2

Follow

502

Followers

概要

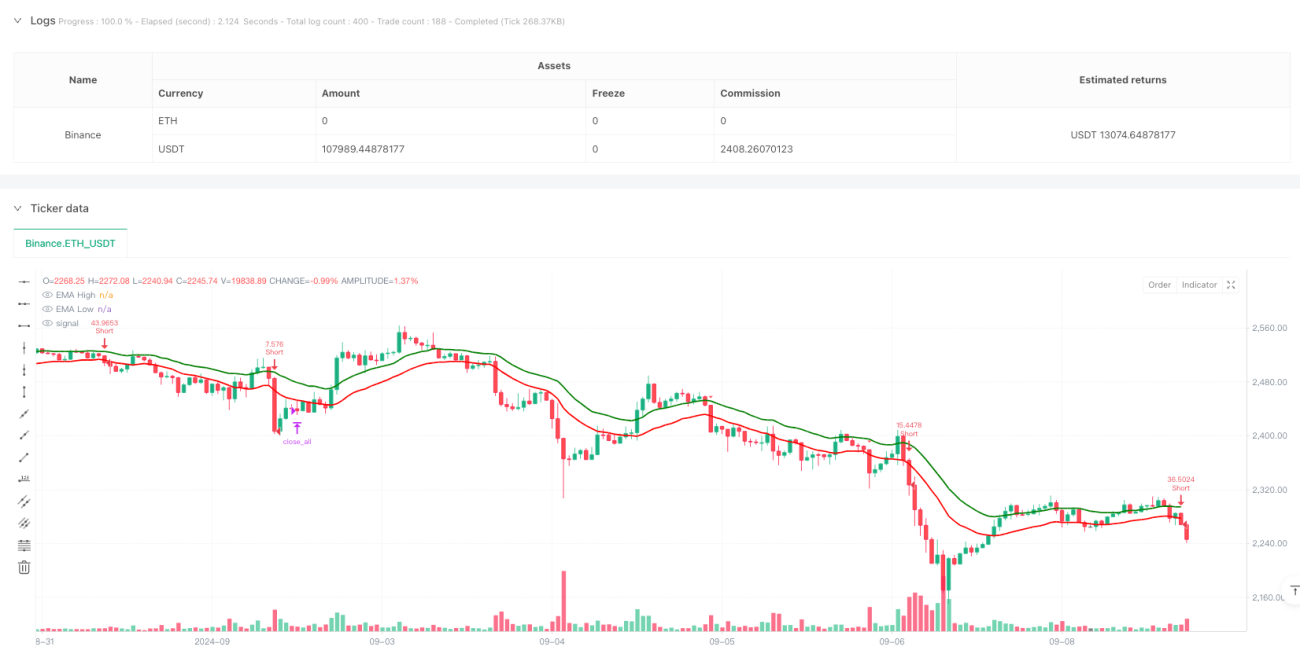

これは、EMAチャネル、RSIの買われすぎ/売られすぎ、MACDのトレンド確認など、複数のテクニカル指標に基づくデイトレード戦略です。3分足で動作し、EMAの高値/安値バンドとRSIおよびMACDのクロス確認を組み合わせて市場トレンドを捉え、ATRベースの動的ストップロス・利確、および固定されたクローズ時間を設定しています。

戦略の原理

戦略では、20期間のEMAを高値と安値それぞれに適用してチャネルを形成します。価格がチャネルをブレイクし、以下の条件を満たした場合にエントリーします。

- ロングエントリー:終値がEMA高値バンドを上抜け、RSIが50~70の範囲にあり、MACDラインがシグナルラインを上抜ける。

- ショートエントリー:終値がEMA安値バンドを下抜け、RSIが30~50の範囲にあり、MACDラインがシグナルラインを下抜ける。

- ATRを用いて動的にストップロス位置を計算し、リスクリワード比2.5倍で利確を設定。

- 1トレードあたりのリスクは口座の1%とし、ストップロス幅に基づいてポジションサイズを動的に計算。

- インド標準時15:00に全ポジションを強制クローズ。

戦略のメリット

- 複数のテクニカル指標によるクロス確認で、取引シグナルの信頼性が向上。

- ATR指標に基づく動的ストップロスにより、市場の変動に柔軟に対応。

- 固定リスク比率とリスクリワード比で、リスクを効果的にコントロール。

- 取引コスト(手数料計算)を考慮。

- 同一方向のナンピンを禁止し、過度なポジション保有リスクを回避。

- 固定クローズ時間により、夜間リスクを回避。

戦略のリスク

- 複数指標によりシグナルが遅れる可能性があり、エントリータイミングに影響。

- EMAチャネルはレンジ相場で頻繁なダマシのブレイクを生じる可能性。

- 固定リスクリワード比は市場環境によっては柔軟性に欠ける。

- RSIの範囲制限により、大きなトレンド相場を見逃す可能性。

- 強制クローズにより、重要なポジションで不利な退出を強いられる可能性。

戦略の最適化方向

- 出来高指標を補助確認として追加することを検討。

- 時間帯ごとの変動特性に応じてリスクリワード比を動的に調整。

- 市場変動率指標を導入し、RSIの閾値を動的に調整。

- トレンド強度フィルターを追加し、ダマシのブレイクを低減。

- 日内の時間帯特性に応じたパラメータ調整を検討。

- 過去の変動率分析を追加し、ポジション管理を最適化。

まとめ

本戦略は、複数のテクニカル指標を組み合わせることで、比較的完成度の高いトレーディングシステムを構築しています。戦略の強みは、動的ストップロス、固定リスク、クローズ時間の設定など、リスク管理が充実している点です。一部の遅延リスクはありますが、パラメータ最適化や補助指標の追加により、さらに戦略パフォーマンスを向上させることが可能です。本戦略は特に変動の大きいデイトレード市場に適しており、厳格なリスク管理と複数シグナルの確認により安定した収益を目指します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1