2

Follow

502

Followers

概要

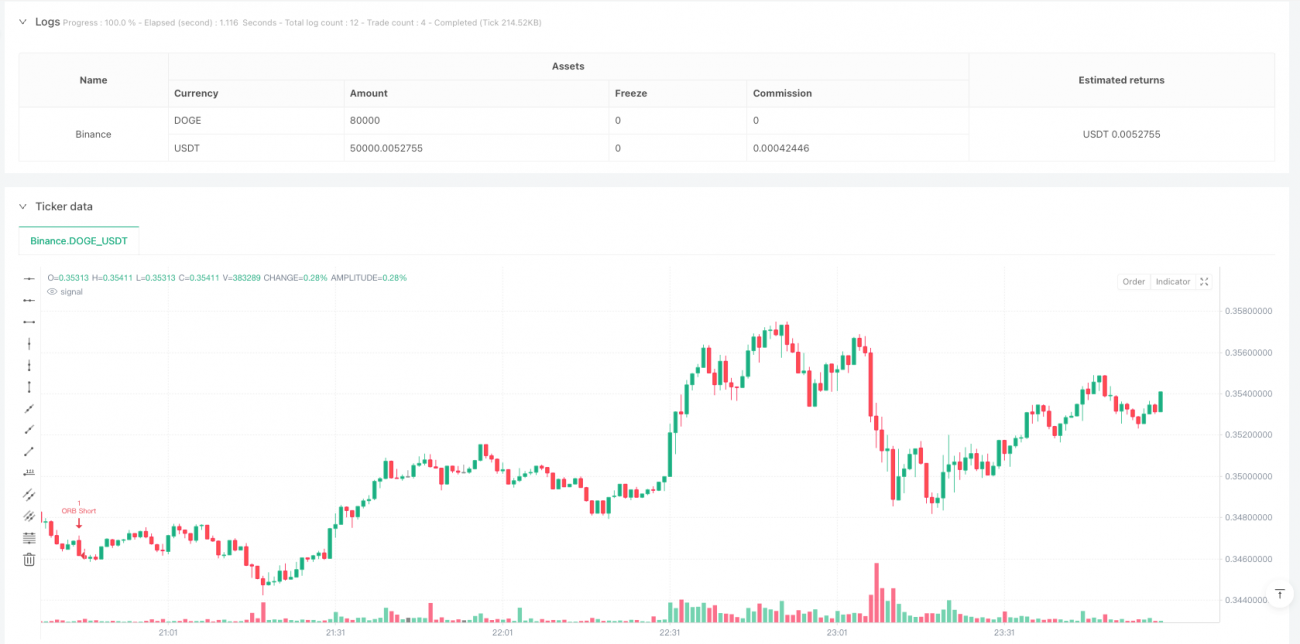

本戦略は、寄付き後のレンジブレイクアウトを活用した高頻度取引システムであり、取引日の早朝9:30~9:45(EST)に形成される価格レンジに焦点を当てています。価格がこの15分間のレンジをブレイクするかどうかを観察し、取引判断を行います。また、動的なストップロスと利確設定を組み合わせることで、リスクとリターンの最適なバランスを実現します。さらに、取引日を選択するフィルター機能を備えており、異なる期間の市場特性に応じて取引を取捨選択できます。

戦略の原理

戦略の核心的なロジックは、各取引日の寄付きから15分間(9:30~9:45 EST)で価格レンジを形成し、その間の高値と安値を記録することです。レンジが形成された後、戦略は当日12時までに価格のブレイクアウトを監視します。

