導入

- 執行メカニズム最適化 - スマートオーダースプリットメカニズムを追加し、インパクトコストを低減

- リスク管理の高度化 - 動的リスク予算管理システムを追加

まとめ

本戦略は、複数のテクニカル指標と取引技術を総合的に活用し、完全な取引システムを構築しています。その優位性は、厳格なリスク管理を維持しながら市場の変化に適応できる点にあります。最適化の余地はあるものの、全体として合理的に設計された定量取引戦略です。

Source

Pine

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-20 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("Adaptive Trend Signals", overlay=true, margin_long=100, margin_short=100, pyramiding=1, initial_capital=50000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

// 1. Enhanced Inputs with Debugging OptionsStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1