- 価格がレンジの上限をブレイクした場合、ロングポジションを建て、ストップロスをレンジ幅の0.5倍、利確をストップロスの3倍に設定します。

- 価格がレンジの下限をブレイクした場合、ショートポジションを建て、ストップロスと利確の設定は同様の原理に従います。

また、重複取引を防ぐ仕組みも含まれており、1日1回のみの取引実行を保証し、引け時には全てのポジションを決済します。

戦略の長所

- 時間効率性:寄付き後の最も活発な取引時間帯に特化し、早朝の大きな値動きの機会を捉えることができます。

- リスク管理:実際の値動き幅に基づいて動的にストップロスと利確を設定し、リスク管理パラメータを決定します。

- 取引の柔軟性:週ごとに取引日を選択できる機能を提供し、特定の市場環境下での不利な取引日を回避できます。

- 明確な執行:取引シグナルが明瞭で、エントリー・エグジット条件が明確であり、主観的な判断に左右されません。

- 高い自動化度:全プロセスが自動執行され、人為的介入による感情的な影響を低減します。

戦略のリスク

- 偽ブレイクアウトのリスク:寄付きレンジ形成後の最初のブレイクアウトは偽ブレイクである可能性があり、ストップロスによる損失が発生します。

- 時間減衰:戦略は午前の時間帯のみ取引を行うため、他の時間帯での好機を逃す可能性があります。

- ボラティリティ依存:市場の値動きが小さい日には、十分な利益を得ることが難しい場合があります。

- スリッページの影響:高頻度取引戦略であるため、執行時に大きなスリッページ損失が発生する可能性があります。

- 市場環境依存:戦略のパフォーマンスは全体的な市場環境に大きく影響される可能性があります。

戦略の最適化方向性

- 出来高指標の導入:ブレイクアウト時の出来高を観察することで、偽ブレイクシグナルをフィルタリングできます。

- 取引時間の動的調整:異なる銘柄の活発な時間帯の特性に応じて、取引時間枠を最適化します。

- トレンドフィルターの追加:より大きな時間足のトレンド判断を組み合わせ、取引方向の精度を向上させます。

- ストップロス設定の最適化:動的なATR指標を使用してストップロス距離を設定することを検討できます。

- ボラティリティフィルターの追加:寄付き前にボラティリティレベルを評価し、その日の取引を実行するかどうかを決定します。

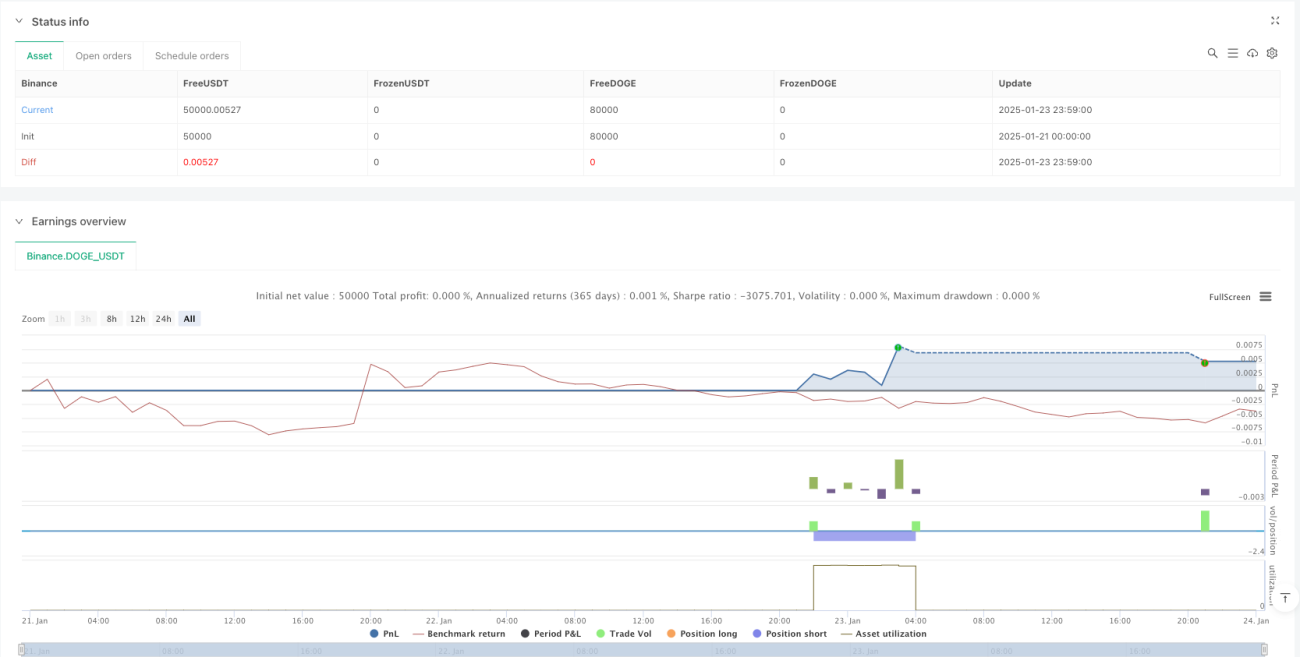

まとめ

本戦略は、合理的に設計されロジックが厳格な寄付きレンジブレイクアウト戦略であり、市場が最も活発な時間帯に集中することで取引機会を捉えます。戦略の利点は、明確な取引ロジックと充実したリスク管理メカニズムにありますが、同時に偽ブレイクアウトや市場環境への依存といった潜在的なリスクにも注意が必要です。継続的な最適化と改良を通じて、本戦略は実際の取引において安定した収益を上げることが期待されます。

Source

Pine

/*backtest

start: 2025-01-21 00:00:00

end: 2025-01-24 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"DOGE_USDT"}]

args: [["MaxCacheLen",580,358374]]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © UKFLIPS69

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1